Blue Owl Capital Inc. OWL offers a standout income profile, with a 90 cents per share annual dividend that equates to roughly a 10.65% yield. The company most recently declared a quarterly dividend of 22.5 cents per Class A share.

Image Source: Zacks Investment Research

Nonetheless, this income appeal comes with real price damage. The stock is down 51.9% over the past year. The setup now is a balancing act between a high yield and near-term business-model headwinds that have pressured sentiment.

Blue Owl’s Stock Signals Remain Weak Near Term

For investors focused on the next one to three months, OWL carries a Zacks Rank #5 (Strong Sell). Its Style Scores reinforce the caution: Momentum is an “F” and the VGM Score is “C.”

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

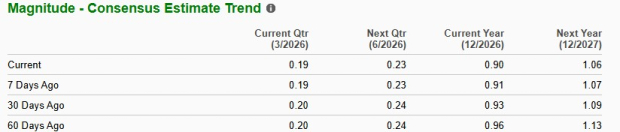

This typically signals that the path of least resistance remains lower near term, especially when estimate revisions are drifting down. OWL’s 2026 earnings estimates have been revised lower in the past weeks, and the stock has lagged its industry over the last six months.

Image Source: Zacks Investment Research

That does not invalidate the income story, but it raises the bar for timing. When momentum is weak, buyers often need a clearer catalyst, such as stabilization in flows or firmer earnings-quality trends, to shift the narrative.

OWL’s Valuation Discount vs. Peers and the Market

The recent selloff has pushed OWL to a discounted valuation versus key benchmarks. The stock trades at about 8.91X forward 12-month earnings, versus 13.20X for the industry.

Image Source: Zacks Investment Research

The discount also stands out against Blue Owl’s own history. Over the past three years, the stock has traded as high as 30.26X and as low as 8.67X, with a three-year median of 19.24X. This puts the current multiple near the bottom of the range.

Blue Owl’s Cash Engine: Fee-Related Earnings Profile

Blue Owl’s earnings model is built around management fees, with permanent capital vehicles providing durability. About 85% of management fees were earned from permanent capital vehicles as of Dec. 31, 2025. This structure supports fee visibility, but the margin story still matters.

In 2025, GAAP revenue rose 25% year over year to $2.87 billion, while GAAP diluted earnings per share fell to 10 cents from 20 cents in 2024. On a non-GAAP basis, Fee-Related Earnings (FRE) rose 19% to $1.50 billion and Distributable Earnings increased 16% to $1.31 billion.

In 2025, FRE margin was 58.3% down from 59.4% in 2024, reflecting higher compensation and non-compensation expenses tied to platform and distribution investments. Management expects FRE margin of 58.5% in 2026, a marginal improvement that would help validate the fee engine even if GAAP results remain noisy.

OWL Fundraising and AUM Growth Support the Long View

Despite near-term concerns in private credit, Blue Owl’s longer-run growth markers remain constructive. The firm raised $42 billion in 2025, up from $27.5 billion in 2024 and $15.4 billion in 2023. Further, management expects 2026 fundraising to look broadly similar to 2025 level.

Assets under management (AUM) reached $307.4 billion at year-end 2025, up 22% year over year, and fee-paying AUM rose 17% to $187.7 billion.

Additionally, Blue Owl ended 2025 with $28.4 billion of assets not yet paying fees, which are expected to translate into more than $325 million of annual management fees once deployed. That embedded ramp is a key pillar of the longer-view thesis.

Management is also leaning into scaling evergreen wealth products and planned product cycles. As those channels broaden, the opportunity is for a steadier cadence of fee realization once deployment normalizes.

Blue Owl’s Risks to Watch Before Buying

Income investors should keep a tight checklist on the risks that could undermine fee stability. First is private-credit liquidity and sentiment risk in retail-oriented, semi-liquid vehicles, where elevated redemptions can pressure flows and fundraising. Blue Owl restricted withdrawals at Blue Owl Capital Corporation II as requests hit the 5% threshold and sold assets across affiliated funds to meet liquidity needs.

Second is deployment timing. Management cited $28.4 billion of assets not yet paying fees at year-end 2025, but fee realization depends on closing activity and capital being put to work across strategies. Any elongation can defer the fee ramp.

Third is borrower-quality risk, particularly in software and AI-adjacent private-credit exposures, where weaker fundamentals can translate into higher downgrade and restructuring risk. Finally, elevated expenses and only modest operating leverage expectations can limit bottom-line progress even as revenues grow.

Where the Buy Case Could Strengthen for OWL

For the risk-reward to improve, the clearest positive is expected to be the smoother deployment of non-fee-paying assets into fee-paying status, turning embedded pipelines into realized management fees. A second unlock would be reduced redemption pressure and improved investor confidence in semi-liquid private-credit products, which would help protect fundraising momentum.

The third is operating discipline. If revenue growth can consistently outpace expenses, it would support better earnings quality and improve the credibility of margin leverage beyond near-term volatility.

Income seekers can also keep an eye on alternatives peers such as Apollo Global Management Inc. APO and Blackstone Inc. BX. Both APO and BX show lower dividend yields compared with OWL, but each carries a Zacks Rank #3 (Hold), suggesting a steadier near-term setup than OWL’s current profile.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Blackstone Inc. (BX): Free Stock Analysis Report

Apollo Global Management Inc. (APO): Free Stock Analysis Report

Blue Owl Capital Inc. (OWL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).