West Pharmaceutical Services WST recently expanded its Dublin facility with a new 165,000 square foot building, significantly boosting its contract manufacturing capacity. The move is aimed at supporting rising global demand for high-volume injectable therapies, particularly in fast-growing areas like diabetes and obesity.

The expansion strengthens West Pharmaceutical Services’integrated service offering under its West Vantage platform, enabling advanced drug handling, automation and end-to-end development support. This positions the company to better serve pharmaceutical partners while accelerating time-to-market for complex, high-demand therapies.

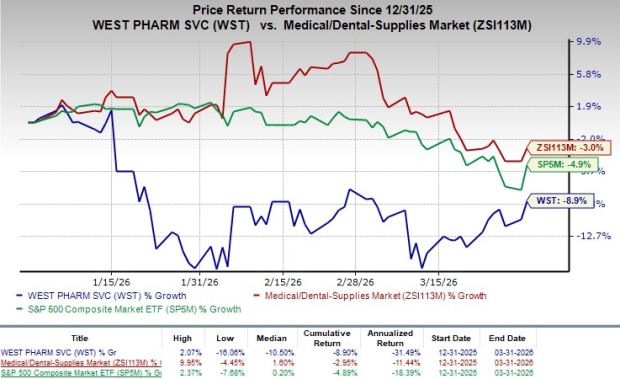

Likely Trend of WST Stock Following the News

Following the announcement, the company's shares gained 2.2% in yesterday’s trading session. In the year-to-date period, shares have lost 8.9% compared with the industry’s 3% decline. The S&P 500 has lost 4.9% over the same period.

The Dublin expansion strengthens West Pharmaceutical Services’ long-term growth by scaling its capacity in high-demand injectable segments like GLP-1 therapies for diabetes and obesity—one of the fastest-growing areas in pharma. By enhancing its end-to-end contract manufacturing capabilities under West Vantage, WST deepens integration with pharma clients, increases switching costs and secures recurring, high-margin revenue streams. This not only improves visibility on future demand but also positions the company as a critical supply chain partner, supporting sustained revenue growth and margin expansion over time.

WST currently has a market capitalization of $17.67 billion.

Image Source: Zacks Investment Research

More on the News

West Pharmaceutical Services has significantly expanded its Damastown, Dublin facility with the addition of a 165,000 square foot building, aimed at addressing the rapidly growing global demand for high-volume injectable therapies. The expansion is particularly aligned with surging needs in chronic disease segments such as diabetes and obesity, where next-generation GLP-1 treatments are driving substantial volume growth.

By increasing its global capacity for drug handling and delivery solutions, WST is reinforcing its role in ensuring reliability, quality and security of supply for pharmaceutical and biotechnology customers operating at scale.

Beyond incremental capacity, the new facility meaningfully enhances WST’s contract manufacturing capabilities by integrating advanced automation and commercial-scale drug handling into its existing offerings. The site now supports a broader range of services, including device assembly, component molding, packaging, analytical testing and regulatory support, all under its West Vantage platform.

This end-to-end, single-source model enables customers to streamline development and commercialization processes, reduce complexity and accelerate time-to-market. Strategically, the expansion strengthens West Pharmaceutical Services’positioning as a critical partner in the injectable drug delivery ecosystem, particularly as demand rises for complex biologics and high-volume therapies worldwide.Top of Form

Favorable Industry Prospect of WST

Per a report by Grand View Research, the global injectable drug delivery devices market size was valued at $467.5 billion in 2023 and is projected to reach $823.29 billion by 2030, expanding at a CAGR of 8.4% from 2024 to 2030.

The rising prevalence of chronic diseases and increasing technological advancements are driving demand for injectable drug delivery devices. Government initiatives for various injectable drugs for chronic diseases are further fueling the market growth.

Recent Developments by WST

Recently, West Pharmaceutical exited the fourth quarter of 2025 with better-than-expected results. Solid top-line results, along with improvements in organic revenues, were impressive. Robust performance by the Proprietary Products segment was encouraging. Strength in HVP and robust growth in the Biologics and Pharma market units during the reported quarter were also promising. Gross margin expansion and improving organic revenue trends reinforce confidence in the company’s execution capabilities.

WST’s management attributed the strong finish to 2025 to the consistent execution of its growth strategy. The HVP Components business within the Proprietary Products segment supported double-digit growth in adjusted earnings per share. The company expects momentum to carry into 2026, positioning the year as an important period for focused execution and operational discipline aimed at sustaining growth and enhancing long-term value for patients, customers and shareholders.

Bottom of Form

WST’s Zacks Rank & Other Key Picks

Currently, WST carries a Zacks Rank #2 (Buy).

Some other top-ranked stocks from the broader medical space are Phibro Animal Health PAHC, Intuitive Surgical ISRG and Cardinal Health CAH.

Phibro Animal Health, currently sporting a Zacks Rank #1 (Strong Buy), reported second-quarter fiscal 2026 adjusted earnings per share (EPS) of 87 cents, which surpassed the Zacks Consensus Estimate by 27.1%. Revenues of $373.9 million beat the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

PAHC has an estimated long-term earnings growth rate of 21.5% compared with the industry’s 12.4% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 20.1%.

Intuitive Surgical, carrying a Zacks Rank #2 at present, reported fourth-quarter 2025 adjusted EPS of $2.53, beating the Zacks Consensus Estimate by 12.4%. Revenues of $2.87 billion surpassed the Zacks Consensus Estimate by 4.7%.

ISRG has an estimated long-term earnings growth rate of 15.7% compared with the industry’s 13.6% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 13.2%.

Cardinal Health, currently carrying a Zacks Rank #2, reported a second-quarter fiscal 2026 adjusted EPS of $2.63, which surpassed the Zacks Consensus Estimate by 10%. Revenues of $65.6 billion beat the Zacks Consensus Estimate by 0.9%.

CAH has an estimated long-term earnings growth rate of 15% compared with the industry’s 9.2% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 9.3%.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).