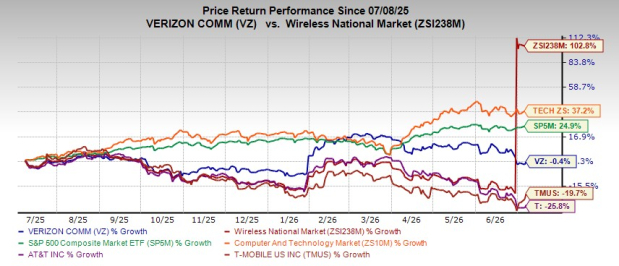

Verizon Communications Inc. VZ has fallen 0.4% in a year against the Wireless National industry’s growth of 102.8%. The stock has also underperformed the Zacks Computer & Technology sector during this period.

Image Source: Zacks Investment Research

The company has outperformed its peers like AT&T Inc. T and T-Mobile, US, Inc. TMUS. Shares of AT&T have declined 25.8%, while T-Mobile has declined 19.7% during this period.

Converged Mobility and Broadband Strategy is a Key Growth Driver

Verizon is increasingly bundling wireless and broadband services rather than selling them separately. If a customer opts for more than one service, such as wireless, home broadband and fiber from the same service provider, it makes it difficult for customers to switch service providers easily. The convergence strategy boosts customer retention and improves churn rate. Users are also preferring to have multiple connectivity needs met by a single trusted provider because it offers greater convenience, better value, and a more seamless experience. Hence, the convergence strategy is enabling Verizon to generate higher revenues per household while lowering customer acquisition costs through cross-selling.

Broadband expansion has become a major growth engine for Verizon. In the first quarter of 2026, Verizon delivered 341,000 broadband net additions, including 214,000 fixed wireless access net additions and 127,000 fiber broadband net additions. The Frontier acquisition expands Verizon’s fiber broadband footprint to 31 states and Washington, D.C., and Frontier results are included beginning Jan. 20, 2026. Management observed that the Frontier integration was on track, with a focus on convergence execution and a target of more than $1 billion of run-rate operating cost synergies by 2028.

Verizon has introduced AI-powered features to transform the user experience. It is also integrating AI to boost efficiency across its internal operations. The focus area includes automation, digital sales and service, micro segmentation of customers and lowering operating expenses. Such strategies are expected to improve profitability over time.

Verizon is also playing a critical role as the Official Telecommunications Services Sponsor for the 2026 FIFA World Cup. Providing network services to such a large-scale tournament demonstrates the reliability of Verizon’s 5G and fiber infrastructure. This significantly enhances its brand visibility.

Major Challenges

The U.S. wireless market remains highly competitive. The company faces competition from other major players such as AT&T and T-Mobile. AT&T is also rapidly expanding its fiber footprint and opting for a convergence strategy to improve churn and subscriber retention. High market saturation limits pricing power and increases reliance on promotional spending for user retention. While management described a shift away from promotion-heavy activity in first-quarter 2026, the company also acknowledged it retains the flexibility to react to competitive moves. That tradeoff can limit the pace of margin recovery if promotional intensity rises again.

The Frontier acquisition creates long-term opportunities but also brings execution risk. Integrating networks, combining operations and managing integration costs without disrupting customer service is a challenging endeavor.

Despite declining profitability due to high competition, telecom remains one of the most capital-intensive businesses. Fiber expansion and 5G network upgrades demand significant investment. The company still expects $16.0-$16.5 billion of capital expenditures in 2026. Such high capital investment will likely reap long-term benefits but will impact cash flow growth in the near term.

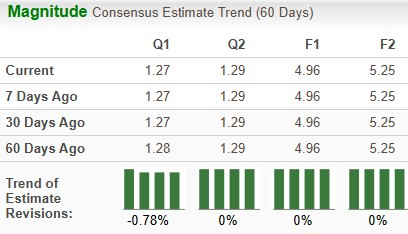

Estimate Revision Trend of VZ

Earnings estimates for VZ for 2026 and 2027 have remained unchanged for past 60 days.

Image Source: Zacks Investment Research

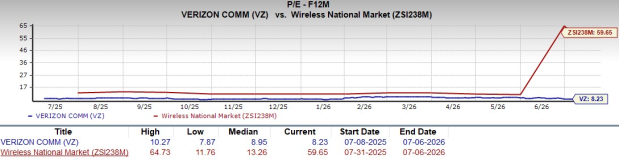

Key Valuation Metric of VZ

From a valuation standpoint, VZ appears to be trading relatively cheaper compared to the industry and its mean. Going by the price/earnings ratio, the company’s shares currently trade at 8.23, lower than 59.65 for the industry.

Image Source: Zacks Investment Research

End Note

Verizon's growth is supported by its convergence strategy. Bundling wireless and broadband services is boosting customer retention and increasing cross-selling opportunities. The company's AI-driven transformation program is improving customer experience and improving customer experience. However, intense competition in the wireless market is hindering top-line growth. Market saturation is limiting pricing power. Substantial capital investments in fiber and 5G network expansion are impacting free cash flow growth to some extent. With a Zacks Rank #3 (Hold), VZ appears to be treading in the middle of the road, and new investors could be better off if they trade with caution. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Verizon Communications Inc. (VZ): Free Stock Analysis Report

AT&T Inc. (T): Free Stock Analysis Report

T-Mobile US, Inc. (TMUS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).