Zimmer Biomet ZBH appears well positioned for growth in the coming quarters, supported by the continued execution of its market strategies centered on People and Culture, Operational Excellence, and Innovation and Diversification pillars. Growth in the knee business revenues is backed by the robust adoption of its cementless offerings. Yet, a dull macro scenario and intense competition add to the worry.

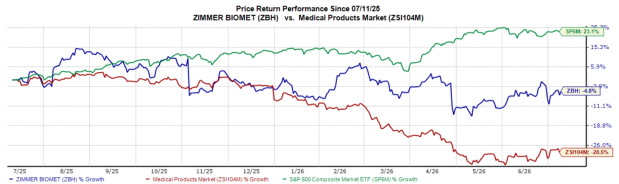

In the past year, this Zacks Rank #3 (Hold) stock has lost 4.8% compared with the 28.5% decline of the industry and the 23.1% growth of the S&P 500 composite.

The leading musculoskeletal healthcare company has a market capitalization of $17.18 billion. The company’s earnings yield of 9.6% is well ahead of the industry’s 2.6% yield. Zimmer Biomet beat on earnings in each of the trailing four quarters, delivering an average surprise of 2.53%.

Let’s delve deeper.

Tailwinds for ZBH Stock

Strong Prospects in Knee Business: Zimmer Biomet continues to focus on driving growth in its Knee franchise through higher cementless penetration and robotics utilization. In first-quarter 2026, total Knees net sales were up 1.8% on an organic constant currency basis. U.S. Knees rose 2.2% and International Knees grew 1.3% on the same basis. Technology & Data, Bone Cement and Surgical net sales rose 11.7% organically to $171.8 million, supporting the view that digital and robotic activity is extending beyond a single quarter.

Solid Market Expansion Strategies: Zimmer Biomet continues to execute its three core pillars of People and Culture, Operational Excellence and Innovation and Diversification, with the near-term focus on tightening commercial execution and sustaining mid-single-digit growth ambitions. First-quarter 2026 net sales increased 6.8% on a constant currency basis and 2.9% on an organic constant currency basis, supported by continued momentum in S.E.T. and Technology & Data and steady large-joint demand.

The 2025 restructuring plan is designed to reduce costs and transform the operating model through 2027, helping offset ongoing investment needs as the commercial organization evolves. On diversification, Paragon 28 continues to broaden its foot and ankle platform, while Monogram achieved its first development milestone in January 2026 and remains on track to begin commercialization in 2027.

Image Source: Zacks Investment Research

What Ails ZBH?

Macroeconomic Concerns: Zimmer Biomet continues to operate in an environment marked by pricing erosion risk, tariff exposure and elevated financing costs. Tariffs and integration costs weighed on profitability in 2025 and management continues to expect 2026 operating margins to be down about 50 basis points year over year, reflecting lower gross margins, Paragon 28 dilution and higher investments in the U.S. commercial channel. First-quarter 2026 results showed interest expense, net of $68.8 million, reflecting the ongoing impact from acquisition-related debt.

Competitive Landscape: Orthopedics remains highly competitive, with large players competing on pricing, implants, robotics and surgeon relationships. Zimmer Biomet must sustain product launches and technology upgrades to protect share and defend pricing across joints and extremities.

ZBH Stock Estimate Trend

The Zacks Consensus Estimate for Zimmer Biomet’s 2026 earnings per share (EPS) has remained constant at $8.48 in the past 30 days.

The Zacks Consensus Estimate for the company’s 2026 revenues is pegged at $8.53 billion, suggesting a 3.6% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Integra LifeSciences IART and Phibro Animal Health PAHC.

Globus Medical has an earnings yield of 5.5%, well ahead of the industry’s negative 3% yield. Its earnings surpassed estimates in each of the trailing four quarters, the average surprise being 26.3%. The company’s shares have rallied 43.8% against the industry’s 4.8% decline over the past year.

GMED carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Integra LifeSciences, carrying a Zacks Rank #2 at present, has an earnings yield of 16% against the industry’s negative 3% yield. Shares of the company have gained 22.8% compared with the industry’s 4.8% growth. IART’s earnings topped estimates in each of the trailing four quarters, the average surprise being 16.8%.

Phibro Animal Health, carrying a Zacks Rank #2 at present, has an earnings yield of 9.2% compared with the industry’s 2.8% yield. Shares of the company have climbed 43.1% against the industry’s 27.9% decline. PAHC’s earnings beat estimates in each of the trailing four quarters, the average surprise being 16.3%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zimmer Biomet Holdings, Inc. (ZBH): Free Stock Analysis Report

Integra LifeSciences Holdings Corporation (IART): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).