Alto Ingredients, Inc. ALTO has been benefiting from improving profitability, favorable industry conditions and expanding opportunities from Section 45Z tax credits. The renewable fuels producer is also executing operational optimization and capacity expansion initiatives that are expected to strengthen its earnings profile and support long-term growth. Despite these positive developments, ALTO continues to trade at a discount to its industry and several key peers, making the stock worth a closer look.

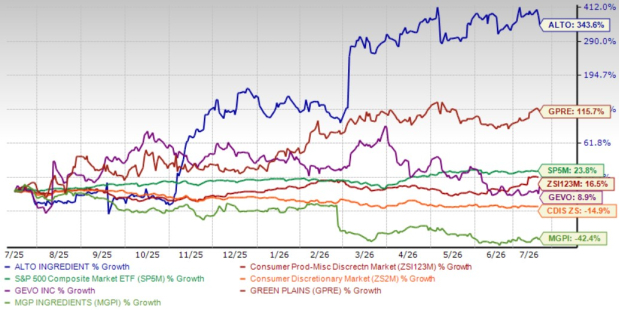

Shares of ALTO have soared 343.6% in the past year, significantly outperforming the broader market and most industry peers. Over the same period, the S&P 500 advanced 23.8%, while the Consumer Products - Discretionary industry gained 16.5%. In contrast, the broader Consumer Discretionary sector declined 14.9%.

ALTO has also significantly outperformed several notable competitors, including Green Plains Inc. GPRE, Gevo, Inc. GEVO and MGP Ingredients, Inc. MGPI. Green Plains and Gevo rose 115.7% and 8.9%, respectively, over the same period, while MGP Ingredients declined 42.4%. This exceptional performance has established ALTO as one of the standout stocks within its peer group.

ALTO Stock Past Year Performance

Image Source: Zacks Investment Research

Strong stock performance often comes with stretched valuations. However, despite its remarkable rally, ALTO remains attractively valued compared with the broader industry and several key peers, indicating there could still be room for further upside.

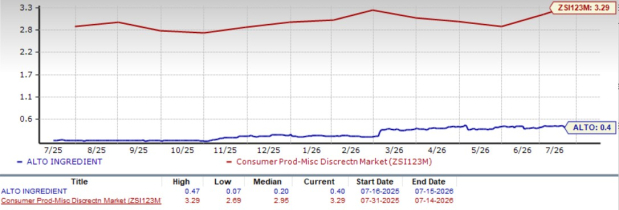

Alto Ingredients' Valuation Still Looks Attractive

ALTO currently trades at a forward 12-month price-to-sales ratio (P/S) of 0.4, well below the industry average of 3.29 and the sector average of 2.28. The stock also trades at lower multiples compared with Green Plains, Gevo and MGP Ingredients, whose forward price-to-sales ratios are 0.59, 1.99 and 0.73, respectively.

ALTO’s Valuation Compared to Industry

Image Source: Zacks Investment Research

So, what's driving ALTO's exceptional performance? Let's take a closer look.

Fundamentals Supporting ALTO’s Rally

Alto Ingredients' rally has been underpinned by a significant turnaround in its financial performance. In the first quarter of 2026, the company reported earnings of 5 cents per share against a loss of 16 cents in the year-ago quarter. Adjusted EBITDA improved to $4.7 million from a negative $4.4 million, while gross profit swung to $9.2 million from a gross loss of $1.8 million. The results underscored the success of ALTO’s strategic realignment and enhanced earnings power.

Favorable industry dynamics have also provided a meaningful boost. Strong export demand, higher export premiums relative to domestic renewable fuel sales and improving corn oil prices supported margins. Board crush margins increased to 17 cents per gallon from just 2 cents a year ago, while essential ingredients returns improved to 53.4% from 48.2%. Management also remains optimistic about demand growth from export markets and year-round E15 adoption.

At the same time, Alto Ingredients continues to invest in projects aimed at enhancing long-term profitability. A debottlenecking project at the Pekin dry mill is expected to raise annual production capacity by about 5 million gallons, while additional CO2 infrastructure investments should enhance flexibility and support higher-value opportunities. The company is also evaluating carbon capture and sequestration initiatives that could provide additional earnings opportunities over time.

Section 45Z tax credits have also emerged as another important growth driver for Alto Ingredients. The company recognized $3.9 million in tax-credit earnings during the first quarter and expects roughly $15 million in annual net proceeds from qualifying production volumes. Positive operating cash flow, lower debt and more than $94 million in borrowing capacity have further strengthened its financial position.

What Could Limit ALTO's Upside?

Alto Ingredients remains exposed to fluctuations in commodity prices and broader macroeconomic conditions. On its first quarter of 2026 earnings call, management noted that rising energy costs, geopolitical tensions in the Middle East and disruptions to freight and export logistics could create volatility in input costs and product demand. Since the company's margins are closely tied to corn, natural gas and ethanol prices, sustained cost inflation or weaker market conditions could weigh on profitability.

The company also faces the risk of weaker industry margins if production outpaces demand. Management acknowledged that strong spring crush margins have historically encouraged higher ethanol production, often leading to oversupply and margin compression in the second half of the year. While export demand and the potential expansion of year-round E15 could help absorb additional volumes, their impact remains uncertain.

The Bottom Line on Alto Ingredients

Alto Ingredients has strengthened the business through higher profitability, favorable industry conditions and ongoing operational investments, supporting its impressive stock performance. ALTO’s shares also continue to trade at an attractive valuation despite the strong rally. However, exposure to commodity price volatility and the potential for industry margin pressure remain key risks to monitor. With a Zacks Rank #3 (Hold), existing investors may consider staying invested, while new investors may await a more attractive entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Alto Ingredients, Inc. (ALTO): Free Stock Analysis Report

Gevo, Inc. (GEVO): Free Stock Analysis Report

Green Plains, Inc. (GPRE): Free Stock Analysis Report

MGP Ingredients, Inc. (MGPI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).