McCormick & Company, Incorporated MKC reported first-quarter fiscal 2026 results, wherein both top and bottom lines beat the Zacks Consensus Estimate and increased year over year.

Adjusted earnings rose 10% to 66 cents per share from 60 cents in the year-ago quarter. The metric beats the Zacks Consensus Estimate of 61 cents per share. The increase was driven by elevated adjusted operating income.

McCormick & Company, Incorporated Price, Consensus and EPS Surprise

McCormick & Company, Incorporated price-consensus-eps-surprise-chart | McCormick & Company, Incorporated Quote

The global flavor leader generated net sales of $1,873.9 million, up 16.7% year over year, including a 3.1% positive currency impact. The top line beats the consensus mark of $1,786 million. The January 2026 acquisition of McCormick de Mexico contributed 13% to the overall sales growth. Organic sales edged up 1.2%, primarily driven by pricing actions.

MKC’s Quarterly Performance: Key Metrics & Insights

The adjusted gross margin expanded 100 basis points, driven by contributions from the McCormick de Mexico acquisition, pricing actions and cost savings from the company’s Comprehensive Continuous Improvement (“CCI”) program, partly offset by higher commodity costs.

Adjusted operating income increased to $268 million from $225 million, reflecting a 19% year-over-year rise, including a 3% favorable currency impact. On a constant currency basis, adjusted operating income grew 16%, supported by elevated gross profit and CCI-driven cost savings, including SG&A efficiencies. These gains were partially offset by higher SG&A expenses, primarily due to acquisition-related costs, continued brand marketing investments and increased technology spending.

Decoding MKC’s Segmental Performance

Consumer: The segment’s sales surged 25% year over year to $1,145 million, supported by a 20% contribution from McCormick de Mexico and a 3% positive currency impact. Organic sales in the segment increased 2%, led by pricing. Adjusted operating income rose 22% year over year to $180 million or 20% in constant currency, driven by higher gross profit, partially offset by increased SG&A investments in marketing and technology.

Flavor Solutions: Sales grew 6% year over year to $729 million, including a 3% favorable currency impact and a 2% contribution from McCormick de Mexico. Organic sales in the segment edged up 1%, driven by pricing. Adjusted operating income increased 12% to $88 million or 7% in constant currency, supported by higher gross profit but partly offset by elevated SG&A expenses, including continued investments in technology.

MKC’s Financial Health Snapshot

McCormick ended the quarter with cash and cash equivalents of $177.7 million, long-term debt of $3.60 billion and total shareholders’ equity of $7.56 billion.

In the three months ended Feb. 28, 2026, net cash provided by operating activities was $50.9 million. The company continues to expect robust cash generation for fiscal 2026, supported by profit and working capital initiatives, and aims to return a significant portion to its shareholders via dividends.

What to Expect From MKC in Fiscal 2026?

The company still expects net sales growth of 13-17% (while 12-16% in constant currency) in fiscal 2026, including an 11-13% contribution from the McCormick de Mexico acquisition in both reported and constant currency terms. Organic sales are projected to increase 1-3% on a constant currency basis.

Adjusted gross margin is expected to expand, implying recovery from 2025, with favorable impacts from organic sales growth, accretion from McCormick de Mexico and benefits from the company’s CCI program, partially offset by higher commodity costs. SG&A expenses are expected to be impacted by cost headwinds, including digital transformation initiatives, the build back of incentive compensation and continued growth investments. These impacts are expected to be partially offset by benefits from the company’s CCI program, including SG&A streamlining initiatives.

Adjusted operating income is projected to rise 16-20% (up 15-19% at constant currency).

The company expects adjusted EPS between $3.05 and $3.13, indicating 2-5% year-over-year growth or a 1-4% rise at constant currency.

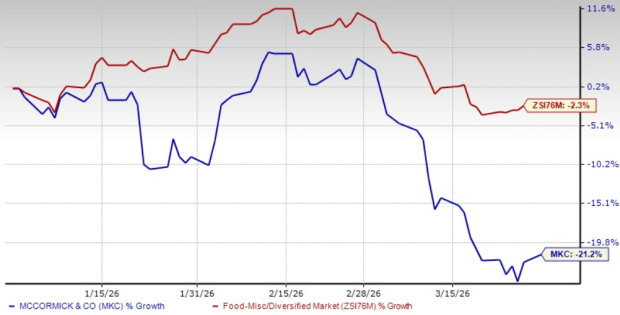

This Zacks Rank #3 (Hold) company has lost 21.2% in the past three months compared with the industry’s decline of 2.3%.

Image Source: Zacks Investment Research

Stocks to Consider

Mama's Creations, Inc. MAMA manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 39.9% and 44.4%, respectively, from the year-ago figures. Mama's Creations delivered a trailing four-quarter earnings surprise of 133.3%, on average.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It flaunts a Zacks Rank #1 at present. HSY delivered a trailing four-quarter earnings surprise of 17.2%, on average.

The Zacks Consensus Estimate for Hershey’s current financial-year sales and earnings indicates growth of 4.8% and 30.1%, respectively, from the prior-year reported levels.

US Foods Holding Corp. USFD engages in the marketing, sale and distribution of fresh, frozen and dry food and non-food products to foodservice customers in the United States. USFD currently carries a Zacks Rank #2 (Buy). US Foods Holding delivered a trailing four-quarter earnings surprise of 2.2%, on average.

The Zacks Consensus Estimate for US Foods Holding’s current fiscal-year sales and earnings implies growth of 5.4% and 20.9%, respectively, from the year-ago figures.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hershey Company (The) (HSY): Free Stock Analysis Report

McCormick & Company, Incorporated (MKC): Free Stock Analysis Report

US Foods Holding Corp. (USFD): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).