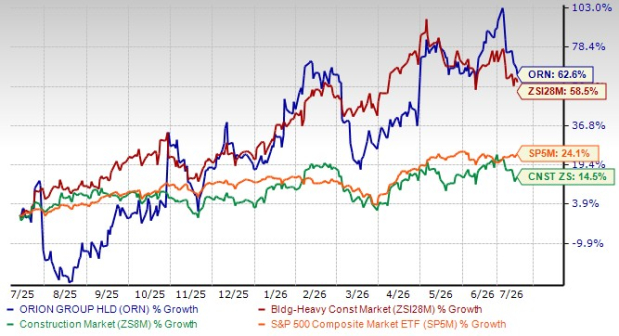

Orion Group Holdings, Inc. ORN has rewarded investors over the past year, with ORN shares gaining 62.6%. The move has outpaced the Zacks Building Products - Heavy Construction industry’s 58.5% rise, the Zacks Construction sector’s 14.5% gain and the S&P 500 Index’s 24.1% advance. That performance shows investors are giving Orion credit for improving execution, stronger end-market exposure and a larger growth runway.

ORN One-Year Price Performance

Image Source: Zacks Investment Research

The question now is whether the rally has already captured most of the near-term upside. Orion’s business momentum is real, but the stock no longer looks ignored.

Orion’s Q1 Results Show a Better Operating Base

Orion opened 2026 with a solid quarter. Revenues increased 15% year over year to $216.3 million, helped mainly by strong demand and service expansion in the Concrete segment. The company reported GAAP net income of $4.7 million, or 12 cents per diluted share, against a year-ago loss. Adjusted EBITDA rose 7% to $8.7 million, while adjusted earnings per share (EPS) improved to 5 cents from 1 cent a year earlier.

The numbers point to a company moving in the right direction. Gross profit rose 12% year over year, supported by higher revenues, strong project execution and favorable project completions. However, selling, general and administrative expenses also increased, partly to support business growth and the J.E. McAmis acquisition.

That mix matters for investors. Orion is improving, but it is still in a phase where growth investment and integration costs can limit how quickly earnings expand.

Marine Tailwinds Support the Long-Term Story for ORN Stock

Orion’s Marine segment remains central to the investment case. The company serves mission-critical waterfront infrastructure markets, including ports, dredging, marine transportation facilities, pipelines, environmental structures and specialty services. Management noted that demand continues to build across defense and port modernization projects.

The J.E. McAmis acquisition strengthens that story. The deal adds federal heavy civil construction expertise, expands Orion’s geographic footprint in markets such as Washington, Oregon, Canada, Florida, Alaska and Hawaii and brings high-value marine assets, including Jones Act vessels. The acquisition closed on Feb. 3, 2026, for $60 million plus possible contingent consideration, and is expected to be accretive to adjusted EBITDA and margin.

Orion also has access to opportunities tied to U.S. Navy infrastructure spending in the Pacific. The investor presentation notes that the company and its partners were selected on several Multiple Award Construction Contracts, allowing Orion to compete for future task orders with a more limited competition set.

These are attractive drivers because they are tied to national security, port modernization, shipyard upgrades, dredging and energy infrastructure. Such work can support multi-year demand and reduce dependence on a single commercial cycle.

Orion’s Concrete Growth Adds a Second Engine

The Concrete segment was the standout in the first quarter. Segment revenues rose sharply to $106 million from $61.5 million a year earlier, while adjusted EBITDA increased to $8.6 million from $2.8 million. Adjusted EBITDA margin improved to 8.1% from 4.6%.

Data centers are a key reason for the stronger outlook. Management said that data centers accounted for about 40% of Concrete’s revenues in the quarter, and that current backlog and pipeline composition suggest data centers will remain an important driver of profitable growth. Orion is also seeing opportunities in advanced manufacturing, transportation and cold storage, supported by reshoring, distribution demand and a favorable regulatory environment.

The expansion into site civil, earthwork and underground utilities should also help Orion pursue larger concrete projects. This gives the company more control over project delivery and may improve execution certainty for customers.

Backlog and Pipeline Improve Visibility for ORN Stock

Orion ended the first quarter with a backlog of $668 million, up from $640 million at the end of 2025. Marine backlog was $494 million, while Concrete backlog was $174 million. The company booked $219 million in awards and change orders during the quarter.

Management also highlighted a $24 billion pursuit pipeline, spread roughly evenly across 2026, 2027 and 2028 and beyond. After quarter-end, Orion was awarded more than $200 million in new work not yet included in backlog, including a $100 million port renovation project, a $40 million dredging project and a $24 million data center project.

This pipeline supports the growth case. It also explains why investors have become more willing to pay up for ORN shares.

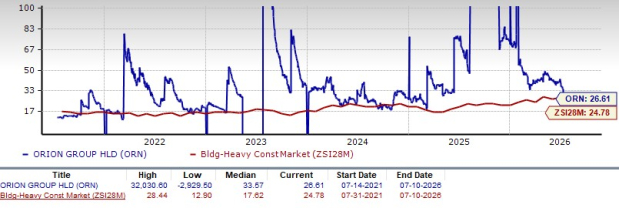

Valuation Is Not Cheap for ORN Stock After the Rally

Orion currently trades at 26.61X forward 12-month earnings, above the industry’s 24.78X. That premium suggests investors already expect execution to remain strong. Still, the multiple is below Orion’s five-year median of 33.57X, so the stock is not stretched versus its own history.

