SailPoint SAIL is trying to broaden its role in enterprise security as identity expands beyond employees to machines, contractors and AI agents. That shift gives SailPoint a larger opportunity, but it also makes execution more complicated. SaaS adoption, AI-related demand and on-premise migrations are all moving together, creating a growth story with timing risk.

SailPoint’s platform is built around identity governance, with Identity Security Cloud and IdentityIQ serving as its core offerings. The company helps enterprises manage lifecycle events, certify access, enforce least-privilege controls and analyze risk across complex systems.

The strategic role is getting broader. SailPoint now frames identity as a control plane for human and non-human identities, including machine identities and AI agents. That matters for large enterprises and government accounts that need auditable access controls across cloud, legacy and custom applications.

SAIL Growth is Being Led by SaaS ARR

SailPoint’s growth engine is increasingly SaaS-driven. Total annual recurring revenue reached $1.163 billion in the first quarter of fiscal 2027, up 26% year over year, while SaaS annual recurring revenue rose 36% to $781 million.

SaaS represented 92% of net new annual recurring revenue in the quarter, compared with 69% a year earlier. Dollar-based net retention held at 113%, showing that existing customers continue to expand usage and add capabilities.

For second-quarter fiscal 2027, SailPoint expects revenues between $308 million and $312 million, indicating year-over-year growth of 17-18%. Adjusted earnings are expected to be between 7 cents and 8 cents per share for the second quarter of fiscal 2027.

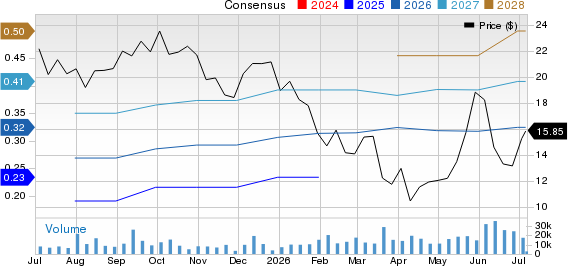

SailPoint, Inc. Price and Consensus

SailPoint, Inc. price-consensus-chart | SailPoint, Inc. Quote

SailPoint AI Push is Becoming More Tangible

AI is no longer just a product narrative for SailPoint. Non-human identities accounted for 40% of identity growth in the first quarter of fiscal 2027 and represented 14% of all identities managed in the company’s cloud offering. Management said about 10% of customers had adopted AI capabilities. Agentic Fabric and related launches are aimed at discovering AI agents, mapping ownership, enforcing authorization, securing prompts and monitoring behavior. Okta OKTA, Cisco Systems CSCO and Microsoft MSFT are other identity-focused companies investors may watch in this context.

Microsoft is SailPoint’s most significant competitor through its Microsoft Entra portfolio, which includes Entra ID, Identity Governance, Privileged Identity Management (PIM) and Conditional Access. Microsoft’s biggest advantage is its massive installed base of Microsoft 365 and Azure customers, allowing it to bundle identity governance with productivity, cloud and security offerings at attractive pricing.

Meanwhile, following the acquisition of Splunk and continued investment in cybersecurity, Cisco has strengthened its identity-focused security capabilities through Cisco Duo and its broader Zero Trust platform. Duo provides multi-factor authentication, device trust, adaptive access and identity verification, while Cisco integrates identity signals with networking and security operations.

Okta’s outlook is supported by steady demand for identity security, an expanding installed base, and rising attach of newer products such as Identity Governance, Privileged Access, and posture and threat capabilities. Management’s agent-focused roadmap and broad partner ecosystem keep Okta relevant as enterprises secure non-human identities and deploy AI workflows across multiple platforms.

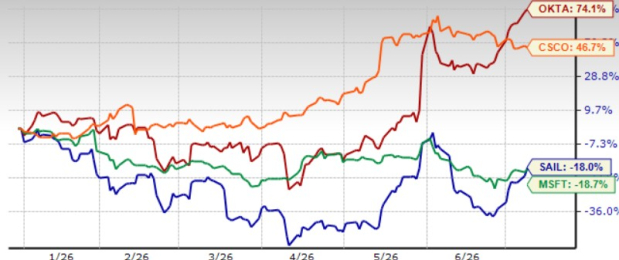

SailPoint shares have dropped 18% year to date, outperforming Microsoft’s fall of 18.7%, while Okta and Cisco shares have returned 74.1% and 46.7%, respectively.

SAIL Stock’s Price Performance

Image Source: Zacks Investment Research

SAIL Migration Opportunity Still Has Friction

The migration opportunity remains a major swing factor. SailPoint still has about $350 million of on-premise annual recurring revenue available for migration, and management has pointed to a typical 2-3 times uplift when customers move to SaaS and add capabilities.

The challenge is timing. These migrations can be complex, especially for large enterprises with legacy infrastructure and regulatory requirements. SailPoint expects only about 10% of its on-premise base to migrate in fiscal 2027, leaving a long runway but also making execution discipline important.

SailPoint Margins and Cash Flow Add Support

Growth is not coming at the expense of operating discipline. Adjusted operating margin improved to 13.5% in the first quarter of fiscal 2027 from 10.2% a year earlier.

Cash generation also improved the setup. SailPoint delivered $38 million in operating cash flow and $33 million in free cash flow during the quarter. Management also raised fiscal 2027 targets for annual recurring revenue, revenues and adjusted operating margin.

Conclusion

The bottom line is that SailPoint has a credible growth story tied to SaaS adoption, AI identity governance and enterprise migrations. Still, the pace of on-premise conversions and the revenue-recognition effects of the SaaS shift keep the near-term setup balanced.

SAIL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Okta, Inc. (OKTA): Free Stock Analysis Report

SailPoint, Inc. (SAIL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).