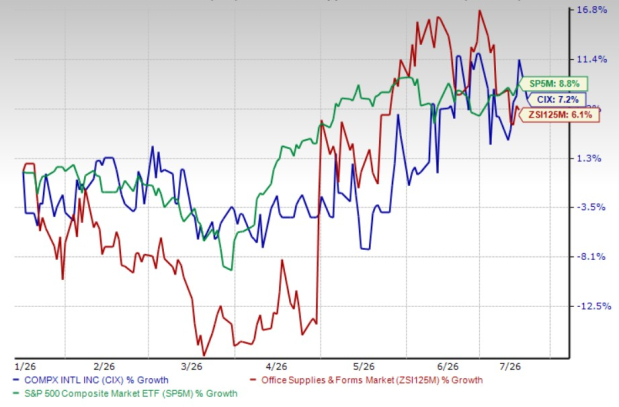

Over the past six months, CompX International Inc. CIX has gained 7.2%, modestly outperforming its sub-industry's 6.1% return. However, the stock has trailed the S&P 500's 8.8% growth.

CompX has continued to improve its operating performance through stronger profitability and disciplined cost management despite a challenging demand environment. While margin expansion has supported earnings growth, persistent cost pressures, tariff-related headwinds and a premium valuation have prompted investors to assess whether the stock's fundamentals justify its current price.

Improved Profitability on Better Product Mix & Margin Expansion

CompX delivered a solid improvement in profitability in the first quarter of 2026 despite generating only modest revenue growth, reflecting improved operating efficiency. Net sales inched up to $40.6 million from $40.3 million in the year-ago quarter, while operating income increased to $7.1 million from $5.9 million. Net income also improved to $5.9 million from $5.1 million.

The company's gross margin expanded to 32.7% from 30.2%, as the cost of sales declined as a percentage of revenues. The improvement was primarily driven by a more favorable customer and product mix within the Security Products segment. Although sales in the segment declined slightly, operating income rose 19%, with operating margins expanding from 18.3% to 22%, demonstrating CompX's ability to generate stronger earnings despite relatively flat sales.

Management also maintained stable operating expenses, allowing much of the higher gross profit to flow directly to the bottom line. The company's ability to improve profitability through operational execution rather than relying solely on revenue growth highlights its disciplined cost management. If margin improvements continue, CompX could remain well-positioned to withstand cost inflation while supporting earnings growth.

Cost Pressures & Demand Uncertainty Remain Key Headwinds

Despite the strong first-quarter performance, management remains cautious about the operating environment for the remainder of 2026. The company expects Security Products sales to remain generally flat as demand across several OEM markets continues to fluctuate. In addition, management indicated that the exceptionally strong margins reported in the first quarter were supported by an unusually favorable customer and product mix, making similar levels difficult to sustain over the balance of the year.

CompX also continues to face tariff-related surcharges on electronic components sourced from Asia, while certain domestic suppliers have implemented additional tariff-related price increases. Although the company plans to offset these higher costs through pricing actions, the ultimate success of these efforts will depend on tariff developments and customers' willingness to accept higher prices.

Beyond tariffs, broader macroeconomic uncertainty, geopolitical risks, supply-chain disruptions and changing customer demand remain potential challenges. These factors could pressure margins and earnings in upcoming quarters, even as the company maintains solid operational discipline.

Valuation Snapshot

Despite its improving profitability, CompX appears richly valued relative to the broader industry. The stock currently trades at a trailing 12-month enterprise value-to-EBITDA (EV/EBITDA) multiple of 9.87X, significantly above the industry average of 3.42X. The premium valuation suggests that investors have already priced in much of the company's recent operational improvement, leaving relatively less room for multiple expansion compared with peers.

Should You Buy CIX Stock?

CompX International continues to demonstrate solid operational execution, supported by expanding margins, disciplined cost control and improved profitability. The company's ability to generate higher earnings despite modest revenue growth reflects the strength of its operating model and management's focus on efficiency.

However, investors should also consider several near-term challenges. Tariff-related cost inflation, uncertain OEM demand, the possibility of moderating margins and broader macroeconomic risks could limit earnings momentum in the coming quarters. More importantly, the stock trades at a substantial premium to its industry, suggesting that much of the company's positive outlook may already be reflected in its share price.

Given the combination of solid fundamentals and an elevated valuation, new investors may prefer to wait for a more attractive entry point rather than chase the stock at the current levels. Existing shareholders can continue to hold on to the stock, but the premium valuation limits the margin of safety for fresh purchases despite the company's improving operational performance.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CompX International Inc. (CIX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).