CoreWeave (CRWV) continues to receive analyst attention after gaining over 46% in the last month. Most recently, it was Macquarie who upgraded the stock from “Neutral” to “Outperform,” mainly on the back of the company’s recent agreements with Meta Platforms (META) and Anthropic. The research house also increased its price target on the stock from $90 to $125.

Last week, Anthropic disclosed that it was going to lease CoreWeave’s data center capacity in a multi-year deal. Just a day before this, the company had already announced the much-talked-about $21 billion deal with Meta.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Analysts now believe that CoreWeave is an integral part of the AI ecosystem as hyperscalers continue to diversify their compute capacity to reduce reliance on any single party. They believe that the pursuit of AGI will ensure there is ample demand for compute capacity once the time comes to extend these deals, giving companies like CoreWeave a solid position in the industry.

About CoreWeave Stock

CoreWeave is a software infrastructure company that offers the CoreWeave Cloud platform to deliver the automation & efficiency needed to manage AI infrastructure at scale. The company also provides storage solutions, mission control services, infrastructure control solutions, runtime acceleration, and others. It was founded by Michael Intrator, Brian Venturo, and Brannin McBee in 2017.

CRWV stock has significantly outperformed the S&P 500 Index ($SPX) over the past year. While the index delivered returns of around 30%, the stock generated gains roughly five times higher during the same time. So far this year, the stock is closing in on 70% gains.

www.barchart.com

www.barchart.com The company’s valuation does not currently concern investors, as it is seen as a company about to be deeply embedded in the AI ecosystem with immense growth potential. It therefore comes at a high risk with hardly any margin of safety. To secure deals like the one with Meta, the company is racking up debt at an incredible pace, currently at $29.82 billion against cash of just $3.16 billion. A three-year revenue growth rate of 596% may alleviate some of the concerns, but a change in plan by hyperscalers or the emergence of a better technology to manage compute elsewhere could send the stock crashing.

CoreWeave Announces Impressive Guidance

The company posted its Q4 FY 2025 results on Feb. 26. CoreWeave reported fourth-quarter revenue of $1.6 billion with full-year revenue of approximately $5.1 billion. For Q4, operating expenses reached $1.7 billion, which included $157 million in stock-based compensation. Adjusted operating income totaled $88 million, while the company reported a net loss of $452 million for the quarter.

Based on the guidance, 2026 revenue is expected to be in the range of $12 billion and $13 billion. Adjusted operating income for 2026 is projected to be between $900 million and $1.1 billion. The company plans to more than double its active power capacity to over 1.7 gigawatts by year-end, with capital spending expected to range from $30 billion to $35 billion. It is this incredible capital spending that adds the risk to an otherwise attractive investment.

What Are Analysts Saying About CRWV Stock?

Based on a report released on April 13, Bank of America Securities analyst Tal Liani reaffirmed a “Buy” rating on CRWV stock while increasing the firm’s price target from $100 to $120. According to the BofA analysts, recent contracts secured by CoreWeave and Nebius support a positive outlook for AI infrastructure demand. BofA also increased its revenue growth forecasts for CoreWeave, now projecting 94% growth in FY27 and 50% in FY28.

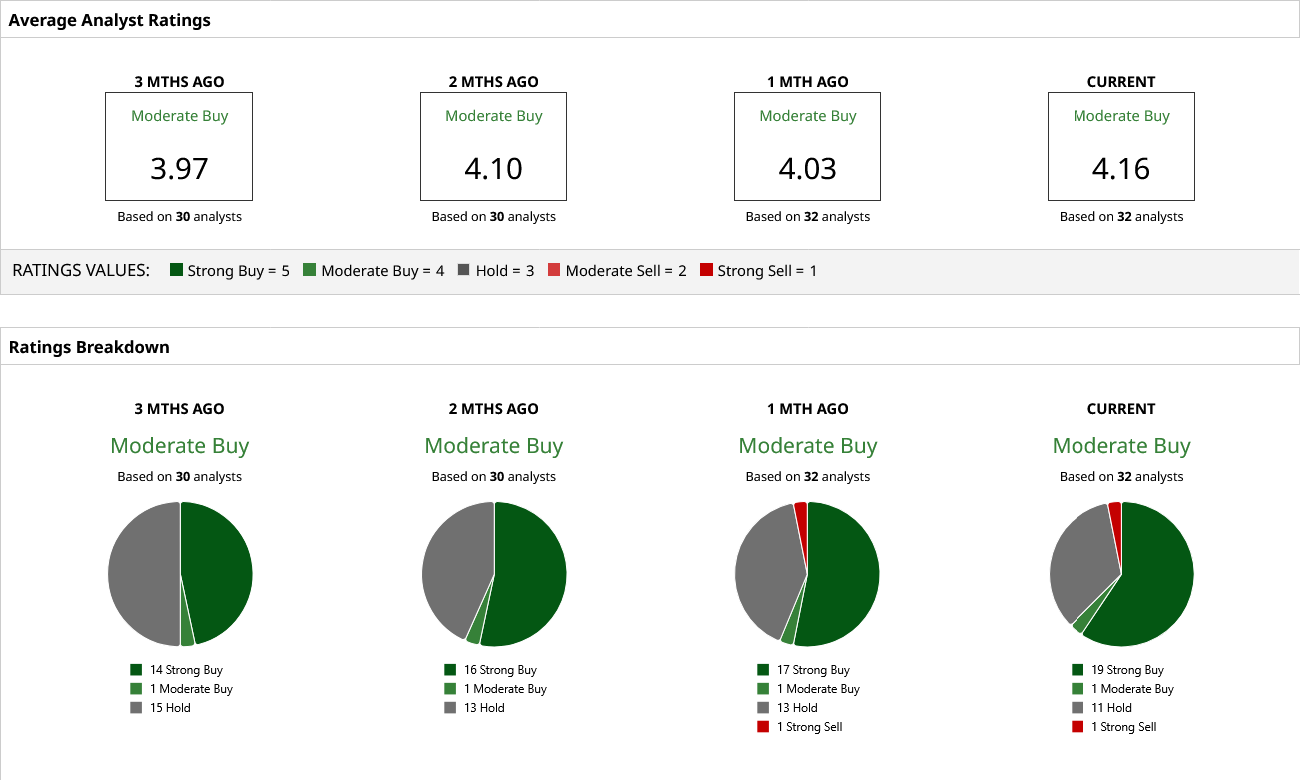

Based on 32 Wall Street analyst forecasts, CRWV stock has a consensus “Moderate Buy” rating. The most bullish analyst forecast suggests that the stock could rise to $180, reflecting an impressive upside of approximately 52%.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Macquarie Is Pounding the Table on CoreWeave Stock with a New ‘Outperform’ Rating. Should You Buy Here? Tesla Is Still a ‘Leader in Physical AI’ and You Should Buy TSLA Stock Now, Says UBS Turbine Season for Tech: John Rowland on the Next Era of AI Data Center Investments IonQ's DARPA Contract Win Makes It the Quantum Computing Stock to Own in 2026