Sandisk SNDK and Marvell Technology MRVL are major players in the AI infrastructure space. These semiconductor companies are playing an important role in deploying modern computing and benefit from the explosion of data and AI workloads. While Sandisk stores the data through its SSDs and flash memory, Marvell moves and processes this data through custom chips and networking silicon offerings, both targeting hyperscalers, including Amazon Web Services, Microsoft Azure and Google Cloud

However, SNDK or MRVL, which of these AI infrastructure stocks has the greater upside potential right now? Let’s find out.

The Case for SNDK Stock

Sandisk is benefiting from strong demand for NAND storage products, which has transitioned from a commodity, cyclical market to a strategic, AI-driven infrastructure layer. Data centers, including hyperscalers, are replacing consumer devices as the largest buyers of NAND, with demand expected to grow more than 60% within a year. This structural change bodes well for SNDK as long-term contracts and higher pricing stability improve top-line growth as well as margin expansion visibility for investors.

SNDK is riding on an accelerating enterprise SSD demand based on the aforesaid factors. The company is seeing strong adoption across all types of AI infrastructure builders, including cloud hyperscalers, edge and enterprise data centers, OEMs and system integrators who are deploying AI at scale. Increasing demand for high-bandwidth flash for AI inference offers a strong growth opportunity over the long term.

The growing need for fast, high-density storage infrastructure places enterprise SSDs at the center of AI infrastructure buildouts. Sandisk’s expanding presence in this segment is supported by next-generation PCIe Gen5 drives and the forthcoming BiCS8 QLC Stargate solution. This is driving a clear shift in SNDK’s revenue mix toward higher-value data center deployments, signaling a structural pivot beyond traditional end markets.

For the third quarter of fiscal 2026, Sandisk expects non-GAAP revenues between $4.40 billion and $4.80 billion. The company anticipates the market to be more undersupplied than it was in the second quarter and expects bits to be down mid-single digits. Gross margin is anticipated in the 65% to 67% range (up from 51.9% reported in the second quarter of fiscal 2026) while earnings are expected between $12.00 and $14.00 per share.

The Case for MRVL Stock

Marvell is seeing robust strength for its products as the global AI infrastructure spending rises. MRVL’s data center business is riding on strong demand from hyperscalers, AI data centers, AI fabs and high-performance computing clients. Increased investments by these enterprises are pushing the demand for MRVL’s networking, optical interconnect and custom silicon solutions. Marvell is also capitalizing on the rising demand for high-speed connectivity, such as 800G and 1.6T optical interconnects. These solutions are gaining traction as AI workloads require faster communication between GPUs and data centers. Based on the current growth trend, MRVL predicts that its interconnect business will grow more than 50% in fiscal 2027.

MRVL’s custom silicon segment reached $1.5 billion in fiscal 2026 and is expected to further increase on the back of the rising demand from hyperscalers. New opportunities, such as XPU attach, CXL memory expansion and scale-up networking, are opening additional revenue streams. These are further amplified by the latest capabilities in AI networking and PCIe/CXL switching from the acquisitions of Celestial AI and XConn Technologies.

Marvell expects first-quarter fiscal 2027 revenues to be $2.40 billion (+/- 5%). The non-GAAP gross margin is projected to be in the 58.25-59.25% range, while non-GAAP operating expenses are estimated to be approximately $575 million. The company projects non-GAAP earnings for the fiscal first quarter to be 79 cents (+/- 5 cents) per share.

However, macroeconomic and geopolitical uncertainties have been an overhang on Marvell’s near-term performance. Global trade tensions, evolving U.S. chip export restrictions and tariffs create operational and demand-side risks, particularly given Marvell’s reliance on hyperscalers and global supply chains.

Price Performance and Valuation of SNDK and MRVL

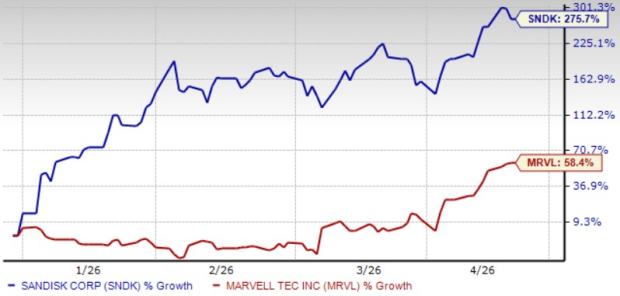

Year to date (YTD), Sandisk shares have jumped 275.7%, outperforming Marvell shares, which have returned 58.4%.

Stock Price Performance: SNDK vs. MRVL

Image Source: Zacks Investment Research

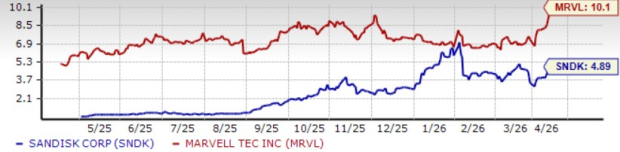

Valuation-wise, both Sandisk and Marvell shares are currently overvalued, as suggested by a Value Score of F and D, respectively.

Valuation: SNDK vs. MRVL

Image Source: Zacks Investment Research

In terms of forward 12-month Price/Sales, Sandisk shares are trading at 4.89X, lower than Marvell’s 10.10X.

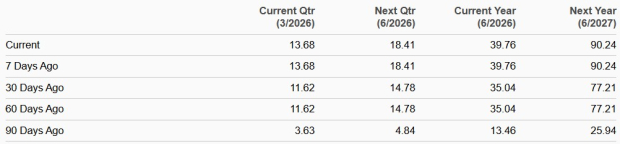

How Do Earnings Estimates Compare for SNDK & MRVL?

The Zacks Consensus Estimate for Sandisk’s fiscal 2026 earnings is pegged at $39.76 per share, up 13.5% over the past 60 days. The company reported earnings of $2.99 per share in fiscal 2025.

Consensus Estimate Trend

Image Source: Zacks Investment Research

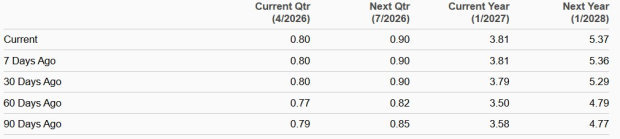

The consensus mark for Marvell’s fiscal 2027 earnings is pegged at $3.81 per share, which has increased 9% over the past 60 days. The figure indicates 34.15% increase year over year.

Consensus Estimate Trend

Image Source: Zacks Investment Research

Sandisk is a Stronger Pick Than MRVL Right Now

Both Sandisk and Marvell benefit from strong AI and data center storage demand. However, Sandisk appears to be the stronger bet given momentum in NAND and enterprise SSD demand.

Sandisk currently sports a Zacks Rank #1 (Strong Buy), which makes it a strong pick compared with Marvel, which has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sandisk Corporation (SNDK): Free Stock Analysis Report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).