Becton, Dickinson and Company BDX is benefiting from its focused transformation into a pure-play MedTech company, supported by strong execution of its BD 2025 strategy. The company’s continued emphasis on innovation, strategic partnerships and solid first-quarter results is driving optimism. However, persistent reimbursement uncertainties remain a key concern.

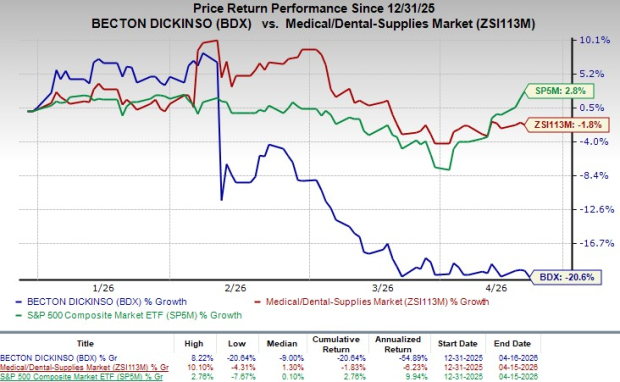

This Zacks Rank #3 (Hold) stock lost 20.6% in the year-to-date period compared with the industry’s 1.8% decline. The S&P 500 Composite has increased 2.8% during the same time frame.

The renowned medical technology player, with a market capitalization of $44.3 billion, remains focused on delivering durable growth and margin expansion. It projects 9.48% growth for the next fiscal year and expects to maintain a strong performance in the future. BDX’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, delivering an average surprise of 3.49%.

Image Source: Zacks Investment Research

Reasons Favoring BDX’s Growth

Continued Focus on R&D: BDX continues to prioritize innovation-led growth through sustained investments in R&D, clinical development and regulatory capabilities, enabling a steady pipeline of new product launches. The company leverages a global R&D footprint spanning North America, Asia and Europe, supported by collaborations with academic institutions, healthcare organizations and specialized partners, to accelerate product development and strengthen its competitive positioning.

Recent initiatives underscore this focus, including a feasibility collaboration with Envetec on recycling medical plastics, a $110 million investment to expand prefillable syringe capacity to support biologics and GLP-1 therapies and the expanded European use of Phasix Mesh in high-risk surgical procedures—collectively reinforcing BDX’s innovation depth, supply resilience and long-term growth potential.

Strategic Deals: BDX has been actively strengthening its strategic positioning through a series of partnerships and portfolio moves. The completion of its Biosciences & Diagnostic Solutions spin-off and combination with Waters represents a key milestone in its BD 2025 strategy, positioning the company as a focused pure-play MedTech player.

At the same time, BDX is expanding its innovation ecosystem through collaborations, such as its partnership with Ypsomed to develop next-generation prefillable syringe solutions, along with research alliances like the University of Pennsylvania to advance immune profiling. Additionally, the company’s collaboration with ChemoGLO enhances capabilities in hazardous drug detection and healthcare safety, collectively supporting long-term growth and competitive strength.

Strong Q1 Results: BD exited the first quarter of fiscal 2026 with better-than-expected results, along with a solid top-line performance. Robust performances by the majority segments and both geographic regions on a reported basis were encouraging. The expansion of both margins bodes well.

Apart from these, there were a few other developments during the recent period. BD announced a collaboration that allows facilities to combine rapid, point-of-care qualitative results from the BD HD Check System with ChemoGLO's LC-MS/MS analysis to expand hazardous drug contamination testing for health care facilities and laboratories and an expanded partnership with Ypsomed to address the rapidly growing biologics market through development of a 5.5 mL version of the BD Neopak XtraFlow Glass Prefillable Syringe that is designed to be fully compatible with Ypsomed's YpsoMate 5.5 autoinjector platform.

The company also expanded the PureWick portfolio with the PureWick Portable Collection System. It also announced the expansion of the BD Surgiphor Surgical Wound Irrigation System to Europe to help hospitals improve patient safety. These raise our optimism about the stock.

A Factor That May Offset BDX’s Gains

Reimbursement Practices: BDX’s sales and market access are significantly influenced by reimbursement dynamics and health insurance coverage, which vary across regions and directly impact product adoption, pricing and demand. Increasing scrutiny from third-party payers, along with adverse reimbursement decisions, may limit coverage for procedures involving its products, while ongoing cost-containment pressures and budget constraints among healthcare providers could shift demand toward lower-cost alternatives.

Additionally, government-led measures such as value-based payment reforms, competitive bidding, pricing regulations and evolving healthcare policies (including Medicare and Medicaid changes) are likely to add further uncertainty, potentially weighing on demand, pricing and overall financial performance.

Estimate Trend

BD is witnessing a negative estimate revision trend for fiscal 2026. In the past 30 days, the Zacks Consensus Estimate for its earnings has moved south by 33 cents to $12.55 per share.

The Zacks Consensus Estimate for the company’s second-quarter fiscal 2026 revenues is pegged at $4.67 billion, indicating an 11.4% decline from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks from the broader medical space are Phibro Animal Health PAHC, GE HealthCare Technologies GEHC and Cardinal Health CAH.

Phibro Animal Health, currently sporting a Zacks Rank #1 (Strong Buy), reported second-quarter fiscal 2026 adjusted earnings per share (EPS) of 87 cents, which surpassed the Zacks Consensus Estimate by 27.1%. Revenues of $373.9 million beat the Zacks Consensus Estimate by 4.7%. You can see the complete list of today’s Zacks #1 Rank stocks here.

PAHC has an estimated long-term earnings growth rate of 21.5% compared with the industry’s 12% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 20.1%.

GE HealthCare Technologies, currently carrying a Zacks Rank #2 (Buy), reported fourth-quarter 2025 adjusted EPS of $1.44, which surpassed the Zacks Consensus Estimate by 0.7%. Revenues of $5.7 billion beat the Zacks Consensus Estimate by 1.9%.

GEHC has an estimated long-term earnings growth rate of 9.1% compared with the industry’s 12% rise. The company beat earnings estimates in the trailing four quarters, the average surprise being 7.5%.

Cardinal Health, currently carrying a Zacks Rank #2, reported a second-quarter fiscal 2026 adjusted EPS of $2.63, which surpassed the Zacks Consensus Estimate by 10%. Revenues of $65.6 billion beat the Zacks Consensus Estimate by 0.9%.

CAH has an estimated long-term earnings growth rate of 15% compared with the industry’s 9.3% rise. The company’s earnings beat estimates in the trailing four quarters, the average surprise being 9.3%.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Becton, Dickinson and Company (BDX): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

GE HealthCare Technologies Inc. (GEHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).