Sterling Infrastructure STRL has been one of the top-performing infrastructure stocks over the past year, with its shares soaring 215.9%. The rally has far outpaced the Zacks Engineering - R&D Services industry's 36.8% gain, the Zacks Construction sector's 18.9% increase and the S&P 500's 23.9% return. Investors have rewarded the company for delivering outstanding financial performance while successfully positioning itself at the center of several long-term infrastructure trends, including AI-driven data centers, semiconductor manufacturing and mission-critical construction.

STRL Price Performance (1 Year)

Image Source: Zacks Investment Research

The sharp rise in the stock, however, has pushed Sterling's valuation above the industry average. The stock currently trades at a forward 12-month price-to-earnings (P/E) multiple of 31.76X compared with the industry average of 29.8X. While the premium is not excessive, it raises an important question for investors: Does Sterling's business outlook justify paying more for the stock, or has most of its future growth already been reflected in the current share price?

STRL Valuation vs Industry - P/E (F12M)

Image Source: Zacks Investment Research

Sterling's latest operating performance suggests the premium may still be supported. The company continues to report record earnings, rapidly expanding backlog and improving guidance, while analysts remain overwhelmingly bullish on its long-term prospects.

Sterling's Growth Story Remains Strong

Sterling's investment case continues to be supported by powerful earnings momentum and growing exposure to some of the fastest-growing infrastructure markets.

The company's first-quarter 2026 performance demonstrated that demand remains exceptionally strong. Revenues surged 92% year over year, while adjusted earnings per share jumped 120%. Adjusted EBITDA more than doubled, supported by expanding margins and strong execution across large infrastructure projects. Following these results, management raised its full-year guidance, expecting revenues between $3.7 billion and $3.8 billion and adjusted earnings per share (EPS) of $18.40-$19.05.

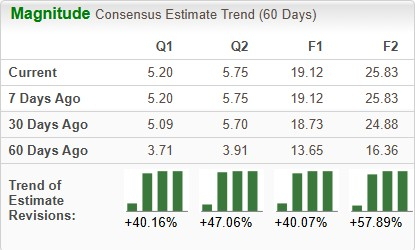

Analysts have become increasingly optimistic as well. Over the past 60 days, the Zacks Consensus Estimate for 2026 earnings has increased to $19.12 per share from $13.65, reflecting expected growth of 75.7% from 2025. Revenues are projected to climb 59.2% in 2026, followed by another 29.1% increase in 2027, while EPS is expected to grow another 35.1%.

STRL EPS Estimate Revision Trend

Image Source: Zacks Investment Research

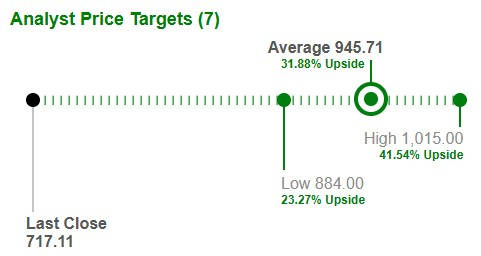

Wall Street also remains highly positive on the stock. Sterling carries an Average Brokerage Recommendation (ABR) of 1.00, with all nine covering analysts rating the shares a Strong Buy. The average price target of $945.71 suggests roughly 32% upside from current levels.

Image Source: Zacks Investment Research

Data Centers & Semiconductors Drive Long-Term Opportunity

The biggest driver of Sterling's future growth continues to be its rapidly expanding E-Infrastructure business.

First-quarter E-Infrastructure revenues increased 174%, while adjusted operating income climbed 177%, benefiting from continued investment in data centers and other mission-critical projects. Management noted that more than 90% of the segment's backlog now comes from mission-critical projects, including data centers, advanced manufacturing and semiconductor facilities.

The company also secured the initial phase of a large semiconductor fabrication campus during the quarter. Management believes this award represents only the beginning of a much larger semiconductor opportunity expected to accelerate later this decade. Sterling also continues expanding into new geographic markets as hyperscale customers increase investments across Texas, the Midwest and the Pacific Northwest.

