Apple (AAPL) shares edged higher, buoyed by fresh data showing a sharp rebound in its most critical international market on April 17. iPhone shipments in China surged 20% year-over-year (YOY) in the first quarter, making Apple the fastest-growing major smartphone vendor in a market that otherwise contracted.

The strength of this performance is underscored by the broader backdrop as China’s overall smartphone shipments declined roughly 4% during the same period, pressured by supply chain disruptions and rising component costs. Yet Apple not only defied the downturn but gained share, reinforcing the durability of its premium positioning and ecosystem-driven demand.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

It remains to be seen whether this surge represents a cyclical rebound or a more structural turnaround in a region that has weighed on Apple’s growth in recent years. China remains the world’s largest smartphone market and a critical battleground against domestic competitors like Huawei, making any sustained momentum there highly important for Apple’s revenue trajectory and valuation.

With the stock reacting modestly to the news, the market appears cautiously optimistic.

About Apple Stock

Based in California, Apple stands as a forward-looking company and a worldwide leader in hardware, software, and services. Its portfolio spans iconic devices like the iPhone, iPad, Mac, and Apple Watch, alongside widely used platforms such as the App Store, iCloud, Apple Music, and Apple TV+. The company currently boasts a market cap of $4 trillion and a Magnificent Seven status.

