With a market cap of $31.6 billion, Axon Enterprise, Inc. (AXON) is a U.S.-based public safety technology firm that develops conducted energy weapons (TASER devices) alongside a growing suite of digital solutions for law enforcement and security agencies. Headquartered in Scottsdale, Arizona, its hardware segment includes TASER devices and related consumables, which provide a steady revenue stream through ongoing purchases and upgrades.

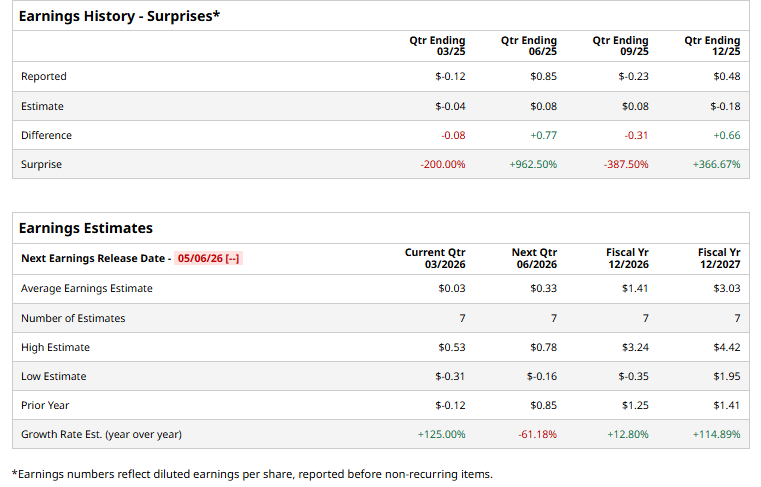

The safety tech juggernaut is expected to report its fiscal 2026 Q1 earnings soon. Ahead of the event, analysts expect AXON to report an earnings of $0.03 per share, up 125% from a loss of $0.12 per share reported in the year-ago quarter. It has exceeded analysts' earnings estimates in two of the past four quarters, while missing in two other quarters.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For the current year, analysts expect AXON to report EPS of $1.41, up 12.8% from $1.25 in fiscal 2025. Moreover, analysts expect its earnings to surge 114.9% year over year to $3.03 per share in fiscal 2027.

www.barchart.com

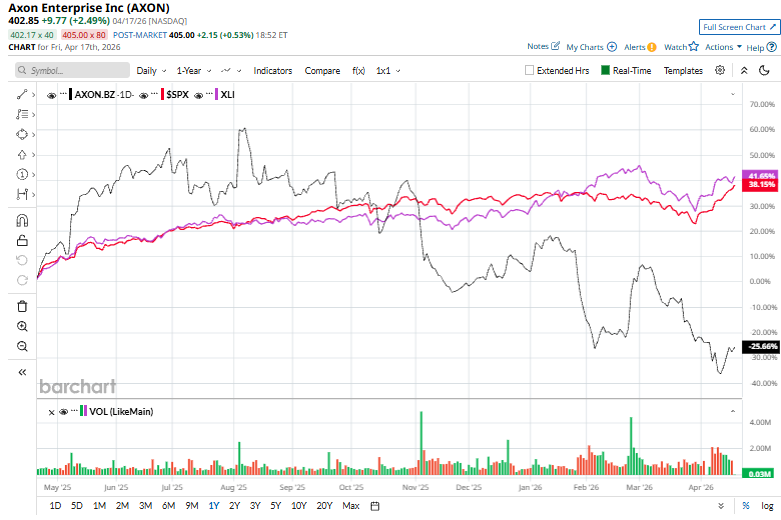

www.barchart.comOver the past year, AXON shares have declined 28%, significantly underperforming the S&P 500 Index’s ($SPX) 34.9% gains and the Industrial Select Sector SPDR Fund’s (XLI) 38.5% rally over the same time frame.

www.barchart.com

www.barchart.comAxon Enterprise shares surged 5.3% on Apr. 15 after TD Cowen reaffirmed its “Buy” rating with a price target of $825, citing expectations of a strong revenue beat and an upward revision to full-year guidance. The optimism was driven by robust adoption of newer offerings, including AI solutions, automated license plate recognition (ALPR), drones, and the Fusus platform, helping reverse recent negative sentiment around the stock.

The consensus opinion on AXON stock is highly optimistic, with an overall “Strong Buy” rating. Out of the 20 analysts covering the stock, 14 recommend a “Strong Buy,” four recommend a “Moderate Buy,” and two recommend a “Hold.” Its mean price target of $723.17 indicates a robust 79.5% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Only 3 Dividend Kings Passed This Brutal Screen. They Could Pay You Well for Years to Come. United Airlines Stock Is Flying Higher as Strait of Hormuz Opening Promises to Lower Jet Fuel Prices. Should You Buy It Here? As Critical Metals Ups Its Stake in Greenland Rare Earths, Should You Buy CRML Stock Today? Why Many (or Most) of Your Stock Picks Have Not Been Successful