Primo Brands Corporation PRMB is showing clearer sales momentum, but profitability has not caught up. That makes the stock story more balanced than a simple recovery narrative.

Premium-water demand and Direct Delivery stabilization are improving the setup. Margins, freight and integration costs still keep execution at the center of the investment case.

Primo Brands Has Broad North American Reach

Primo Brands operates across retail outlets, away-from-home locations such as hotels and hospitals, hospitality and food-service accounts, and direct delivery to homes and businesses. It also reaches consumers through Exchange and Refill, giving the company exposure to both packaged-water purchases and recurring hydration needs.

The company’s network spans every U.S. state and Canada, supported by more than 200,000 retail outlets, about 26,500 Exchange locations and more than 23,500 Refill stations. That breadth gives PRMB several ways to capture bottled-water demand across daily household use, workplace consumption and on-the-go occasions.

The portfolio also includes Poland Spring, Pure Life, Saratoga, The Mountain Valley, Arrowhead, Deer Park, Ice Mountain, Ozarka, Zephyrhills, Primo Water and Sparkletts. Investors comparing broader beverage exposure may also watch The Coca-Cola Company KO and PepsiCo Inc. PEP, both of which compete in hydration categories through larger beverage platforms.

PRMB Premium Water Is the Main Growth Driver

Premium water is carrying much of the growth story. In the first quarter of 2026, premium water sales rose 42.8% year over year to $105.5 million, well ahead of the broader portfolio.

Saratoga and The Mountain Valley were the standout brands, with combined sales up 43% in the quarter. Their momentum reflects new distribution, market-share gains and stronger consumer demand for premium hydration.

Comparable net sales increased 1.7%, supported by a 1.3% contribution from price and mix and a 0.4% contribution from volume. That mix benefit matters because premium water is doing more of the heavy lifting than larger categories such as regional spring and purified water.

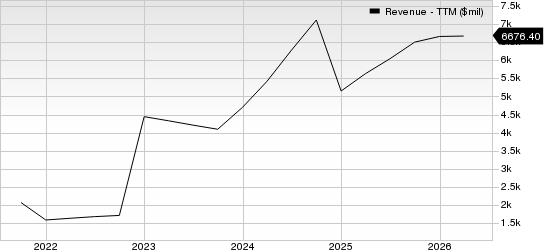

Primo Brands Corporation Revenue (TTM)

Primo Brands Corporation revenue-ttm | Primo Brands Corporation Quote

Primo Brands Works to Fix Direct Delivery

Direct Delivery remains PRMB’s biggest operational swing factor. Comparable Direct Delivery sales declined 3% year over year in the first quarter due to a smaller customer base and difficult comparisons.

The trend improved through the quarter. Sales performance strengthened sequentially each month, customer net additions approached breakeven in March and customer call volume declined.

On-time-in-full service exceeded 90% in March, an important sign that execution is stabilizing. Management expects Direct Delivery to move closer to breakeven in the second quarter and return to modest growth in the second half of 2026.

PRMB Still Faces Margin Pressure

The recovery is not yet translating cleanly into profitability. Gross margin fell to 28.6% from 32.3% in the first quarter, while operating income declined to $138 million from $153.2 million.

Net income from continuing operations dropped to $27.3 million from $34.7 million. Adjusted EBITDA fell 10.4% to $306 million, and comparable adjusted EBITDA margin contracted 260 basis points to 18.8%.

The pressure reflects higher Direct Delivery service spending, severe winter weather, tighter freight markets, incremental logistics costs and integration-related expenses. Until those costs ease, sales gains may not fully show up in earnings.

Primo Brands Corporation Price, Consensus and EPS Surprise

Primo Brands Corporation price-consensus-eps-surprise-chart | Primo Brands Corporation Quote

Primo Brands Signals a Balanced Setup

The bottom line is that Primo Brands has a credible sales recovery, but the earnings story remains uneven. Premium water is growing quickly, and Direct Delivery metrics are improving, but margin pressure keeps the stock from looking one-sided.

PRMB currently carries a Zacks Rank #3 (Hold). That rank fits a company with encouraging operating progress but not enough earnings leverage to support a more bullish near-term view.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock has a Value Score of B, Growth Score of B, Momentum Score of C and VGM Score of B. The B grades point to solid fundamental appeal, while the Momentum Score of C signals a more neutral timing backdrop.

For now, PRMB’s setup sits in the middle ground. Better premium mix and delivery recovery help the case, but investors still need clearer evidence that margins can improve as integration and service costs normalize.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Primo Brands Corporation (PRMB): Free Stock Analysis Report

CocaCola Company (The) (KO): Free Stock Analysis Report

PepsiCo, Inc. (PEP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).