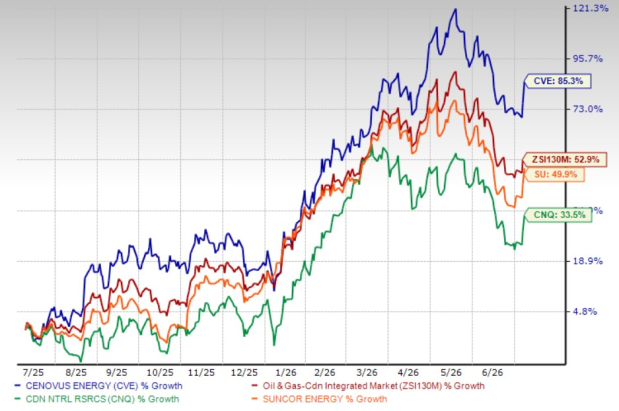

Over the past year, shares of Cenovus Energy Inc. CVE have climbed 85.3%, comfortably outpacing Canadian Natural Resources' CNQ 33.5% gain and Suncor Energy's SU 49.9% rally. During the same period, the stock has surpassed the sub-industry’s 52.9% return. The strong stock performance reflects growing investor confidence in the company's execution strategy and expanding operational footprint within Canada's energy sector.

Cenovus has steadily strengthened its business through disciplined capital allocation, acquisitions and production growth. As the stock continues to outperform, investors are evaluating whether the company's improving fundamentals can support further upside.

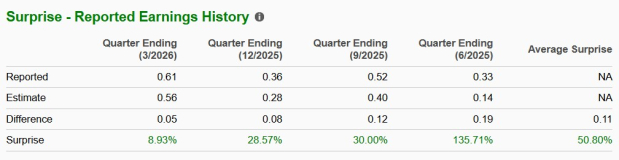

Adding to the bullish case, Cenovus has exceeded the Zacks Consensus Estimate in the past four quarters, delivering an average earnings surprise of 50.8%. Such consistent earnings outperformance highlights the company's operational strength despite the cyclical nature of the energy industry.

Key Factors Driving Cenovus' Growth Story

MEG Energy Acquisition Is Already Delivering Results

The acquisition of MEG Energy, completed in late 2025 for C$7.1 billion, has quickly become a major value driver for Cenovus. The transaction expanded the company's oil sands portfolio by adding assets adjacent to its Christina Lake operations, creating opportunities for operational efficiencies and lower development costs.

Management has indicated that redevelopment wells at Christina Lake North are performing better than originally anticipated. Consequently, the company expects to exceed its initial C$150-million synergy target for 2026, while maintaining its outlook of generating more than C$400 million in annual synergies by 2028.

Beyond near-term cost savings, the acquisition strengthens Cenovus' reserve base, enhances production capacity and further reinforces its leadership position among Canada's oil sand producers.

Low-Cost Operations Provide a Durable Competitive Advantage

One of Cenovus' biggest strengths remains its industry-leading cost structure. According to the company, combined operating and sustaining capital costs are approximately $21 per barrel, making Cenovus one of the lowest-cost producers in its peer group.

Its portfolio of long-life, high-quality oil sands assets enables the company to generate attractive returns across commodity price cycles. Management has also maintained a disciplined capital allocation strategy, with growth projects designed to earn acceptable returns even if WTI crude falls to around US$45 per barrel.

This structural cost advantage positions Cenovus to protect margins, generate healthy free cash flow and continue to create long-term shareholder value even in weaker commodity environments.

Integrated Operations Enhance Cash Flow Stability

While crude oil prices remain supportive, the longer-term outlook points to a more balanced global oil market as OPEC+ gradually restores production, geopolitical supply disruptions ease and inventories rebuild. According to the U.S. Energy Information Administration (EIA), Brent crude prices are expected to average $82 per barrel in 2026 before moderating in 2027 as higher global supply weighs on the market.

Against this backdrop, Cenovus appears well-positioned to generate resilient cash flows. The company's upstream portfolio is anchored by long-life oil sand assets with combined operating and sustaining capital costs of approximately $21 per barrel, while management expects its growth investments to generate acceptable returns even at WTI prices of US$45 per barrel. This low-cost production profile provides a meaningful cushion against weaker commodity prices.

