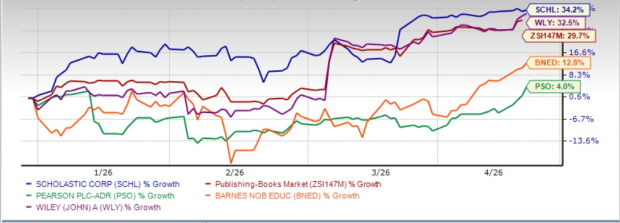

Scholastic Corporation SCHL stock’s strong rally this year has caught investor attention. Scholastic, which operates in the broader educational publishing and media space alongside companies such as Pearson plc PSO, Barnes & Noble Education, Inc. BNED and John Wiley & Sons, Inc. WLY, has seen its shares rise 34.2% year to date, comfortably outpacing the industry’s gain of 29.7%.

The rally has been supported by momentum in its Book Fairs business, a resilient publishing portfolio, improving trends in Education, and expanding reach across digital media and entertainment. The key question now is whether investors should lock in gains or remain invested.

Compared with Scholastic’s strong performance, shares of Pearson, Barnes & Noble Education, and John Wiley & Sons have gained 4%, 12.8%, and 32.5%, respectively.

SCHL Year-to-Date Stock Performance

Image Source: Zacks Investment Research

Decoding Potential Tailwinds Behind SCHL’s Rally

Scholastic stands out as a unique and resilient business built on a powerful combination of a trusted brand, proprietary distribution channels, and globally recognized content. At its core, the company has a deep connection with schools, teachers, and families, giving it a direct and recurring relationship with its end customers that few competitors can match. This direct access creates a strong competitive moat, especially through its school-based channels, which allow Scholastic to consistently reach young readers in a highly targeted and effective way. Over time, this ecosystem has proven to be durable, helping the company maintain relevance across generations while supporting stable demand for its products.

One of the strongest reasons to invest in Scholastic is the continued strength and evolution of its Book Fairs business. This channel is not only highly differentiated but also increasingly productive, benefiting from better execution, improved merchandising, and higher engagement from schools and families. Importantly, the company is not standing still, as it continues to innovate within this platform by introducing new formats and expanding into adjacent educational categories. These initiatives are helping to enhance the overall experience, increase participation, and drive higher spending per event. As a result, Book Fairs represents a reliable and growing engine that can support long-term revenue growth and profitability.

Scholastic’s publishing business further strengthens its investment appeal through a portfolio of iconic and enduring franchises. Titles and series that resonate globally continue to drive strong demand, supported by a combination of new releases, backlist performance and upcoming media tie-ins. This creates a recurring revenue stream that is less dependent on any single product cycle. The company’s ability to consistently produce and extend successful intellectual property across formats is a key advantage, ensuring that its content remains relevant while providing multiple opportunities for monetization. This depth of content not only stabilizes performance but also positions Scholastic to benefit from future entertainment and licensing opportunities.

Another important driver of future growth is the company’s expanding presence in digital media and entertainment. Scholastic is successfully building audiences across platforms such as streaming services and online video, allowing it to reach children in new ways beyond traditional books. This growing digital footprint strengthens the connection between its content and its audience, often driving renewed interest in its core publishing business. During the third quarter of fiscal 2026, the company reported strong viewership growth across its YouTube channels and Scholastic’s TV app. The entertainment division is showing signs of recovery, with improving activity levels and a stronger pipeline of projects. As this segment gains momentum, it has the potential to become a more meaningful contributor to both revenues and profitability over time.

Consensus Estimates for Scholastic See a Positive Shift

The Zacks Consensus Estimate for earnings per share has seen upward revisions. Over the past 30 days, the consensus estimate has risen by 40 cents to $1.88 for the current fiscal and by 65 cents to $2.80 for the next fiscal. These estimates indicate year-over-year growth rates of 291.7% and 48.9%, respectively.

Image Source: Zacks Investment Research

Does Scholastic Tick the Boxes for Value Investing?

From a valuation standpoint, Scholastic's forward 12-month price-to-sales ratio stands at 0.51, below the industry average of 0.77. Scholastic is trading at a discount to Pearson (with a forward 12-month P/S ratio of 1.82) and John Wiley & Sons (1.21).

Image Source: Zacks Investment Research

How to Play Scholastic Stock: Buy, Hold or Sell?

Scholastic appears well-positioned for continued long-term value creation, supported by the strength of its Book Fairs business, the durability of its publishing franchises, improving trends in Education, and a growing digital and entertainment presence. The company’s trusted brand, unique school-based reach, and disciplined capital allocation further strengthen the investment case and suggest that the recent rally reflects real business progress rather than short-term market enthusiasm alone. For current investors, the story still supports staying invested as the company continues to build on these fundamentals, while potential investors may view Scholastic as an attractive name for fresh investment, given its balanced mix of resilience, growth opportunities, and improving execution.

Scholastic currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pearson, PLC (PSO): Free Stock Analysis Report

Scholastic Corporation (SCHL): Free Stock Analysis Report

Barnes & Noble Education, Inc (BNED): Free Stock Analysis Report

John Wiley & Sons, Inc. (WLY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).