Used vehicle e-retailer Carvana CVNA recently approved a 5-for-1 forward stock split, its first-ever stock split. Effective May 7, the shares will begin trading on a split-adjusted basis.

Stock splits don’t really change the underlying fundamentals of the company. It simply increases the number of shares outstanding while proportionally reducing the share price, improving liquidity and lowering the entry barrier for potential investors. Stock splits often signal management confidence in the company’s long-term outlook and occur after strong share-price appreciation. And this is true in Carvana’s case.

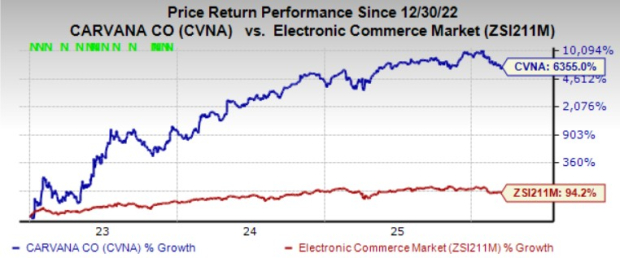

From being on the brink of collapse in 2022, Carvana has staged a remarkable turnaround thanks to successful debt restructuring and solid operational execution. And that’s being reflected in its share price. Since the beginning of 2023 to date, shares of CVNA have rocketed over 6,300%. It has handily outperformed its close peers like CarMax KMX and Sonic Automotive SAH. While CarMax has declined 31% over the same timeframe, Sonic has risen around 23%.

Carvana has made tangible progress on operational and financial fronts and is now the second-largest used car retailer in the United States. The stock split decision follows the company’s solid 2025 results, with record unit sales, revenues and profitability.

CVNA’s retail sales units in 2025 grew 43% year over year to 596,641, and revenues witnessed a year-over-year jump of 49% to more than $20 billion.

Adjusted EBITDA increased over 60% to $2.2 billion, with margins improving from 10.1% to 11% in 2025. Carvana’s cash from operating activities in 2025 was more than $1 billion, up from $918 million in 2024, signaling that the business is generating real cash.

While these numbers are impressive, the stock’s valuation is quite stretched (and won’t be affected by the stock split), suggesting much of the strong execution and growth potential is already priced into the stock. It carries a Value Score of D.

Carvana is trading at a forward sales multiple of 2.48X, way higher than SAH’s 0.13X and CarMax’s 0.23X.

CVNA Appears Overvalued

While this stock split announcement is a positive development, is it really a buy signal at current levels? Let’s unpack.

Carvana’s Growth Runway Remains Vast

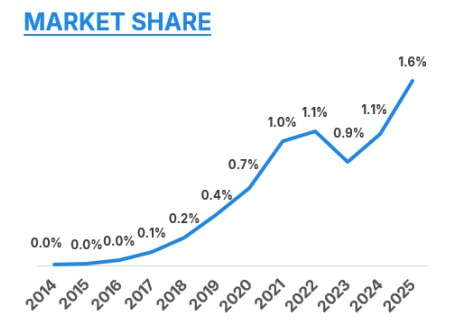

Carvana is now the second-largest used car retailer in the United States. Investors should note that the company holds just a 1.6% share of the highly fragmented U.S. automotive retail market. This suggests that there is ample room for the company to expand, especially as more consumers gravitate toward online car buying.

The company anticipates strong growth in retail unit sales for full-year 2026. It expects a sequential increase in retail unit sales in the first quarter of 2026.

Carvana’s next milestone goal is to sell 3 million vehicles annually, which is expected to increase its used car market share to 7.5%.

Importantly, the acquisition of ADESA’s U.S. operations has also strengthened Carvana’s position. ADESA adds scale to CVNA’s logistics, auction and reconditioning capabilities, improving both vehicle quality and throughput. With 34 reconditioning locations currently operational, the highest number in its history, Carvana has broadened its geographic reach. Expanding the ADESA Clear digital auction platform across more locations further ties wholesale expertise with Carvana’s differentiated digital-first business model.

Further, CVNA sees substantial fixed-cost leverage and fundamental improvements across the business. It has set an adjusted EBITDA margin goal of 13.5% by 2030 to 2035. This compares to the adjusted EBITDA margin of 11% in 2025.

The company anticipates strong growth in adjusted EBITDA for full-year 2026 and a sequential increase in the first quarter of 2026.

Reconditioning Costs Weigh on Near-Term Profitability

Despite its strong growth outlook, Carvana is facing some near-term operational pressures. One of the key concerns is the rise in reconditioning costs in the fourth quarter. The company also expects reconditioning costs to remain elevated in the first quarter of 2026.

Reconditioning — the process of preparing used vehicles for sale — is a critical part of Carvana’s operations. Part of the pressure appears tied to the company’s rapid expansion of its vehicle-preparation network. As Carvana adds new facilities and ramps up inventory, some of the newer sites are still working through early operational inefficiencies.

This pushed reconditioning expenses higher and weighed on profit per vehicle in the last reported quarter. While management believes these issues are temporary, it highlights how Carvana’s aggressive growth strategy can sometimes create short-term operational volatility.

What Do the Estimates Say for CVNA?

While the consensus estimate for Carvana’s 2026 revenues indicates a 33% year-over-year increase, its 2026 EPS is projected to decline 17%. EPS estimates for CVNA have also trended lower over the past 30 days.

Conclusion

Carvana has delivered one of the most striking turnarounds in the auto space, and its recent stock split reflects the strong momentum in both operations and investor sentiment. However, stock splits do not alter fundamentals, and CVNA’s premium valuation already factors in much of the company’s recovery and growth expectations.

At the same time, rising reconditioning costs and softening earnings estimates suggest that near-term execution risks remain. While the company’s long-term opportunity in the fragmented used-car market is compelling, the current risk-reward balance appears less attractive. As such, it’s advisable to wait for a better entry point instead of buying the stock now.

CVNA stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CarMax, Inc. (KMX): Free Stock Analysis Report

Sonic Automotive, Inc. (SAH): Free Stock Analysis Report

Carvana Co. (CVNA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).