In a market obsessed with hypergrowth stocks, defensive stocks are often overlooked as dull. Yet, these so-called “boring” stocks tend to shine when volatility rises. In a diversified portfolio, these defensive dividend stocks serve as safe haven assets, providing stability, consistent returns, and stable income. With an extraordinary 54-year streak of consecutive dividend hikes, Abbott Laboratories (ABT) has earned its place as a Dividend King and could continue to be a winner in your portfolio.

Is ABT stock a buy now?

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

www.barchart.com

www.barchart.com A Reliable Start to the Year Despite Headwinds

Valued at $160.5 billion, Abbott Labs is a global healthcare company that develops and sells medical devices, diagnostic tests, nutritional products, and branded generic medicines across 160 countries. By increasing dividends for 54 years in a row, Abbot Labs has earned the title of both a Dividend Aristocrat and a Dividend King. But Abbott is not just a defensive dividend stock. It has growth potential too, as it actively invests in the future of healthcare.

Last week, the company reported its first-quarter results, with adjusted earnings growth of 6% to $1.15, in line with its guidance and the consensus estimates. This growth comes amid higher financing costs tied to a major acquisition and weaker demand in certain diagnostic categories. Revenue increased 3.7% on a comparable basis to $11.1 billion, reflecting the strength of Abbott’s diversified business model. The company operates through four business segments:

Nutrition: This segment produces science-based nutritional products for all age groups. Diagnostics: This segment focuses on early detection and monitoring of diseases. Established Pharmaceuticals (EPD): This segment sells branded generic medicines across gastroenterology, women’s health, cardiovascular diseases, and pain management, mostly in emerging markets Medical Devices: This segment designs and manufactures devices used to treat serious health conditions.Notably, the EPD segment grew 9% in the quarter, driven by strong demand across Latin America and Asia-Pacific regions. Comparable sales in the medical devices segment rose 8.5%, owing to strong demand in cardiovascular devices, including electrophysiology and heart failure treatments. Abbott’s nutrition business is currently in a transition phase. The company has been adjusting pricing strategies to restore volume growth after a period of softness. Hence, comparable sales declined 7.7% in the quarter.

Abbott's diagnostics segment showed mixed results, with comparable sales up only 1.8%. However, the acquisition of Exact Sciences could mark a significant strategic shift, pushing the company deeper into the rapidly expanding cancer diagnostics market. Management expects this deal to generate approximately $3 billion in incremental sales in 2026.

A Dividend King Built for All Market Conditions

Abbott's diversified business model has reduced reliance on any single product or segment, helping it stay stable even when one segment stumbles. This balanced model is the key reason Abbott Labs has paid 406 consecutive quarterly dividends since 1924. Furthermore, healthcare is one sector that always remains in demand, regardless of the economic climate. Abbott’s 54-year streak of consecutive dividend hikes reflects its disciplined approach to growth and capital allocation. The company offers a dividend yield of 2.6%, higher than the S&P 500 ($SPX) average. Its forward payout ratio of 45% is also sustainable while leaving room for dividend hikes.

With strategic acquisitions, a robust innovation pipeline, and an expanding global presence, Abbott is positioning itself for the next phase of growth while maintaining its reputation as a reliable dividend stock. Analysts predict earnings to grow at a stable rate of 6.5% in 2026, followed by 10.6% in 2027, which will support dividend payouts.

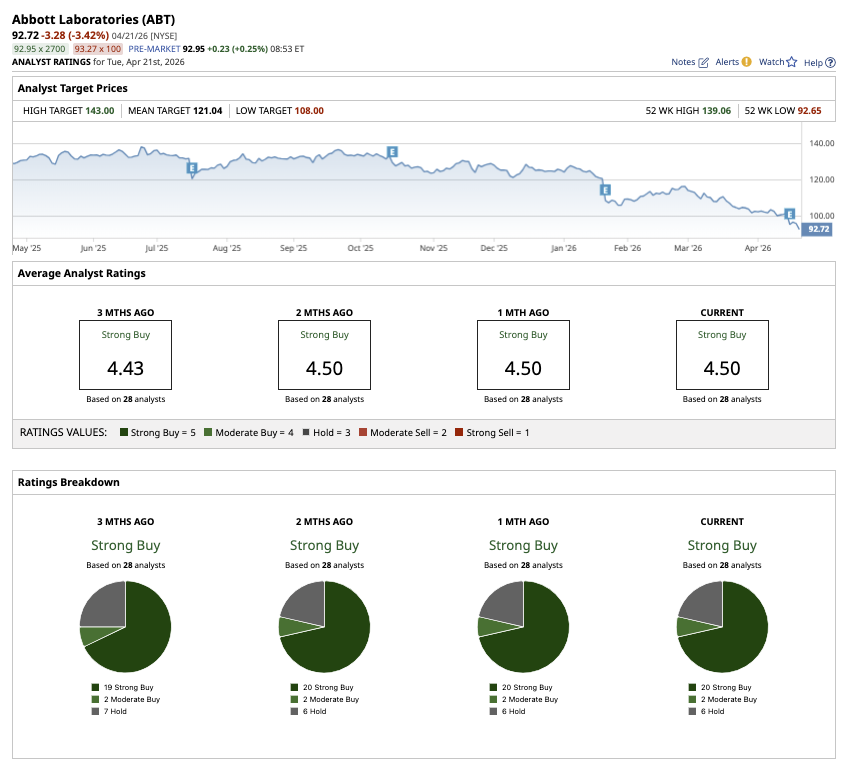

Overall, analysts have rated ABT stock a “Strong Buy.” Out of 28 analysts covering the stock, 20 have a “Strong Buy” rating, two have a “Moderate Buy” rating, and six have a “Hold” rating. ABT stock is down 25.4% year-to-date (YTD), compared to the broader market. But analysts expect the stock to climb 30.5% from current levels based on its average target price of $121.04. Plus, the high price estimate of $143 implies potential upside of 54.2% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Boring Dividend King Might Be the Safest Pick to Add to Your Portfolio Should You Sell Apple Stock Before September 1? Lululemon Is Sinking on New CEO Pick. Should You Buy, Sell, or Hold LULU Stock? Is Arm Stock a Buy at New All-Time Highs?