Bloom Energy (BE) set a new all-time high on Tuesday, climbing to almost $230, its highest level in five years. The jump followed news that the company expanded its deal with Oracle (ORCL), and it has only increased expectations around its role in powering AI data centers. That kind of move naturally makes people stop and ask what comes next.

Those same AI data centers are popping up everywhere, but not everyone is happy about it. Lawmakers in Maine recently approved a one-year freeze on new large projects because of concerns about power use and the strain on local communities.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

This clash between growing digital demand and limits on the traditional grid is exactly where Bloom Energy comes in, offering on-site fuel cell power as a different way to keep these facilities running. With the stock now at record levels in the middle of all this, is it a buy, a sell, or a hold at today’s price?

What the Numbers Say at New Highs

Based in San Jose, California, Bloom Energy develops and sells solid‑oxide fuel cell systems that provide on‑site, always‑on power for commercial and industrial customers around the world.

The share price is up 140.2% year-to-date (YTD) and 1,070% over the past 52 weeks.

www.barchart.com

www.barchart.comThis move now reflects an equity value of $60 billion, with a trailing 12-month price-to-sales ratio of 25.40 times versus a sector median of 1.94 times and a price-to-cash flow ratio of 526.48 versus 14.69 times, showing the market is clearly paying up for the story.

Their latest quarterly report, for the period ending Dec. 25, showed earnings per share of $0.28 compared with a $0.15 estimate, an 86.67% surprise to the upside. It also showed Q4 2025 revenue of $777.7 million, up 35.9% from $572.4 million a year earlier.

Bloom’s product and service revenue rose to $700.2 million, up from $525.5 million, as the company shipped and installed more of its systems for customers. That same quarter generated operating income of $87.5 million, down $17.2 million from the prior year, along with $418.1 million in cash flow from operating activities.

The full-year numbers help round out the picture. Revenue for 2025 came in at $2.02 billion, up 37.3% from $1.47 billion in 2024, and product and service revenue reached $1.76 billion, 35.5% above $1.30 billion. That growth was backed by $114 million in operating cash flow for the year and a second straight year of positive free cash flow, which gives the stock a firmer foundation.

Bloom’s Building Blocks

Bloom Energy’s growth story right now really starts with Oracle. The two companies recently signed a new master services agreement that lets Oracle buy up to 2.8 GW of Bloom’s solid oxide fuel cell systems to power its growing AI and cloud operations. An initial 1.2 GW is already under contract and being rolled out across projects in the U.S., including those scheduled into next year, which effectively makes Bloom a key on-site power partner for Oracle’s more demanding workloads.

That momentum is being backed up on the utility side, too. A separate $2.65 billion deal with American Electric Power (AEP) covers the long-term supply of Bloom’s fuel cell products for a planned 900 MW facility near Cheyenne, Wyoming. The plant’s entire output is tied to a 20-year offtake agreement with a high-grade customer.

Also, some important work is occurring within the company to manage this expansion in size. In March, Bloom named Simon Edwards as Chief Financial Officer, effective Apr. 13. He brings nearly 20 years of experience in technology and digital infrastructure businesses, including senior roles at cloud software firms and GE Digital, with a focus on tighter operations, stronger systems, and better margins.

What Wall Street Is Seeing at These Highs

The next earnings update is coming up soon. It is scheduled for Apr. 29 and will cover the March 2026 quarter, with the street looking for earnings of -$0.02 per share. That would be a big step up from -$0.11 in the same quarter last year, an estimated improvement of about +81.82%, even though the company is still expected to post a small loss.