Cenovus' integrated business model strengthens its earnings resilience. The company owns approximately 660,000 barrels per day of refining capacity across North America through refineries in Canada and the United States. This downstream business helps offset volatility in upstream earnings by capturing refining margins when crude price realizations weaken. In addition, its extensive pipeline connectivity and heavy-oil processing capabilities help reduce the impact of Western Canadian Select (WCS) price differentials.

The combination of low-cost upstream operations and a sizable downstream refining network enables Cenovus to generate relatively stable free cash flow across commodity cycles, supporting continued shareholder returns, disciplined capital allocation and long-term production growth.

Estimates Reflect Continued Earnings Growth

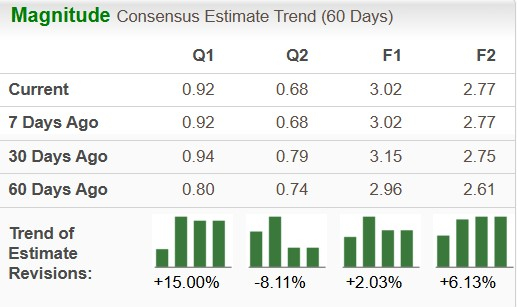

Analyst sentiment has become increasingly constructive toward Cenovus in recent months. The Zacks Consensus Estimate for 2026 revenues stands at $37.6 billion, implying 5.8% year-over-year growth, while earnings are projected to reach $3.02 per share, representing an impressive 96% increase from the prior year.

For 2027, consensus estimates call for an additional 1.5% increase in revenues, although earnings are expected to decline 8.2%.

Reflecting improved confidence in the company's outlook, earnings estimates have also moved higher. Over the past 60 days, the consensus EPS estimate has increased 2.03% for 2026 and 6.13% for 2027.

Attractive Valuation Compared With Peers

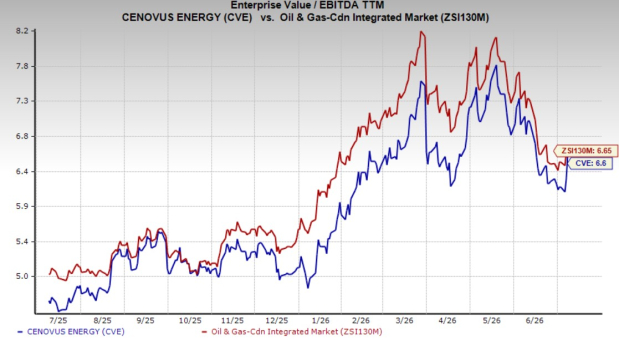

Despite its strong share price appreciation, Cenovus continues to trade at a reasonable valuation. The stock currently carries a trailing 12-month EV/EBITDA multiple of 6.6X, slightly below the industry average of 6.65X.

The valuation also remains well below Canadian Natural Resources, which trades at 9.08X EV/EBITDA. Although Suncor Energy commands a similar multiple, Cenovus offers a more compelling long-term growth profile, supported by acquisition synergies, low-cost operations and multiple development opportunities that should drive production growth.

Should You Buy CVE Stock?

Cenovus has built a compelling long-term investment case by combining disciplined execution with growth initiatives. The successful integration of the MEG Energy acquisition, one of the industry's lowest operating cost structures and a highly integrated upstream-downstream business model, positions the company to generate resilient earnings across varying commodity price environments.

At the same time, improving earnings estimates indicate growing confidence in management's ability to translate these operational strengths into higher profitability. Despite its strong rally over the past year, the stock continues to trade at an attractive valuation relative to the broader industry and several key competitors.

Backed by a Zacks Rank #1 (Strong Buy), Cenovus appears well-positioned to deliver sustainable shareholder value over the long term, making the stock an attractive consideration for investors seeking exposure to a financially disciplined and operationally efficient Canadian energy producer.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cenovus Energy Inc (CVE): Free Stock Analysis Report

Suncor Energy Inc. (SU): Free Stock Analysis Report

Canadian Natural Resources Limited (CNQ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).