Applied Digital APLD shares are down 5.5% since the company reported its third-quarter fiscal 2026 results on April 8, 2026. The decline is notable given that revenues of $126.6 million surged 139.3% year over year, beating the Zacks Consensus Estimate by 68.73%. The decline reflects growing unease over the gap between top-line momentum and underlying profitability.

Adjusted revenues reached $108.6 million, and adjusted EBITDA improved 7x year over year to $44.1 million. However, APLD reported a loss of 36 cents per share in the third quarter of fiscal 2026, suggesting that the adjusted picture and the reported reality remain far apart. A substantial portion of adjusted revenues was driven by tenant fit-out services, a nonrecurring line item contributing $18.9 million at margins of roughly 5%. Core base rent of $44.1 million reflects only one operational 100-megawatt building at Polaris Forge 1, meaning the earnings trajectory remains heavily dependent on completing and contracting the broader construction pipeline before it can be considered durable at scale.

APLD's Execution and Capital Intensity Create Near-Term Pressure

APLD is simultaneously building large-scale capacity across Polaris Forge 1, Polaris Forge 2 and Delta Forge 1, making execution the key swing factor in the near term. The model hinges on converting construction-phase assets into stabilized, rent-generating operations, but that transition remains incomplete. Any delays in energizing additional buildings or slower lease conversion across campuses could push out operating leverage and keep earnings volatile.

The cost structure is scaling ahead of revenues. Selling, general and administrative expenses rose 251% year over year to $79.7 million in the fiscal third quarter, driven by higher stock-based compensation and expansion-related overhead. This reflects a business still in build mode, where recurring base rent has yet to catch up with the cost base. Capital intensity remains elevated, with nearly a gigawatt under construction. Total debt stands at $2.7 billion against $2.1 billion in cash, while the recent $2.15 billion in 6.75% senior secured notes issued for Polaris Forge 2 adds fixed obligations ahead of the revenue ramp. With additional financing still required for Polaris Forge 1, balance sheet pressure is likely to persist.

The Zacks Consensus Estimate for APLD's fiscal 2026 loss has been revised upward by 4 cents over the past 30 days to 35 cents per share. The estimate still marks a meaningful improvement from the fiscal 2025 reported loss of 85 cents per share.

Applied Digital Corporation Price and Consensus

Applied Digital Corporation price-consensus-chart | Applied Digital Corporation Quote

APLD Faces Concentration Risk and Pipeline Uncertainty

APLD's revenue base remains highly concentrated, limiting near-term visibility. CoreWeave CRWV accounts for roughly $11 billion of approximately $16 billion in total contracted revenue, nearly 69% of the contracted base and the fully leased capacity at Polaris Forge 1. While recent credit enhancements tied to CoreWeave's refinancing improve counterparty quality, reliance on a single hyperscaler relationship continues to elevate risk.

The growth pipeline is also still transitioning from contracted potential to realized revenue. Polaris Forge 2 is leased to an investment-grade hyperscaler, but 100 megawatts at the campus remains uncontracted and meaningful contribution will only begin once facilities turn operational. Additional campuses remain in negotiation, creating uncertainty around timing and conversion into stable lease income. Unlike peers such as Riot Platforms RIOT and Equinix EQIX, which generate revenues across multiple customers and benefit from more diversified and predictable income streams, APLD's earnings visibility remains largely dependent on a single tenant relationship at this stage. Until APLD expands beyond CoreWeave and builds multiple concurrent revenue streams, its growth story remains exposed to concentration risk and pipeline timing uncertainty.

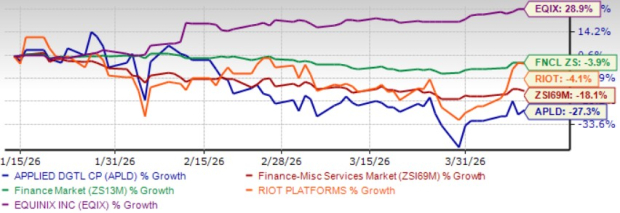

APLD Shares Remain Under Pressure

APLD has plunged 27.3% over the past three months, underperforming the Zacks Finance-Miscellaneous Services industry, which has declined 18.1%, and the Zacks Finance sector, which has slipped 3.9%. The relative weakness is starker against peers Riot Platforms and Equinix. Equinix shares have appreciated 28.9% over the same period, while Riot Platforms has declined a modest 4.1%, suggesting that APLD's drawdown reflects company-specific execution concerns rather than broader market pressure.

APLD’s 3-Month Price Return Performance

Image Source: Zacks Investment Research

APLD Faces Premium Valuation

APLD shares are overvalued, as suggested by the Value score of F. The stock trades at a forward 12-month price-to-sales of 11.47x, a premium versus the industry average of 2.68x and the sector average of 8.28x. For a business still in execution mode, heavily dependent on a single tenant in CoreWeave and with recurring base rent yet to scale meaningfully across its campus pipeline, sustaining this premium is difficult to justify at current levels.

APLD’s P/S Valuation

Image Source: Zacks Investment Research

Conclusion

Despite the growth push, APLD's path to profitability remains long and uncertain. Rising costs, a heavily leveraged balance sheet, single-tenant dependence on CoreWeave and an unproven pipeline across new campuses present meaningful near-term risks. Estimate revisions are moving downward, and the stock's stretched valuation makes it a difficult proposition at current prices.

APLD currently carries a Zacks Rank #5 (Strong Sell), suggesting that investors should stay away from the stock for now.

You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Equinix, Inc. (EQIX): Free Stock Analysis Report

Riot Platforms, Inc. (RIOT): Free Stock Analysis Report

Applied Digital Corporation (APLD): Free Stock Analysis Report

CoreWeave Inc. (CRWV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).