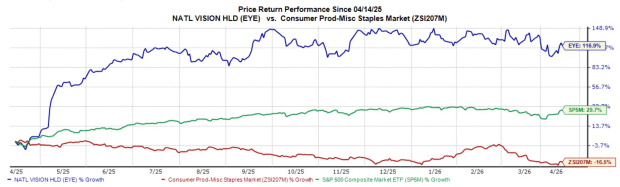

National Vision EYE has witnessed strong momentum over the past year. Shares of the company have risen 116.9%, outperforming the industry’s 16.5% decline. The S&P 500 composite has increased 29.7% during the same time frame.

With healthy fundamentals and strong growth opportunities, this Zacks Rank #3 (Hold) company appears to be a solid wealth creator for its investors at the moment.

National Vision is a major optical retailer in the United States. As of 2025, the company operated through a diverse portfolio of 1,250 retail stores across four brands, along with associated omnichannel consumer websites. National Vision operates through one reportable segment, Owned & Host, which includes two owned brands — America’s Best Contacts and Eyeglasses (America’s Best) and Eyeglass World.

Factors Favoring EYE’s Share Price Growth

National Vision’s share price is trending upward, prompted by its ongoing strategic transformation. The strategy focuses on four growth areas. In 2025, National Vision targeted underserved segments like managed care users and progressive lens wearers, boosting traffic. It also expanded premium and branded products, increasing sales and attracting higher-income customers, with strong performance from smart glasses and advanced lenses.

EYE is using data-driven segmentation to improve customer experience, personalize marketing and enhance sales practices, while leveraging its optometry network and technology to support steady expansion into new markets and formats.

In 2026, the company plans to open approximately 30 to 35 new stores, primarily comprising America’s Best locations, before returning to its more typical store opening cadence as strategic initiatives begin to take hold. New store openings are expected to remain a key driver of growth in net revenues and operating profit.

Investors are currently focused on the company’s strong market share gain in the Owned & Host segment. The segment continues to gain from positive comparable store sales growth and new store openings. Of the two Owned brands, America’s Best remains the primary revenue driver.

In the fourth quarter of 2025, adjusted comparable store sales growth was 4.8%. Remote exam technology remains central to National Vision’s ability to deliver care at scale. The company is making progress with its remote hybrid model, where in-store doctors also perform exams in other stores remotely. The program continues to expand, with more doctors being trained and participating.

National Vision’s 2026 outlook looks encouraging. Net revenues are projected to be in the range of $2.033-$2.091 billion. Adjusted EPS is estimated to be between 85 cents and $1.09.

Image Source: Zacks Investment Research

Factors That May Offset EYE’s Gains

EYE’s business remains vulnerable to growing geopolitical complexities, supply-chain disruptions, shortages of healthcare staff and volatility in capital markets. Additionally, the ongoing changes in U.S. trade policy and retaliatory tariffs look discouraging. All these factors continue to weigh on its profitability. In the fourth quarter of 2025, SG&A expenditures rose 12.1% year over year.

From a solvency viewpoint, National Vision has a significant amount of indebtedness. It exited the fourth quarter of 2025 with cash and cash equivalents of $39 million and short-term debt of $17 million. Long-term debt was $229 million, much higher than cash levels. This leverage could have several consequences, including greater exposure to adverse economic, industry or competitive developments.

A Look at EYE’s Estimates

The Zacks Consensus Estimate for 2026 EPS has remained unchanged at 93 cents in the past 30 days.

The company has an estimated long-term EPS growth rate of 20.1% compared with the industry’s 10.4%.

Stocks to Consider

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Alcon ALC and Phibro Animal Health PAHC.

Globus Medical has an earnings yield of 4.9%, well ahead of the industry’s -0.7% yield. Its earnings surpassed estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 18.8%. The company’s shares have rallied 22.3% against the industry’s 3.8% decline over the past year.

GMED sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

ALC, carrying a Zacks Rank #2 (Buy) at present, has an earnings yield of 4.4% against the industry’s -1.1% yield. Shares of the company have lost 13.9% against the industry’s 2.3% growth. ALC’s earnings topped estimates in two of the trailing four quarters and missed in the other two, the average surprise being 1.1%.

Phibro Animal Health, carrying a Zacks Rank #2 at present, has an earnings yield of 6.1% compared with the industry’s 2.6% yield. Shares of the company have climbed 130.6% against the industry’s 17.9% decline. PAHC’s earnings beat estimates in each of the trailing four quarters, the average surprise being 20.2%.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Alcon (ALC): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

National Vision Holdings, Inc. (EYE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).