The Cooper Companies, Inc.’s COO growth is fueled by CooperVision’s premium lens migration and MiSight’s myopia-management leadership, supported by CooperSurgical’s women’s health and fertility portfolio.

However, channel volatility, private-label transition risks, Asia-Pacific softness and tariff/FX pressures weigh on near-term performance. Long-term opportunities remain strong, but execution and regional challenges could affect margin resilience and growth trajectory.

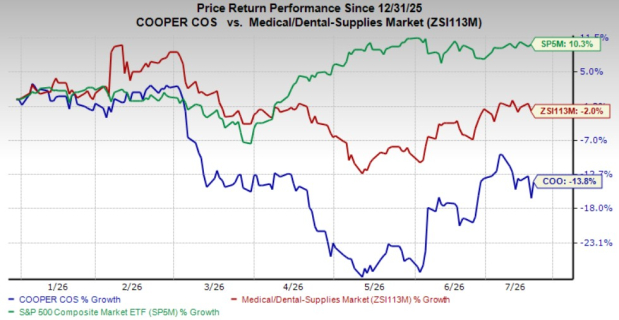

Shares of this Zacks Rank #3 (Hold) company have lost 13.8% so far this year compared with the industry's 2% decline and the S&P 500 Index’s 10.3% rise.

Image Source: Zacks Investment Research

Cooper Companies, with a market capitalization of $13.36 billion, is a global specialty medical device company.

COO’s bottom line is estimated to improve 8.3% over the next five years. Its earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 5.80%.

What's Driving COO’s Performance?

Promising Premium Contact Lens and Myopia Portfolio: CooperVision's premium product strategy remains one of its strongest competitive advantages. The company recorded its 18th consecutive year of market share gains, supported by double-digit growth in MyDay daily silicone hydrogel lenses and 23% growth in MiSight.

Premium offerings such as MyDay multifocal, Energys and toric lenses all expanded more than 15%, while the launch of MyDay MiSight across Europe and MiSight in Japan has seen encouraging clinician adoption. As higher-value products become a larger portion of sales, Cooper should benefit from stronger pricing power, improved customer retention and a structurally higher-margin revenue mix.

Operational Restructuring Is Delivering Sustainable Margin Expansion: The benefits of last year's organizational restructuring are becoming increasingly visible across the income statement. Cooper posted a 20% increase in adjusted earnings per share despite only modest organic revenue growth, as operating expenses declined meaningfully as a percentage of sales.

Management highlighted structural cost reductions, shared-service optimization and broader adoption of AI-enabled automation across marketing, planning and back-office functions. These efficiency gains are funding higher investments in sales and marketing while simultaneously lifting profitability and free cash flow. This demonstrates that the restructuring is creating durable operating leverage rather than relying solely on temporary cost reductions.

Product Launch Pipeline and Contract Wins Boost Second-Half Prospect: Cooper has entered the second half of fiscal 2026 with one of its strongest product launch calendars in recent years, supported by expanding MyDay, MiSight and private-label offerings across multiple regions.

Management highlighted several recently secured branded and private-label contracts, particularly for MyDay products, which are expected to contribute more meaningfully from third quarter onward. In addition, supply constraints that had previously limited contract execution have now been eliminated, enabling the company to fully capitalize on new customer wins.

Combined with expanding availability of premium silicone hydrogel lenses and ongoing launches across Asia-Pacific and Europe, this commercial pipeline provides greater confidence in accelerating revenue growth during the back half of the fiscal year.

What’s Weighing on COO Stock?

Weakness in Japan Continues to Weigh on Asia-Pacific Growth: Japan remains the company's most significant operational challenge. CooperVision's Asia-Pacific revenues declined as competitive pressure on legacy hydrogel lenses offset strong adoption of newer premium products.

Management acknowledged that competitors are gaining share in older hydrogel categories while Cooper has deliberately avoided aggressive price discounting. Although numerous launches, including MyDay toric, MiSight and expanded clariti products, are expected to restore regional growth beginning fiscal third-quarter, Asia-Pacific is likely to remain a drag during the near term. Continued execution delays could postpone the expected recovery and limit overall revenue acceleration.

Fertility Business Still Faces Geographic and Market Uncertainty: Although industry fundamentals are improving, CooperSurgical's fertility business continues to face meaningful external risks. Management highlighted ongoing weakness in China, where fertility activity is yet to recover, while geopolitical tensions in the Middle East continue creating uncertainty around product distribution in an important regional market.

In addition, equipment installations remained soft during the quarter, reflecting cautious capital spending by fertility clinics. Because management expects only a gradual recovery rather than a sharp rebound, any further deterioration in international demand or geopolitical disruptions could slow CooperSurgical's earnings recovery.

Competitive Risks Increasing Across Key Product Categories: Cooper enjoys strong positioning in both contact lenses and women's health, but competition continues to intensify across several important franchises. In vision care, pricing remains aggressive in portions of Asia-Pacific, particularly within legacy hydrogel products, while myopia-control alternatives continue expanding globally.

Within CooperSurgical, management continues monitoring the potential competitive threat to Paragard, even though its current guidance already assumes some market impact. Maintaining premium pricing while defending market share will require continued innovation, successful product launches and sustained investment in sales, marketing and clinical education over the coming years.

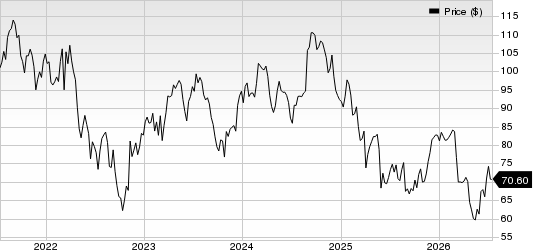

The Cooper Companies, Inc. Price

The Cooper Companies, Inc. price | The Cooper Companies, Inc. Quote

Estimate Trend

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $4.31 billion, implying growth of 5.3% from the year-ago reported figure. The consensus mark for adjusted EPS is pinned at $4.63, indicating an improvement of 12.4% from the previous year’s recorded level.

In the past 60 days, COO’s earnings estimate for fiscal 2026 has moved north 2 cents.

Stocks to Consider

Some better-ranked stocks from the broader medical space are Align Technology ALGN, Intuitive Surgical ISRG and Cardinal Health CAH, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Align Technology reported first-quarter 2026 earnings per share of $2.58, which beat the Zacks Consensus Estimate by 14.2%. Revenues of $1.04 billion surpassed the Zacks Consensus Estimate by 1.8%.

Align Technology has an estimated long-term earnings growth rate of 10.3%. ALGN’s earnings surpassed estimates in three of the trailing four quarters and missed once, the average surprise being 7.80%.

Intuitive Surgical reported first-quarter 2026 adjusted EPS of $2.50, which beat the Zacks Consensus Estimate by 20.2%. Revenues of $2.77 billion surpassed the Zacks Consensus Estimate by 6.2%.

Intuitive Surgical has an estimated long-term earnings growth rate of 14.3%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Cardinal Health reported a third-quarter fiscal 2026 adjusted EPS of $3.17, which beat the Zacks Consensus Estimate by 13.2%. Revenues of $60.94 billion missed the Zacks Consensus Estimate by 2.3%.

Cardinal Health has an estimated long-term earnings growth rate of 17%. CAH’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 10.3%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Cooper Companies, Inc. (COO): Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).