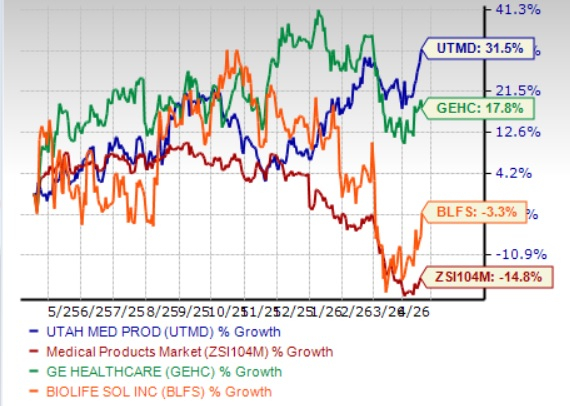

Utah Medical Products, Inc. UTMD shares have gained 31.5% in the past year against the industry’s 14.8% decline. The company has outperformed other industry players, including GE HealthCare Technologies Inc. GEHC and BioLife Solutions, Inc. BLFS. Shares of GE HealthCare have rallied 17.8%, while BioLife Solutions has declined 3.3% in the same time frame. Strong niche positioning, global diversification, clinician-driven innovation, robust balance sheet, and favorable maternal and neonatal healthcare demand trends support steady long-term growth for UTMD.

Image Source: Zacks Investment Research

A Key Look Into UTMD’s Business Operations

Utah Medical develops and manufactures cost-effective, high-quality medical devices focused on improving patient safety and clinical outcomes. Its success relies on identifying clinical needs, designing efficient solutions, ensuring reliable production and distributing products either directly or through partners. UTMD integrates multiple engineering disciplines to create differentiated devices used primarily in neonatal intensive care, labor & delivery and women’s health. The company markets globally through direct sales in key countries and a wide network of distributors, while also producing components for other firms. Founded in 1978, UTMD has expanded through acquisitions and international subsidiaries, strengthening its product range and distribution. Its offerings include fetal monitoring systems, neonatal care devices, surgical tools and pressure monitoring equipment, all designed to enhance efficiency, reduce complications and lower overall healthcare costs.

Utah Medical’s Key Tailwinds

One of the key growth drivers for UTMD is its strong positioning in niche, high-value medical device segments, particularly in neonatal care, labor & delivery and women’s health. The company focuses on clinically differentiated products that improve patient safety and outcomes rather than competing purely on price. This creates a durable competitive advantage, as many of its devices are trusted by clinicians and have been in use for decades.

Another important factor supporting growth is UTMD’s diversified global footprint and direct distribution strategy. The company sells products in over a hundred countries, with direct presence in key developed markets like the United States, the UK, Ireland, Canada, Australia and France, alongside a wide distributor network. This geographic diversification reduces reliance on any single market and allows the company to capture opportunities in international healthcare systems.

Product innovation and continuous development also play a major role in sustaining momentum. UTMD benefits from a steady pipeline of clinician-driven ideas, combined with its in-house engineering and manufacturing capabilities. The company consistently enhances existing products and introduces new devices aimed at improving safety, efficiency and cost-effectiveness in healthcare procedures.

A further supportive element is UTMD’s strong financial position and disciplined capital allocation. The company operates with no bank debt, maintains high cash reserves and generates consistent cash flows, enabling it to fund R&D, withstand cyclical pressures, and return capital to shareholders through dividends and buybacks. This financial strength also allows UTMD to invest opportunistically in acquisitions or capacity expansion without diluting shareholders.

Finally, favorable long-term healthcare trends underpin the company’s outlook. Rising global demand for quality maternal and neonatal care, increasing use of medical devices in both hospitals and outpatient settings and a growing emphasis on patient safety all align closely with UTMD’s product portfolio. As healthcare systems increasingly prioritize better clinical outcomes and cost efficiency, the company’s specialized, safety-focused devices are well-positioned to benefit.

Challenges Persist for UTMD’s Business

The company faces several structural and operational headwinds that could pressure future performance, including increasing regulatory burdens that raise costs, delay product approvals and divert management focus from innovation to compliance. Growing healthcare bureaucracy and the influence of group purchasing organizations limit access to clinicians and shift purchasing decisions toward price rather than clinical value, weakening the firm’s differentiation. Competitive pressure from lower-cost international manufacturers further constrains margins, while reliance on third-party distributors introduces revenue unpredictability. Foreign exchange volatility and tariffs add additional earnings uncertainty, especially given significant international exposure.

Utah Medical’s Valuation

From a valuation perspective, Utah Medical appears relatively expensive. Currently, UTMD is trading at 3.46X trailing 12-month EV/sales value, above the industry’s average of 3.1X. The metric remains higher than one of the company’s peers, GE HealthCare (1.87X), but remains lower than that of BioLife Solutions (9.71X).

Image Source: Zacks Investment Research

Conclusion

Utah Medical offers a stable, niche-driven growth profile supported by strong clinical positioning, global diversification, and solid financial discipline, all of which align with favorable long-term healthcare trends. However, regulatory pressures, pricing constraints, competitive intensity, and international exposure risks may limit upside.

Also, its valuation is higher than the industry average. For long-term investors, UTMD’s strong fundamentals may justify holding the stock, but investors looking to add the stock to their portfolios may want to wait for a better entry point.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BioLife Solutions, Inc. (BLFS): Free Stock Analysis Report

Utah Medical Products, Inc. (UTMD): Free Stock Analysis Report

GE HealthCare Technologies Inc. (GEHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).