Cencora, Inc. COR recently announced that it has agreed to merge its wholly owned subsidiary, MWI Animal Health, with Covetrus in a transaction that values MWI at an enterprise value of $3.5 billion. MWI has long served as Cencora’s dedicated animal health distribution arm, supplying pharmaceuticals, vaccines and medical products to veterinary clinics and livestock producers across the United States.

Strategically, the move allows Cencora to unlock value from MWI while aligning the business with a partner solely focused on animal health technology and services. MWI’s strong supply chain and distribution footprint will be combined with Covetrus’ tech-enabled veterinary solutions, creating a broader, more integrated platform designed to enhance efficiency, expand access and support long-term growth in the animal health ecosystem.

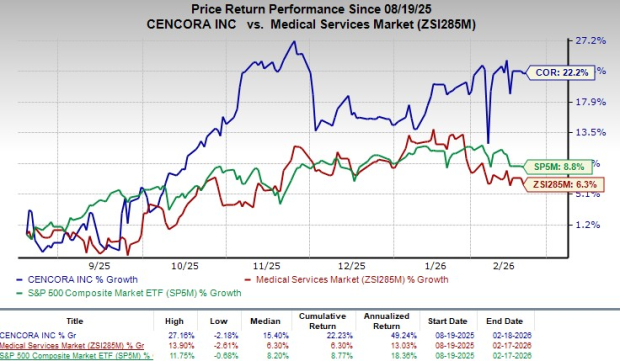

Likely Trend of COR Stock Following the News

Following the announcement, COR shares traded flat during yesterday’s after-market trading. Shares of the company have gained 22.2% in the last six-month period compared with the industry’s 6.3% growth. The S&P 500 has gained 8.8% in the same time frame.

Over the long run, the transaction allows Cencora to unlock capital from MWI while still retaining meaningful upside through its 34.3% equity stake in the combined company. The upfront cash and preferred equity strengthen Cencora’s balance sheet, providing flexibility to reinvest in higher-growth specialty segments.

At the same time, by partnering with MWI through a dedicated animal health platform, Cencora positions the business for potentially faster growth and operational synergies, providing it with continued exposure to the expanding animal health market without bearing full operational responsibility.

Meanwhile, COR currently has a market capitalization of $70 billion.

Image Source: Zacks Investment Research

More on the Deal

The transaction values MWI at an enterprise value of $3.5 billion, exceeding Cencora’s current carrying value of the business. The combination brings together MWI’s established supply chain infrastructure and customer relationships with Covetrus’ global animal health technology and services platform.

Upon closing, Cencora will receive $1.25 billion in upfront cash proceeds, $800 million in preferred equity and $1.45 billion in common equity of the combined company, resulting in a 34.3% non-controlling common equity stake. The structure allows Cencora to partially monetize MWI while maintaining continued economic exposure to the performance and growth of the merged entity through its retained ownership interest.

The combined company is expected to expand access and innovation across the animal health ecosystem by delivering timely and cost-effective solutions to veterinary practices and animal health professionals across companion and production animal markets. By integrating MWI’s supply chain strength with Covetrus’ pharmacy and practice management solutions, the platform aims to improve operational efficiencies and generate meaningful cost savings for veterinary professionals and pet owners.

Additionally, as manufacturers introduce new animal health products, the expanded platform is positioned to enhance end-user reach and product adoption, support launches across emerging customer channels, and better address the evolving needs of pet owners, veterinarians and producers.

The completion of the transaction remains subject to customary closing conditions, including the receipt of required regulatory approvals. Cencora also reaffirmed its fiscal 2026 financial guidance and noted that the outlook for the fiscal year ending Sept. 30, 2026, does not currently contemplate the closing of the transaction.

Favorable Industry Prospect for COR

Per a report by Grand View Research, the global animal health market size was valued at $62.89 billion in 2024 and is projected to reach $112.33 billion by 2030, expanding at a CAGR of 10.46%.

Market growth is being propelled by higher spending on animal healthcare, growing integration of artificial intelligence in diagnostics and practice management, and an evolving regulatory landscape. Additional drivers include the rising incidence of animal diseases, heightened concerns around zoonotic infections, strategic initiatives by leading companies, increasing adoption of pet insurance, and the ongoing trend of pet humanization.

Other News

Recently, COR reported fiscal first-quarter results that reflected a mixed performance, with earnings beating estimates while revenues were in line with expectations, and the fiscal 2026 revenue guidance exceeding the Zacks Consensus Estimate. The quarter was supported by broad-based growth across its healthcare solutions platforms and sustained demand for specialty products, including GLP-1 therapies. Although customer losses created some volume pressure, overall market growth and strong specialty demand helped offset the impact, aided by disciplined execution and operational efficiency.

COR’s Zacks Rank & Stocks to Consider

COR carries a Zacks Rank #3 (Hold) at present.

Some better-ranked stocks from the broader medical space are Intuitive Surgical ISRG, GE HealthCare Technologies GEHC and AtriCure ATRC.

Intuitive Surgical, sporting a Zacks Rank #1 (Strong Buy) at present, reported fourth-quarter 2025 adjusted earnings per share (EPS) of $2.53, beating the Zacks Consensus Estimate by 12.4%. Revenues of $2.87 billion surpassed the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

ISRG has an estimated long-term earnings growth rate of 15.7% compared with the industry’s 12.8% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 13.2%.

GE HealthCare Technologies, currently carrying a Zacks Rank #2 (Buy), reported fourth-quarter 2025 adjusted EPS of $1.44, which surpassed the Zacks Consensus Estimate by 0.7%. Revenues of $5.7 billion beat the Zacks Consensus Estimate by 1.9%.

GEHC has an estimated long-term earnings growth rate of 9.1% compared with the industry’s 13.4% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 7.5%.

AtriCure, currently carrying a Zacks Rank #2, reported a third-quarter 2025 adjusted loss per share of 1 cent, narrower than the Zacks Consensus Estimate by 90.9%. Revenues of $134.3 million beat the Zacks Consensus Estimate by 2.1%.

ATRC has an estimated earnings growth rate of 91.7% for 2026 compared with the industry’s 16.5% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 67.1%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cencora, Inc. (COR): Free Stock Analysis Report

AtriCure, Inc. (ATRC): Free Stock Analysis Report

GE HealthCare Technologies Inc. (GEHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).