Former U.S. Treasury Secretary Henry Paulson is pressing policymakers to put an emergency plan in place in case the demand for U.S. Treasurys suddenly collapses. In such a scenario, the fallout could be fast and devastating, and Paulson wants the government to be prepared.

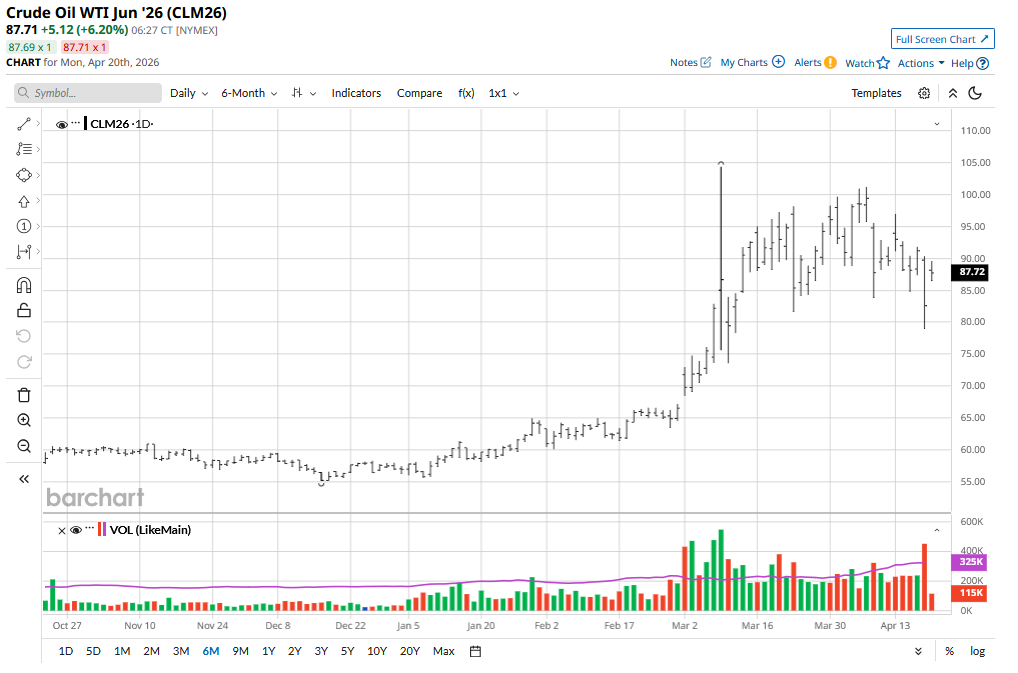

The current geopolitical environment is adding to the uncertainty. The U.S. government is currently involved in a standoff with Iran, which directly impacts oil supply, as evident from surging oil prices over the last two months.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

www.barchart.com

www.barchart.comDifferent and Bigger Than 2008

Paulson was the man in charge when the 2008 financial crisis nearly brought down Wall Street. Back then, the problem was reckless bank lending and toxic mortgage debt. This time, Paulson says the risk is coming from a completely different place — the size of the U.S. government’s own debt and how much it needs to borrow just to keep operating. With roughly $31 trillion in outstanding Treasury debt, the government’s capacity to borrow is at an all-time low.

Paulson’s core fear is a breakdown in the Treasury market that triggers a self-reinforcing cycle of pain. Here is exactly how that could play out:

Investors lose confidence and demand higher yields (interest rates) to keep buying U.S. government bonds, to compensate for growing fiscal risk. Higher rates mean the U.S. government’s borrowing costs climb, which expands the budget deficit even further. A larger deficit forces the government to issue even more debt, flooding the market and further spooking investors. In a worst-case scenario, the Federal Reserve steps in as the buyer of last resort, pushing bond prices lower and driving interest rates higher across the entire economy.The Reality of Risk Versus Timing

Paulson is not predicting a crash next week. But he is clear that nobody knows exactly when stress could hit, and that is precisely the problem. When it does come, it could arrive without warning and escalate rapidly. That is why he is urging policymakers to have a rapid-response plan ready to deploy before the market forces their hand, not after.

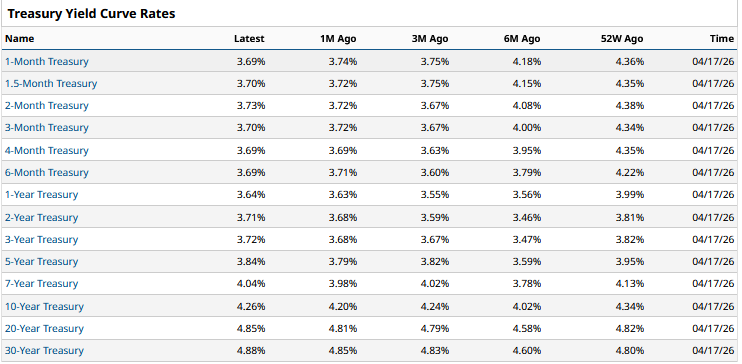

These are the interest rates the U.S. government is paying on its debt across different time periods. Rising yields on longer maturities signal that investors want more compensation for long-term fiscal uncertainty.

www.barchart.com

www.barchart.comThe 30-year yield is significantly higher than the two-year, a steep gap that reflects how uneasy investors are about the long-term fiscal outlook for the United States.

What Are Others Saying About the U.S. Debt?

Earlier this year, Blackrock (BLK) issued a scathing warning on the U.S. debt, pointing out that the increasing risk could put the U.S. dollar's status as a reserve currency in doubt. This would then improve the case for investing opportunities outside of the U.S., thus bringing down the economy in the process. This has become even more apparent now, as China continues to dump U.S. Treasurys at an alarming rate.

At the beginning of April, Federal Reserve Chair Jerome Powell reiterated these risks. While he played down the absolute size of the debt, he pointed out that it is the pace at which debt is being added that is alarming. Like Paulson, he also pointed out that this could end in disaster if something isn’t done soon.

The question for investors is how to prepare for an era where the unquestioned demand for U.S. debt may be fading. Henry Paulson rightly wants policymakers to answer that question before investors and the general public go looking out for answers on their own.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.