ORN Stock’s Valuation (P/E F12M)

Image Source: Zacks Investment Research

The valuation picture is mixed. Orion has a VGM Score of A, supported by a Value Score of B and a Growth Score of A. That suggests the stock still has appealing characteristics, especially if revenue growth, margin improvement and project wins continue. Yet, after a 63% rally, valuation leaves less room for disappointment.

Wall Street remains constructive. Out of seven recommendations contributing to Orion’s Average Brokerage Recommendation, six are Strong Buy ratings, resulting in an ABR of 1.29. The average price target of $18 implies roughly 28% upside from the last closing price. That support is meaningful, but investors should remember that estimated trends matter more for near-term stock performance.

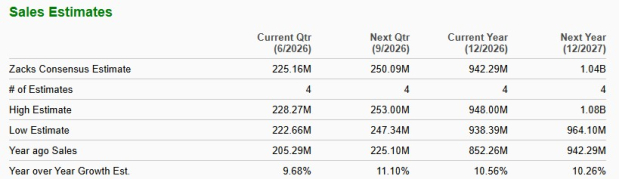

Orion’s Estimate Revisions Raise Some Caution

The main concern is that earnings estimates have moved lower recently. Over the past seven days, the 2026 EPS estimate slipped to 39 cents from 40 cents, while the 2027 estimate declined to 63 cents from 68 cents. That is not a large cut, but it shows analysts are not yet raising expectations despite the strong share-price move.

The growth outlook remains strong. The current estimate still implies EPS growth of 56% in 2026 and 59.6% in 2027. Revenue estimates also point to growth of 10.6% in 2026 and 10.3% in 2027. Orion’s 2026 guidance calls for revenues of $900 million to $950 million, adjusted EBITDA of $54 million to $58 million and adjusted EPS of 36-42 cents.

ORN’s EPS Estimates

Image Source: Zacks Investment Research

ORN’s Revenue Estimates

Image Source: Zacks Investment Research

However, the guidance also implies a back-half-weighted year. Management said the Marine business was lighter in the first quarter due to project timing, while confidence depends on backlog, recent wins and work expected to be delivered later in the year.

Execution Risks Remain Real for Orion

Orion’s business carries project-based risks. Backlog can fluctuate due to contract timing and execution, and there is no guarantee that backlog will convert into expected revenues or profits. Concrete projects typically run six to 12 months, while Marine projects can run 18 to 24 months, which creates timing variability.

The company also faces risks tied to fixed-price contracts, productivity delays, customer cancelations, funding delays and government budget constraints. These risks can affect profitability even when demand is strong.

Data centers are another area to watch. Management noted that visibility into data center work can be limited until projects are ready to move forward, even though activity remains heavy.

How Orion Compares With Competitors

Orion competes against several established infrastructure contractors, particularly in marine construction, heavy civil work and transportation projects.

Sterling Infrastructure STRL has significantly outperformed Orion over the past year, with shares rising 182.7%. Sterling has benefited from strong demand across e-infrastructure, manufacturing and transportation markets. Sterling also trades at a richer 30.07X forward earnings multiple, reflecting stronger growth expectations.

Granite Construction GVA offers another close comparison. Granite Construction operates across transportation, water and civil infrastructure markets. Granite Construction gained 30.9% over the past year and trades at a considerably lower forward P/E of 15.66X. Granite Construction, therefore, offers a cheaper valuation, although Orion currently appears to have stronger earnings growth prospects.

Construction Partners ROAD focuses primarily on infrastructure and highway construction. Construction Partners stock lost 10% over the past year and trades near Orion's valuation at 26.72X forward earnings. Construction Partners continues expanding through acquisitions, while Orion's marine specialization provides greater exposure to waterfront infrastructure and defense-related projects.

Among these peers, Orion differentiates itself through its combination of marine infrastructure leadership and rapidly expanding concrete operations tied to data center construction.

What Investors Should Do With ORN Stock Now?

Orion’s growth story is stronger than it was a year ago. The company has improved Marine exposure, a better Concrete growth platform, a large pipeline, rising backlog and a strategic acquisition that should expand its capabilities. These positives justify much of the stock’s rally.

Still, the 63% gain has raised expectations. The valuation is above the industry average, earnings estimates have slipped slightly, and 2026 execution depends partly on a stronger second half. With ORN carrying a Zacks Rank #3 (Hold), the right stance is patience. Existing investors may continue to hold the stock, but new investors may want a better entry point or clearer evidence of upward estimate revisions before becoming more aggressive. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Orion Group Holdings, Inc. (ORN): Free Stock Analysis Report

Sterling Infrastructure, Inc. (STRL): Free Stock Analysis Report

Granite Construction Incorporated (GVA): Free Stock Analysis Report

Construction Partners, Inc. (ROAD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).