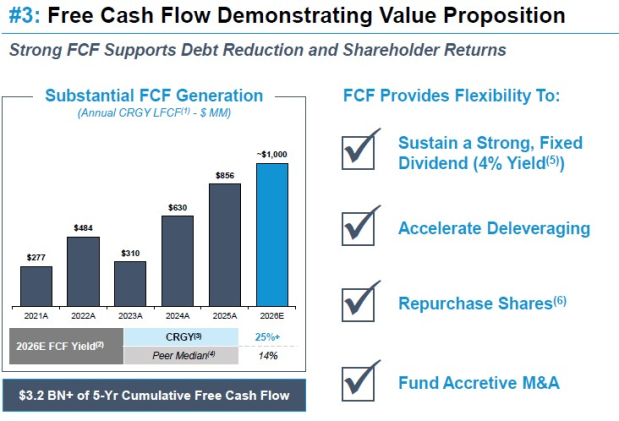

Crescent Energy Company CRGY has built its strategy around generating sustainable free cash flow (FCF) rather than pursuing production growth at any cost. This disciplined approach is helping the company strengthen its financial position while creating opportunities for long-term expansion.

CRGY's latest performance highlights the effectiveness of this model. In the first quarter of 2026, the company generated $690 million in adjusted EBITDAX and $192 million in levered free cash flow despite reporting a net loss driven by non-cash derivative mark-to-market adjustments. Management expects to generate nearly $1 billion in levered FCF in 2026, supported by a projected FCF yield of more than 25%.

Image Source: Crescent Energy Company

Operational execution has further strengthened the business. Crescent Energy has already captured approximately $120 million in synergies from the Vital Energy acquisition, exceeding its original target through improved drilling efficiency, infrastructure optimization and lower development costs. These efficiencies allow the company to reinvest selectively while directing excess cash toward debt reduction, dividends, share repurchases and value-accretive acquisitions. With roughly $2 billion of liquidity, no near-term debt maturities and a long-term leverage target of about 1x, Crescent Energy remains financially flexible.

Although cash flow remains exposed to oil and natural gas price volatility, Crescent Energy's focus on capital discipline, operational efficiency and strong cash generation provides a solid foundation for future growth. If management continues to execute effectively and commodity markets remain supportive, the company's cash flow-centric business model should remain a key driver of long-term shareholder value.

How Does Crescent Energy Compare With Peers?

Several U.S. exploration and production companies have recently been following a cash flow and capital discipline-centric theme, translating it into concrete financial targets and operational decisions.

EOG Resources, Inc. EOG continues to demonstrate strong cash flow generation through disciplined capital allocation and low-cost operations. In the first quarter of 2026, EOG generated $1.5 billion in free cash flow and expects a record FCF of $8.5 billion for full-year 2026 while maintaining its $6.5 billion capital budget. The company is also committed to returning at least 70% of annual FCF to its shareholders through dividends and share repurchases. With a low breakeven below $50 WTI, a pristine balance sheet and a flexible multi-basin portfolio, EOG Resources remains well positioned to sustain strong free cash flow generation across commodity cycles.

SM Energy Company SM demonstrated resilient cash flow generation in the first quarter despite its expenses related to the Civitas merger. The company reported adjusted FCF of $20 million, even after absorbing nearly $180 million in one-time integration and transaction costs. SM expects FCF to accelerate significantly through the remainder of 2026, supported by higher production, disciplined capital spending and growing merger synergies. Rising free cash flow is expected to support faster debt reduction, increased share repurchases and enhanced shareholder returns, positioning SM Energy for stronger financial performance in the second half of the year.

The Zacks Rundown on Crescent Energy

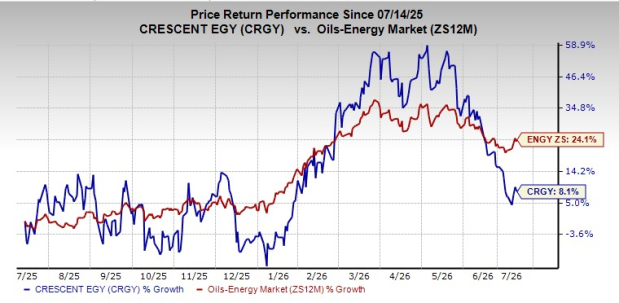

Shares of Crescent Energy have gained nearly 8.1% in a year compared with the Oil/Energy sector’s growth of 24.1%.

Image Source: Zacks Investment Research

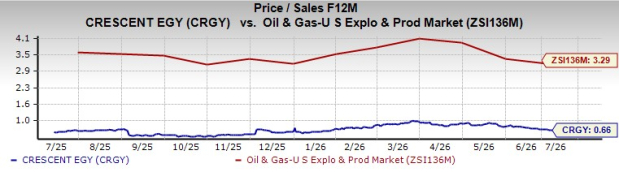

From a valuation perspective — in terms of the forward 12-month Price/Sales (P/S F12M) ratio — Crescent Energy is trading at a discount compared with the industry average, making it attractive for investors as more upside is still left in the stock.

Image Source: Zacks Investment Research

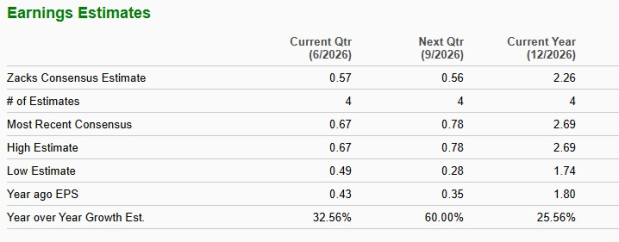

The Zacks Consensus Estimate implies about 25.6% year-over-year growth in Crescent Energy’s 2026 earnings per share. In other words, investors are paying up for CRGY at a point when the fundamentals of the company are expected to accelerate.

Image Source: Zacks Investment Research

CRGY stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Crescent Energy Company (CRGY): Free Stock Analysis Report

EOG Resources, Inc. (EOG): Free Stock Analysis Report

SM Energy Company (SM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).