OptimizeRx OPRX closed 2025 on a high, but its revised 2026 outlook reflects emerging near-term headwinds. The company expects 2026 revenues of $109-$114 million compared with the $118-$124 million provided at the end of the third quarter of 2025. Revenues for 2025 grew 19% to $109.4 million.

Softness in contracted revenues, linked to a broader market shift away from managed services, is an overhang. Management noted that the first half of 2025 saw $9 million higher managed services revenues, which are not expected to repeat this time around.

Volatility is increasing as pharmaceutical clients adopt a more conservative spending approach amid Most Favored Nation (“MFN”) pricing dynamics. However, OptimizeRx emphasized that this appears temporary. Management noted that it continues to see strong engagement across its network and is confident that the demand trends will cushion the business. It expects normalization over the coming quarters.

Despite the lower revenue outlook, profitability remains a key strength. OptimizeRx reiterated its focus on adjusted EBITDA, guiding $21-$25 million for 2026. This is more than the previously mentioned $19-$22 million. In addition to a fixed cost base and scalable operating model, EBITDA is gaining from cost discipline measures (post the Medicx buyout).

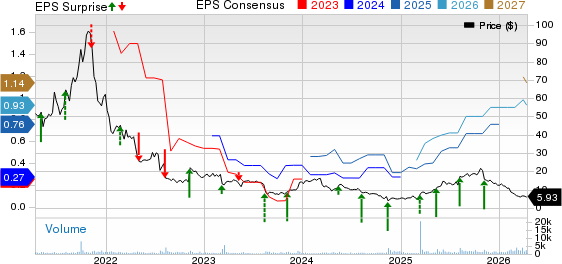

OptimizeRx Corp. Price, Consensus and EPS Surprise

OptimizeRx Corp. price-consensus-eps-surprise-chart | OptimizeRx Corp. Quote

Over the long term, the expanding adoption of OPRX’s Dynamic Audience Activation Platform (DAAP) is expected to support top-line growth. The DAAP platform offers predictive and secure marketing solutions, which connect patients, HCPs and life sciences across a strong network of clinical and personal platforms.

On the last reported quarter’s earnings call, OPRX noted that its engagement with established clients remains strong while it is adding more customers, especially in the mid-tier and long-tail life science companies. Management views this segment as highly attractive.

The company addressed AI concerns, positioning it as a tailwind rather than a disruption risk, highlighting that AI is expected to free up marketing budgets, which are usually allocated up to 50% to content creation. These could be reallocated toward marketing execution and audience reach, areas where OptimizeRx shines, as highlighted by management.

Let’s Look at the Guidance of Competitors

GoodRx Holdings, Inc. GDRX is another digital healthcare company focused on medication savings in the United States and is used by nearly 25 million consumers. For 2026, the company expects revenues of $750-$780 million, implying a decline of 2-6% from the $796.9 million reported in 2025.

Adjusted EBITDA is expected to be at least $230 million, suggesting a 15% decline from the $270.5 million reported in 2025. This signals meaningful margin pressure as the company ramps up investments in the Pharma Direct business and subscription offerings. Lower prescription transaction revenues are concerning (down 6% in 2025 to $544 million), which is expected to remain under pressure in 2026.

Phreesia PHR lowered its revenue guidance for fiscal 2027. It expects $510 million to $520 million, down from the prior mentioned $545 million to $559 million. Management noted that the downgrade was primarily due to reduced visibility into spending commitments from pharmaceutical manufacturers. PHR is witnessing lower-than-anticipated committed spending from network solutions clients for the second half of fiscal 2027, increasing variability in forecasting.

However, management added that it did not consider this a structural shift in demand for its solutions. Other parts of the business are tracking in line with prior expectations. Phreesia is maintaining its adjusted EBITDA guidance of $125 million to $135 million, even with a reduced revenue outlook.

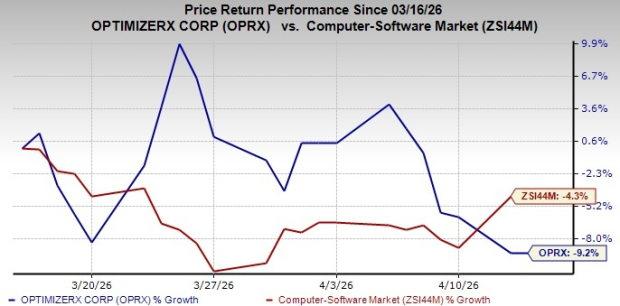

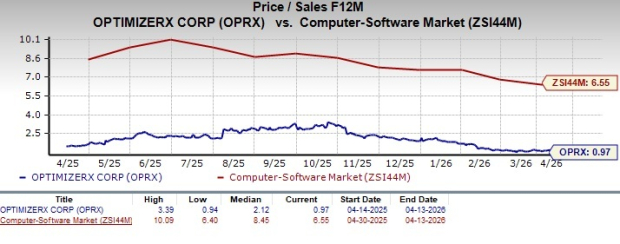

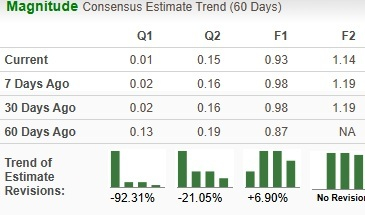

OPRX Price Performance, Valuation & Estimates

Shares of OptimizeRx have lost 9.2% in the past month compared with the Computer Software industry’s decline of 4.3%.

Image Source: Zacks Investment Research

Regarding the forward 12-month price/sales ratio, OPRX is trading at 0.97, lower than the sector’s multiple of 6.55.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for OPRX’s earnings for fiscal 2027 has been revised upward over the past 60 days.

Image Source: Zacks Investment Research

OPRX currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

OptimizeRx Corp. (OPRX): Free Stock Analysis Report

Phreesia, Inc. (PHR): Free Stock Analysis Report

GoodRx Holdings, Inc. (GDRX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).