International Business Machines Corporation IBM and Arista Networks, Inc. ANET are leading players in the enterprise IT infrastructure and are benefiting from the rise of AI (artificial intelligence) and cloud computing. IBM offers cloud and data solutions that aid enterprises in digital transformation. In addition to hybrid cloud services, the company provides advanced information technology solutions, computer systems, quantum computing and supercomputing solutions, enterprise software, storage systems and microelectronics.

On the other hand, Arista offers one of the broadest product lines of data center and campus Ethernet switches and routers in the industry. It provides routing and switching platforms with industry-leading capacity, low latency, port density and power efficiency.

With a focus on hybrid cloud and AI, both IBM and Arista are strategically positioned in the cloud infrastructure market, with overlapping presence in networking infrastructure, enterprise IT solutions and cloud/data-center ecosystems. Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

The Case for IBM

IBM is poised to benefit from healthy demand trends for hybrid cloud and AI, which drive the Software and Consulting segments. The company’s growth is expected to be aided by analytics, cloud computing and security in the long term. With a surge in traditional cloud-native workloads and associated applications, along with a rise in generative AI deployment, there is a radical expansion in the number of cloud workloads that enterprises are currently managing. This has resulted in heterogeneous, dynamic and complex infrastructure strategies, which have led firms to undertake a cloud-agnostic and interoperable approach to highly secure multi-cloud management, translating into a healthy demand for IBM hybrid cloud solutions.

In addition, the buyout of HashiCorp has significantly augmented IBM’s capabilities to assist enterprises in managing complex cloud environments. HashiCorp’s tool sets complement IBM Red Hat’s portfolio, bringing additional functionalities for cloud infrastructure management and bolstering its hybrid multi-cloud approach.

Despite solid hybrid cloud and AI traction, IBM is facing stiff competition from Amazon.com, Inc.’s AMZN AWS and Microsoft Corporation’s MSFT Azure. Increasing pricing pressure is eroding margins, and profitability has trended down over the years, barring occasional spikes. The company’s ongoing, heavily time-consuming business model transition to the cloud is a challenging task. Weakness in its traditional business and foreign exchange volatility remain significant concerns.

The Case for Arista

Arista holds a leadership position in 100-gigabit Ethernet switches and is increasingly gaining market traction in 200- and 400-gigabit high-performance switching products. It is witnessing solid demand trends among enterprise customers backed by its multi-domain modern software approach, which is built upon its unique and differentiating foundation, the single EOS (Extensible Operating System) and CloudVision stack. Arista has made several additions to its multi-cloud and cloud-native software product family with CloudEOS Edge. It has introduced new cognitive Wi-Fi software that delivers intelligent application identification, automated troubleshooting and location services. The versatility of Arista’s unified software stack across various use cases, including WAN routing, campus and data center infrastructure, sets it apart from other competitors in the industry.

In addition to high capacity and easy availability, its cloud networking solutions promise predictable performance and programmability, enabling integration with third-party applications for network management, automation and orchestration. The company boasts a comprehensive portfolio with the right network architecture for client-to-campus data center cloud and AI networking, backed by three guiding principles. These include best-in-class, highly proactive products with resilience and zero-touch automation, with predictive client-to-cloud one-click operations with granular visibility and prescriptive insights for deeper AI algorithms. Arista is likely to benefit from its software-driven, data-centric approach, which helps customers build their cloud architecture and enhance the cloud experience they offer their clients.

However, Arista remains plagued by high operating costs. Total operating expenses in the fourth quarter of 2025 increased around 23.1% to $530.9 million, owing to higher headcount, new product introduction costs and higher variable compensation expenditures. Moreover, the redesigning of products and their supply chain mechanism has eroded margins. Research & development costs rose to $348.4 million from $285 million. Lingering supply bottlenecks for advanced products, a concentrated customer base and stiff competition from other networking & cloud native infrastructure vendors are other headwinds for ANET.

How Do Zacks Estimates Compare for IBM & ANET?

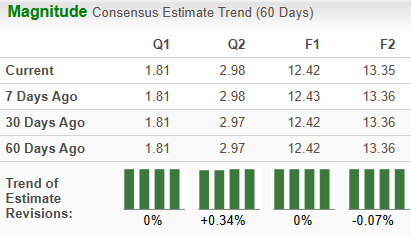

The Zacks Consensus Estimate for IBM’s 2026 sales and EPS implies year-over-year growth of 5.3% and 7.2%, respectively. The EPS estimates have remained static over the past 60 days.

Image Source: Zacks Investment Research

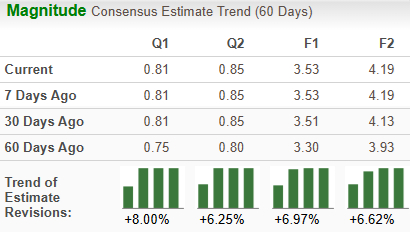

The Zacks Consensus Estimate for Arista’s 2026 sales and EPS implies year-over-year growth of 25% and 18.5%, respectively. The EPS estimates have trended up 7% over the past 60 days.

Image Source: Zacks Investment Research

Price Performance & Valuation of IBM & ANET

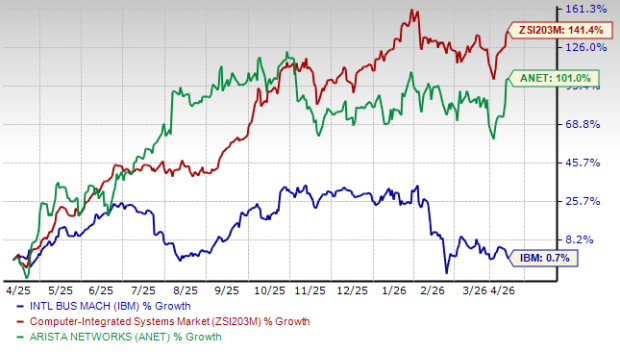

Over the past year, IBM has gained 0.7% compared with the industry’s growth of 141.4%. ANET has surged 101% over the same period.

Image Source: Zacks Investment Research

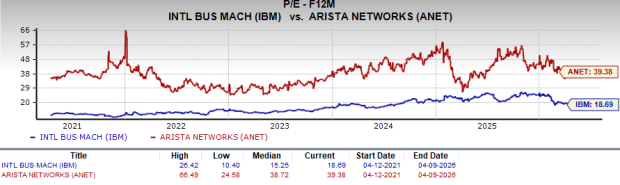

IBM looks more attractive than Arista from a valuation standpoint. Going by the price/earnings ratio, IBM’s shares currently trade at 18.69 forward earnings, significantly lower than Arista’s 39.38.

Image Source: Zacks Investment Research

IBM or ANET: Which is the Better Pick?

Both IBM and Arista carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both companies expect their sales and profits to improve in 2025. Arista has a better price performance and better estimate revisions compared with IBM, although it is a bit expensive in terms of the valuation metric. Arista has shown steady revenue and EPS growth for years, while IBM has been facing a bumpy road. Investors looking for the "next wave" in AI and cloud infrastructure may lean toward Arista, while those seeking a broad, resilient tech play may favor IBM. Although there is not much to choose from, based solely on the emerging growth opportunities in AI and cloud infrastructure, Arista seems to hold a slight edge and appears to be a better investment option at the moment.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

International Business Machines Corporation (IBM): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).