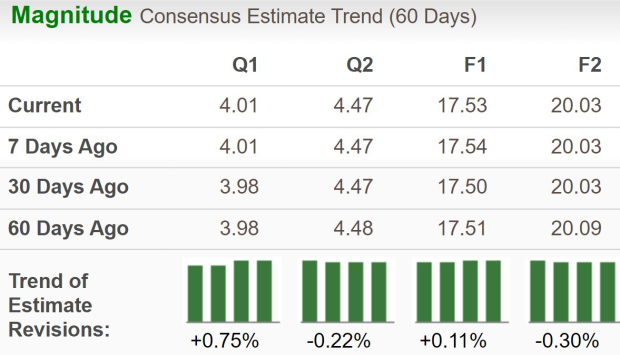

American Express Company AXP is set to report first-quarter 2026 results on April 23, 2026, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $4.01 per share, and the same for revenues is pinned at $18.62 billion.

The first-quarter earnings estimate witnessed one upward revision over the past 60 days against one downward movement. The bottom-line prediction indicates a year-over-year increase of 10.2%. The consensus estimate for quarterly revenues implies year-over-year growth of 9.7%.

For the full-year 2026, the Zacks Consensus Estimate for AmEx’s revenues is pegged at $78.81 billion, implying a rise of 9.1% year over year. Meanwhile, the consensus mark for the full year EPS is pegged at $17.53, implying growth of 14% on a year-over-year basis.

AmExbeat the consensus estimate in three of the last four quarters and missed once, with the average surprise being 3.9%.

American Express Company Price and EPS Surprise

American Express Company price-eps-surprise | American Express Company Quote

Q1 Earnings Whispers for AmEx

Our proven model predicts a likely earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is precisely the case here.

AXP has an Earnings ESP of +4.36% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

What Is Shaping AmEx’s Q1 Results?

AmEx is expected to see a rise in network volumes during the first quarter, likely attributable to the resilient consumer spending of its premium customer base, which is less impacted by economic volatilities. The Zacks Consensus Estimate for first-quarter total network volumes indicates 8.9% year-over-year growth from $439.60 billion.

Discount revenues, a key source of AmEx’s top line, are expected to have benefited from rising network volumes. The consensus mark for first-quarter Discount revenues indicates 7.9% year-over-year growth. Billed businesses in U.S. Consumer Services and Commercial Services are expected to witness growth of 9% and 3.5% year over year, respectively. The Zacks Consensus Estimate for pre-tax income from Commercial Services indicates a 25% jump from a year ago.

Cards-in-force are expected to increase in the quarter on the back of expanding product offerings and stronger market penetration.The consensus projection for first-quarter total cards-in-force indicates 4.8% year-over-year growth. The estimate for Average Card Member loans also implies an 8.8% year-over-year increase.

AmEx’s interest income, another major revenue contributor, is expected to rise on higher loan receivables. The estimate for AXP’s net interest income implies an upside of 9.5% from the year-ago reported figure.

The above factors are expected to support year-over-year growth in the first quarter and set the stage for a potential earnings beat. However, higher customer engagement and operating costs could limit the upside. First-quarter client engagement costs are expected to have increased due to expanding Card Member spending and higher usage of travel and lifestyle-related benefits.

AXP’s Price Performance & Valuation

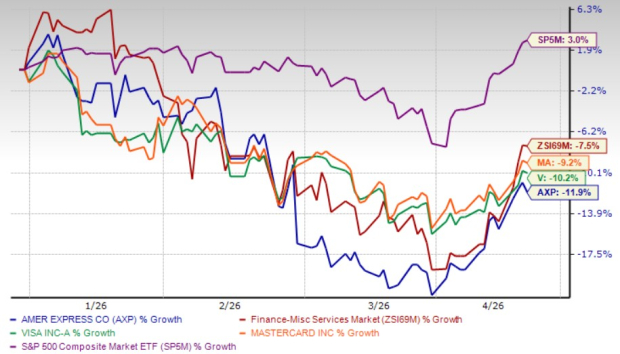

AmEx’sstock has declined 11.9% in the year-to-date period, underperforming the industry’s fall of 7.5%. During this time, Visa Inc. V has lost 10.2% while Mastercard Incorporated MA dropped 9.2%. The S&P 500 Index gained 3% during the same period.

Price Performance – AXP, V, MA, Industry & S&P 500

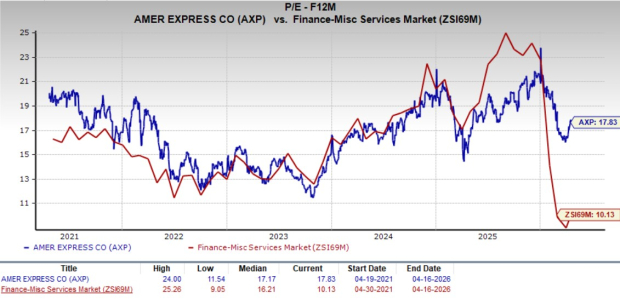

Now, let’s look at the value American Express offers investors at current levels.

Currently, AXP is trading at 17.83X forward 12-month earnings, above the industry’s average of 10.13X, marking it overvalued. However, it is much cheaper compared to its peers like Visa and Mastercard, which are valued at 22.90X and 25.44X F12M P/E, respectively.

How to Play American Express Stock Now?

American Express appears well-positioned for a solid first-quarter performance, supported by resilient spending from its premium customer base, steady growth in network volumes and continued traction in cards-in-force. Strength in discount revenues and interest income, backed by higher loan balances, should keep revenue momentum intact.

The company’s closed-loop model, expanding premium product mix and growing appeal among younger consumers remain key long-term advantages. Its investments in AI-driven personalization and fraud controls could also support engagement and efficiency over time.

That said, rising customer engagement costs and higher operating expenses remain notable pressure points, especially as richer rewards and travel-related benefits continue to weigh on expense intensity. With shares underperforming year to date and valuation still above the industry average, the stock presents a balanced setup heading into earnings. Investors may be better off waiting for the report before making any fresh investment decision.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mastercard Incorporated (MA): Free Stock Analysis Report

Visa Inc. (V): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).