Capital One COF is set to announce first-quarter 2026 results on April 21, after market close. Similar to 2025, the company’s to-be-reported quarter’s performance is expected to have been driven by its solid credit card business and the positive effect from the acquisition of Discover Financial (completed in May 2025).

The Zacks Consensus Estimate for COF’s first-quarter revenues is pegged at $15.38 billion, which indicates year-over-year growth of 53.8%.

In the past 30 days, the consensus estimate for earnings for the to-be-reported quarter has been revised 2.5% lower to $4.63. The estimate indicates a 14% rise from the prior-year quarter’s actual.

Estimate Revision Trend

Image Source: Zacks Investment Research

COF has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in three of the trailing four quarters, with the average beat being 22.34%.

Earnings Surprise History

Image Source: Zacks Investment Research

Key Factors at Play for Capital One’s Q1 Results

Net Interest Income (NII): The Federal Reserve kept interest rates unchanged in the first quarter. This followed a 175-basis-point cut in the last two years. While relatively lower rates are likely to have hurt COF’s NII to some extent, declining/stabilizing funding costs would have offered some support.

The overall lending scenario was impressive in the first quarter. Per the Federal Reserve’s latest data, the demand for consumer loans was robust. The Zacks Consensus Estimate for total average earning assets is pegged at $602.1 billion, implying a 30.1% rise from the prior-year quarter.

This, along with stable rates, is expected to have helped Capital One’s NII growth. Also, the company’s continued efforts to strengthen its card operations are expected to have provided support. The consensus estimate for NII of $12.33 billion indicates 54% year-over-year growth.

Fee income: Supported by an overall rise in credit card usage and the Discover Financial buyout, Capital One’s interchange fees (constituting more than 60% of fee income) are likely to have increased in the quarter under review. The Zacks Consensus Estimate for interchange fees is $1.87 billion, suggesting a 52.8% year-over-year jump.

The consensus estimate for service charges and other customer-related fees of $825.9 million implies 62.3% growth from the prior-year quarter. The Zacks Consensus Estimate for other non-interest income is pegged at $313 million, indicating a 40.2% rise.

Thus, the consensus estimate for total non-interest income of $3.02 billion indicates a jump of 51.8% from the prior-year quarter.

Expenses: Capital One has been witnessing a persistent rise in expenses over the past several quarters due to higher marketing costs and investment in technology upgrades. Further, the Discover Financial acquisition, along with inflation pressure, is expected to have resulted in an increase in operating expenses in the fourth quarter.

Asset Quality: Capital One is less likely to have set aside a huge amount of money for potential delinquent loans, as the interest rates have come down substantially from the highs of 5-5.25%. However, given the current macro backdrop, because of the Middle East conflict and the oil price shocks, borrowers are likely to have faced some problems in keeping up with loan repayments. Hence, credit costs for COF are likely to have risen in the to-be-reported quarter.

What Our Quantitative Model Unveils for COF

According to our quantitative model, the chances of Capital One beating the Zacks Consensus Estimate for earnings this time are high. This is because it has the right combination of the two key ingredients — a positive Earnings ESP and a Zacks Rank #3 (Hold) or better.

You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Earnings ESP: The Earnings ESP for Capital One is +2.00%.

Zacks Rank: The company currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

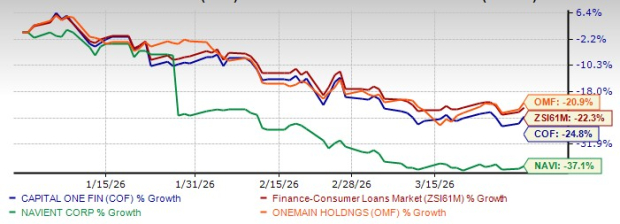

Capital One’s Price Performance

In the first quarter, the COF stock lost 24.8%, underperforming the Zacks Consumer Loans industry. Its peers, Navient Corporation NAVI and OneMain Holdings, Inc. OMF, declined 37.1% and 20.9%, respectively.

1Q26 Price Performance

Image Source: Zacks Investment Research

Navient is scheduled to announce first-quarter 2026 numbers on April 29, while OneMain Holdings is set to announce results on May 1.

Over the past month, the Zacks Consensus Estimate for Navient’s first-quarter 2026 earnings has been revised lower to 17 cents. The consensus estimate for OneMain Holdings has been revised lower to $1.92 over the past 30 days. At present, both NAVI and OMF carry a Zacks Rank #3.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Capital One Financial Corporation (COF): Free Stock Analysis Report

Navient Corporation (NAVI): Free Stock Analysis Report

OneMain Holdings, Inc. (OMF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).