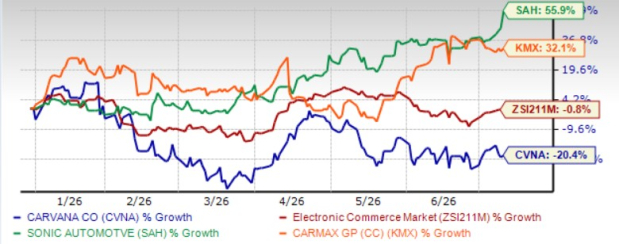

Used car e-retailer Carvana Inc. CVNA had an impressive run on the bourses last year, being the top-performing auto retail stock of 2025. While CVNA stock more than doubled last year, it has declined 20% so far this year. Carvana has also underperformed the industry as well as peers like CarMax KMX and Sonic Automotive SAH year to date. Shares of CarMax and Sonic Automotive have surged 32% and 56%, respectively, over the same timeframe.

YTD Price Performance Comparison

While short-seller accusations and stiff competition have weighed on the stock lately, Carvana’s journey has been nothing short of a rollercoaster. From being on the brink of a collapse in 2022, Carvana has been making tangible progress on operational and financial fronts and is now the second-largest used car retailer in the United States, just behind CarMax.

So, is this a good time to buy CVNA shares? Or should you be waiting on the sidelines? Let’s find out.

What’s Working in Favor of Carvana?

Instead of relying on a network of physical dealerships, the company operates a fully digital platform where customers can browse vehicles, arrange financing and schedule delivery online. Its well-known car vending machines are helping the brand stand out in a crowded market.The used car market remains highly fragmented, with Carvana’s share still below 2%. This suggests that there is ample room for the company to expand, especially as more consumers gravitate toward online car buying. In the longer term, the company continues to target selling 3 million cars per year in the 2030 to 2035 timeframe.

The first quarter of 2026 was the sixth straight quarter of Carvana achieving 40% or greater year-over-year unit sales growth. The company expects a sequential increase in retail units sold in the second quarter of 2026, and it remains on track to deliver growth in retail units for full-year 2026.

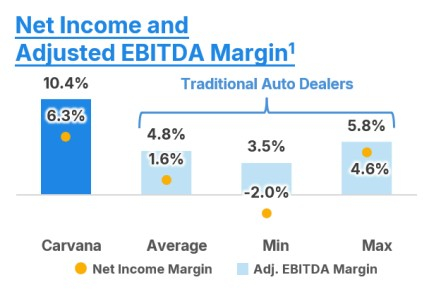

Financial performance is also improving. Adjusted EBITDA reached a record $672 million in the last reported quarter, compared with $488 million in the year-ago period, with industry-leading margins of 10.4%.

For the second quarter of 2026, Carvana expects a sequential increase in adjusted EBITDA. Its longer-term goal of reaching a 13.5% adjusted EBITDA margin further instills optimism.

Beyond growth and margins, Carvana is strengthening the operational backbone needed to support its long-term expansion. Proprietary technology platforms such as Carli and centralized planning tools help optimize staffing, logistics, workflow and throughput across reconditioning centers. By combining real-time operational data with software-driven decision-making, these systems improve productivity, simplify employee training and enable faster scaling as volumes increase.

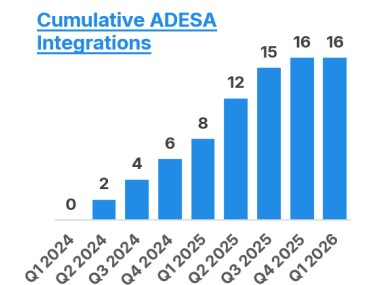

The company is also expanding its physical infrastructure. The ADESA U.S. acquisition continues to strengthen Carvana's logistics, auction and reconditioning network. As of the first quarter of 2026, the company had integrated 16 ADESA sites and plans to add another six to eight during 2026. Meanwhile, the expansion of the ADESA Clear wholesale platform is improving inventory mobility and production flexibility, supporting higher sales volumes while keeping future reconditioning investments more capital efficient.

How to Play CVNA Now

Carvana has evolved from a turnaround story into a profitable growth company with a scalable digital-first model. Its expanding infrastructure, improving margins and significant runway in the highly fragmented used-car market support a compelling long-term growth narrative. The recent pullback offers a more attractive entry point for investors.

The Zacks Consensus Estimate for Carvana’s 2026 and 2027 sales suggests a year-over-year increase of 38% and 26%, respectively. The consensus mark for 2026 EPS has been revised higher by 5 cents over the past 60 days to $1.58, reflecting improving analyst confidence. For 2027, the EPS estimate is $2.12, implying a 34% increase from the projected 2026 levels.

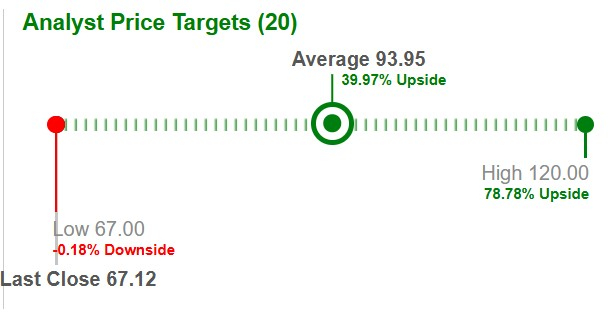

The Wall Street price target for the stock implies roughly 40% upside from current levels.

CVNA appears well-positioned to outperform over the long run, making the dip look like a buying opportunity rather than a warning sign.

Currently, Carvana carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Carvana Co. (CVNA): Free Stock Analysis Report

CarMax, Inc. (KMX): Free Stock Analysis Report

Sonic Automotive, Inc. (SAH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).