Another important advantage is Sterling's growing ability to provide both site development and electrical services through the CEC acquisition. Management said that cross-selling opportunities are materializing much faster than originally expected, allowing the company to secure integrated contracts that improve productivity while supporting future margin expansion.

STRL’s Backlog and Acquisitions Provide Better Visibility

Sterling's record backlog provides another reason for investor confidence. Signed backlog reached $3.8 billion at the end of the first quarter, up 78% year over year, while combined backlog climbed 131% to $5.15 billion. Including unsigned awards and future project phases, Sterling now has visibility into nearly $6.5 billion of future work. Management believes increasing project size, complexity and duration continues to strengthen long-term earnings visibility.

The company is also using acquisitions to expand both its capabilities and geographic reach. After successfully integrating CEC, Sterling recently acquired Stone Ridge Contracting, strengthening its site development operations across the Pacific Northwest and Texas. Stone Ridge is expected to generate between $180 million and $200 million of revenues during 2026 while further expanding Sterling's presence in high-growth data center and industrial markets.

Strong cash generation and a healthy balance sheet provide additional flexibility to pursue further acquisitions while continuing share repurchases.

Premium Valuation Leaves Less Room for Error

Although Sterling's long-term outlook remains attractive, investors should recognize that expectations have become much higher following the stock's remarkable rally.

At 31.76X forward earnings, Sterling trades above the industry average. Such a valuation requires the company to continue delivering exceptional execution, sustained earnings growth and steady margin expansion.

The Building Solutions segment also remains under pressure. While first-quarter revenues improved modestly, management continues to expect residential construction markets to remain challenging throughout 2026 because of affordability pressures.

In addition, Sterling's growth increasingly depends on continued investment in AI infrastructure, hyperscale data centers and semiconductor manufacturing. Any slowdown in these capital spending trends, project delays or weaker customer investment could reduce future growth expectations. Likewise, integrating acquisitions while maintaining industry-leading margins across rapidly expanding operations remains an ongoing execution challenge.

Sterling vs. Its Competitors

Sterling competes with EMCOR Group EME, MasTec MTZ and Granite Construction GVA across data centers, utilities, transportation and other large infrastructure projects.

Sterling has significantly outperformed all three competitors over the past year, with its 215.9% gain comfortably exceeding MasTec's 126.3% increase, Granite Construction's 60.2% rise and EMCOR's 45.5% advance. The superior stock performance reflects Sterling's faster earnings growth and increasing exposure to AI-related infrastructure spending.

Valuation tells a balanced story. Sterling's forward P/E multiple of 31.76X sits above EMCOR's 25.27X but below MasTec's 36.18X, while Granite Construction trades at a lower valuation than Sterling. EMCOR offers investors a less expensive alternative with strong execution, MasTec commands the richest valuation because of its own infrastructure growth prospects, while Granite Construction provides steadier exposure to traditional public infrastructure markets. Sterling appears reasonably valued relative to its expected growth and sits between the lower-risk EMCOR and the higher-valued MasTec.

Is STRL Stock Still a Buy?

Sterling is no longer a bargain after more than tripling over the past year, but its premium valuation appears supported by equally impressive business momentum.

The company continues benefiting from favorable long-term trends in AI infrastructure, hyperscale data centers, semiconductor manufacturing and advanced industrial construction. Record backlog, rising analyst estimates, expanding margins, disciplined capital allocation and strategic acquisitions further strengthen its growth outlook.

While investors should expect occasional volatility after such a strong rally, Sterling's improving fundamentals suggest its growth story remains intact. Backed by a Zacks Rank #1 (Strong Buy), the stock still appears capable of delivering further upside for long-term investors, even while trading at a modest premium to the industry. You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sterling Infrastructure, Inc. (STRL): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

Granite Construction Incorporated (GVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).