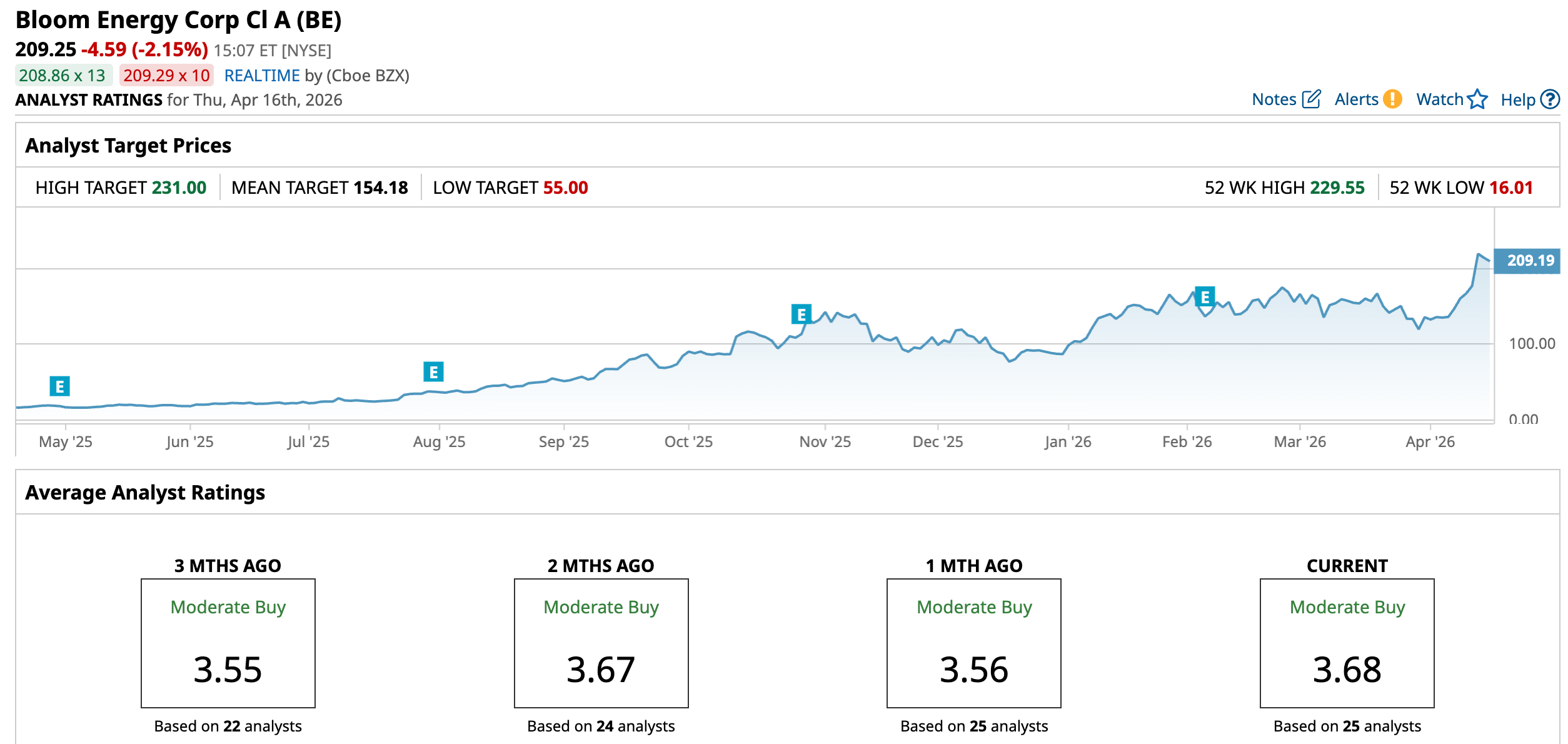

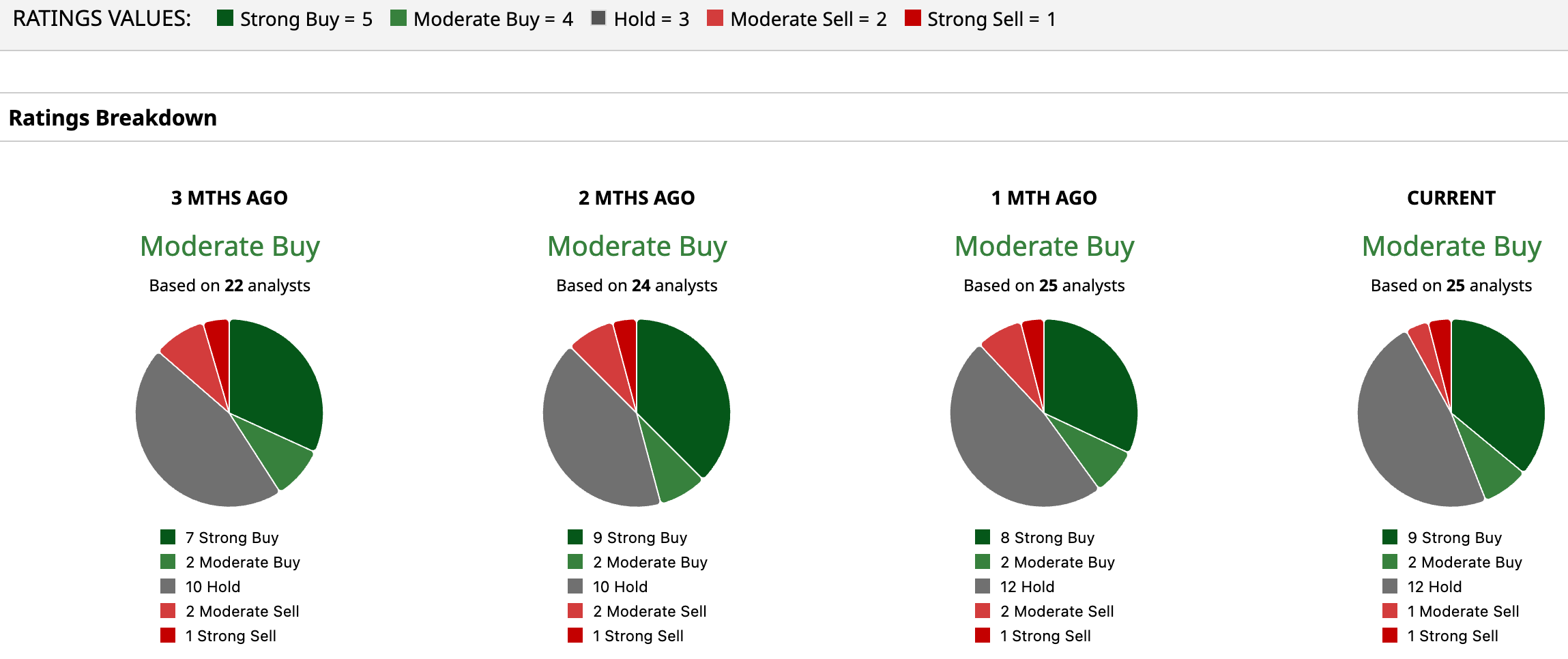

Citi’s latest take lines up with that mixed picture. The firm started coverage on Bloom with a “Neutral” rating and highlighted “strong uptake” for its solutions as power needs rise, but it stopped short of calling the stock a clear “Buy” at current levels.

That view lines up with the broader group of 25 covering firms, where the consensus rating sits at “Moderate Buy.” BE’s price targets tell a more cautious story, though. The average 12-month target is $154.18, which is below the current price and works out to roughly -26% downside from here.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

Bloom Energy looks more like a “Hold” than a fresh “Buy” at this point unless you are genuinely thinking long term and can handle big swings in price. The business has strong momentum, and the Oracle and AEP deals give it a clear growth path, but the stock already trades as if that success is largely in the bag. From here, pullbacks to more reasonable valuation levels are likely to offer better entry points, while selling now mainly makes sense if the position has become too big for your comfort

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Is Bloom Energy Stock a Buy, Sell, or Hold at New All-Time Highs? Does the QQQ ETF Have a Bad Case of Premature Accumulation? Is the Software Apocalypse Real? Piper Sandler Just Slashed Its Price Target on Salesforce Stock. As Airline Stocks Sell Off on Jet Fuel Prices, Delta Is the Top-Rated Stock to Buy on the Dip