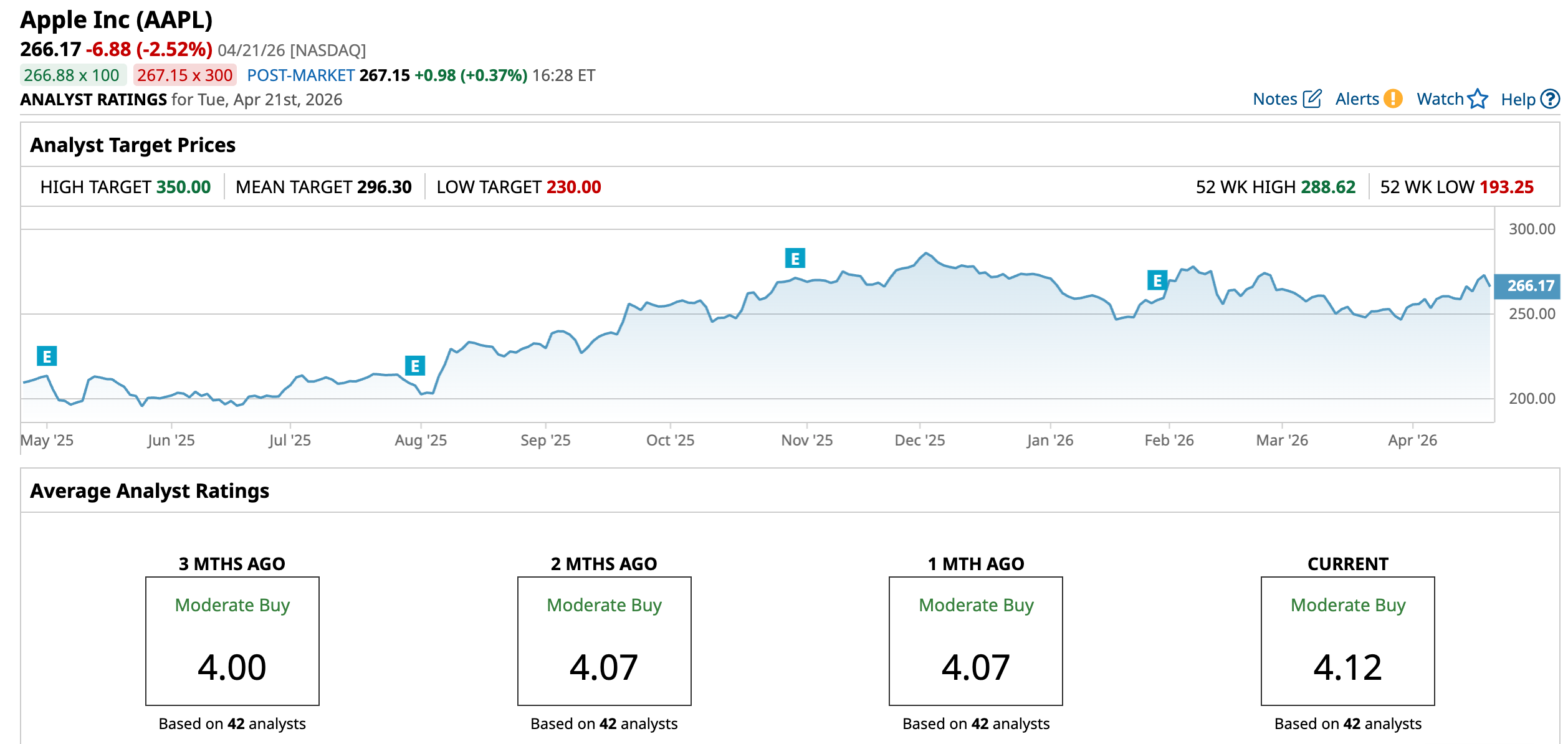

Apple’s stock performance over the past year reflects a pattern of resilience tempered by intermittent bouts of macro-driven volatility. Over the past 52 weeks, the stock’s overall returns stood at 37.8% despite periods of weakness, particularly tied to China demand concerns and broader tech sector rotations that have capped upside.

In 2026, however, the momentum has been far less convincing. Apple stock has seen marginal gains as geopolitical uncertainty, rising component costs, and earlier concerns about slowing iPhone demand weighed on investor sentiment. The stock’s underperformance underscores a market that is increasingly demanding clear evidence of reacceleration.

Against this backdrop, the recent data point showing a 20% YOY surge in iPhone shipments in China has provided a timely catalyst. The stock moved modestly higher, gaining 2.6% intraday on April 17 and 1% on the following session, signaling a tentative improvement in sentiment. This reaction is notable not for its magnitude, but for its direction, as it comes amid a broader contraction in China’s smartphone market, where overall shipments declined, highlighting Apple’s ability to gain share even in a weakening environment.

Notably, Apple announced on Monday, April 20, that CEO Tim Cook will step down from his role on Sept. 1, 2026. Cook will transition to the role of executive chairman of the board. John Ternus, currently Apple’s Senior Vice President of Hardware Engineering, will succeed him as the new CEO. The news led the stock falling slightly in after-hours trading.

www.barchart.com

www.barchart.com The stock trades at a premium at 31.83 times forward earnings, compared to the sector median and its historical average.

Q1 Results Exceeded Expectations

Apple reported its fiscal 2026 first-quarter results for the period ended Dec. 27, 2025, on Jan. 29, 2026, delivering what can only be described as a record-breaking holiday quarter that exceeded expectations.

The company posted revenue of $143.8 billion, representing a 16% YOY increase from $124.3 billion in the prior-year quarter, while earnings per share rose 19% to $2.84, above expectations. Net income came in at $42.1 billion, compared to $36.3 billion in the same period last year.

The growth was primarily driven by the iPhone segment, which delivered its strongest quarter on record, with revenue rising 23.3% YOY to about $85.3 billion. Services continued to provide a structurally important and high-margin growth engine, increasing 14% YOY to $30 billion. On the other hand, product revenue grew 16.1% YOY to $113.7 billion.

Performance across other hardware categories was more mixed. iPad revenue increased modestly by about 6.3% YOY to $8.6 billion, while Mac revenue declined 6.7% YOY. Wearables, home, and accessories also experienced a slight contraction.

Geographically, Apple delivered strong growth across all major regions, with particularly notable momentum in emerging markets and a sharp rebound in Greater China, where revenue increased 37.9%, supported by strong demand for the latest iPhone cycle.

Furthermore, management provided guidance for the fiscal second quarter, forecasting revenue growth in the range of 13% to 16% YOY. The company also guided for gross margins in the 48% to 49% range, while flagging potential cost pressures from rising memory prices.

Analysts covering Apple predict its EPS to rise by 15.8% YOY to $1.91 in the second quarter (about to be reported on April 30). Further, the consensus estimate of $8.49 for fiscal 2026 indicates an increase of 13.8% YOY, before improving by around 9.7% annually to $9.31 in fiscal 2027.

What Do Analysts Expect for Apple Stock?

Recently, Wedbush reiterated its “Outperform” rating and $350 price target on Apple despite the major leadership shake-up, under which Tim Cook will become Executive Chairman and John Ternus will take over as CEO.

Moreover, Monness, Crespi, Hardt & Co. reiterated a “Buy” rating on Apple with a $315 price target. Also, this month, BofA Securities raised its price target on Apple to $325 from $320 while maintaining a “Buy” rating, citing stronger-than-expected iPhone demand and Services growth.

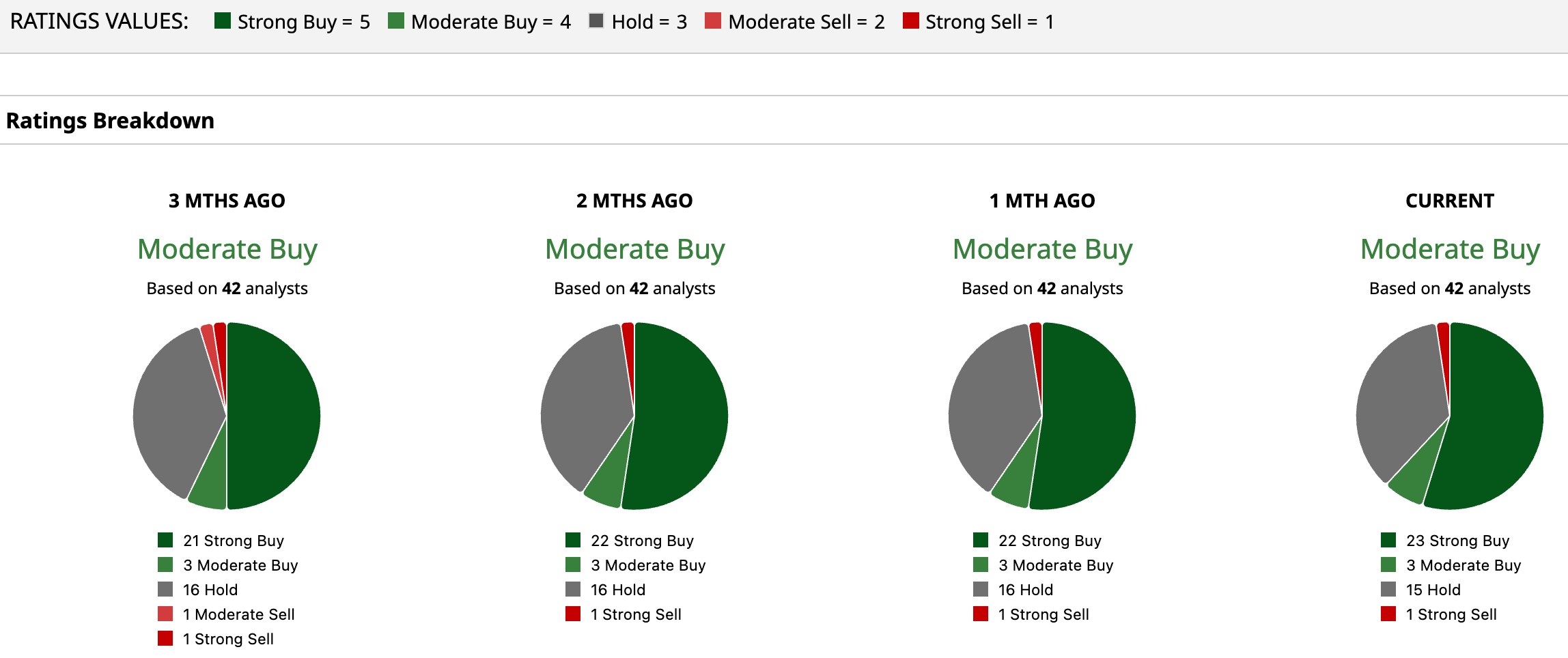

Apple stock has a consensus “Moderate Buy” rating overall. Out of 42 analysts covering the tech giant, 23 recommend a “Strong Buy,” three give a “Moderate Buy,” 15 analysts stay cautious with a “Hold” rating, and one has a “Strong Sell” rating.

While the average analyst price target of $296.30 suggests an upside of 11.32%, Wedbush’s Street-high target price of $350 suggests as much as 31.5% upside ahead.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Astera Labs Stock Jumps on Major Amazon-Anthropic Deal. Should You Buy ALAB Here? As China iPhone Shipments Jump 20%, Should You Buy Apple Stock? Is a Short Squeeze Breaking Out in Beyond Meat Stock Now? Is PayPal an Acquisition Target? How to Play PYPL Stock Right Now Amid Activist Investor Rumors.