Alphabet (GOOG) (GOOGL) is set to report its first-quarter earnings on Wednesday, April 29. GOOGL stock has advanced about 19% over the past month, reflecting the market’s optimism about Google’s ability to translate its artificial intelligence (AI) investments into sustained revenue growth.

Notably, Google’s integration of AI across its core businesses is accelerating its growth. Within Search, enhanced AI capabilities are improving user engagement and ad targeting efficiency, which in turn is supporting stronger advertising revenues.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Also, AI is strengthening Google’s Cloud business. As enterprises accelerate adoption of AI-driven tools and infrastructure, Alphabet’s cloud segment is benefiting from increased demand for AI solutions. Another catalyst is Alphabet’s custom-designed Tensor Processing Units (TPUs). Demand for its in-house AI chips is rising, providing the company with a significant growth platform.

Overall, Alphabet is in a solid position heading into the first-quarter earnings release. Its dominance in Search, solid momentum in Cloud, and opportunities in hardware provide multiple avenues for growth.

www.barchart.com

www.barchart.com AI-Led Momentum to Drive Growth in Q1

Alphabet entered 2026 with strong operating momentum, driven by its growing AI capabilities across its core businesses. AI is driving both user engagement and monetization, particularly within its Search and Cloud businesses.

In Search, the rollout of features such as AI Overviews and AI Mode is driving engagement and improved ad yield. These enhancements strengthen the durability of Google’s core advertising engine while positioning it for incremental monetization opportunities.

The company’s solid financial performance reflects this acceleration. Alphabet surpassed $400 billion in annual revenue in 2025, with broad-based strength across segments. Search revenue grew 17% in the fourth quarter, signaling sustained demand. YouTube continues to evolve into a diversified revenue platform, exceeding $60 billion in annual revenue from advertising and subscriptions.

The standout performer, however, was Google Cloud. Revenue jumped 48% in Q4, pushing its annualized run rate beyond $70 billion. The segment’s growth reflects solid enterprise adoption of Google’s AI infrastructure, platforms, and solutions. Moreover, its backlog climbed 55% quarter-over-quarter (QOQ) to $240 billion, indicating solid growth ahead.

Enterprise adoption is accelerating. In 2025, Alphabet signed more billion-dollar contracts than in the previous three years combined. Existing customers are also significantly expanding their usage. This suggests both strong retention and deeper integration of Google’s products.

AI is providing a solid competitive advantage. About 75% of its customers are now using its integrated AI offerings, which combine custom hardware such as TPUs, foundation models, and enterprise platforms. These customers tend to adopt more services overall, creating opportunities for cross-selling and strengthening long-term relationships.

Despite strong top line momentum, Alphabet’s near-term profitability may face headwinds. Elevated capital expenditure, primarily related to AI infrastructure investments, is expected to pressure margins. Analysts expect Alphabet to report earnings of $2.64 per share in Q1, reflecting a year-over-year (YOY) decline of more than 6%.

Notably, Alphabet has consistently exceeded analysts’ EPS consensus expectations over the past four quarters.

Is Alphabet Stock a Buy, Sell, or Hold Now?

Alphabet's first quarter will reflect sustained operational strength. The company continues to benefit from its leadership in Search and strength in YouTube. At the same time, its Cloud division is scaling rapidly, supported by increasing enterprise adoption and demand for AI-driven solutions.

Despite this favorable operating backdrop, near-term earnings may face pressure from elevated capital expenditures. These costs, while weighing on margins in the short run, are likely to strengthen Alphabet’s competitive moat. Moreover, much of this anticipated margin compression appears to be already reflected in the stock’s current valuation, suggesting limited downside from these factors unless execution falters.

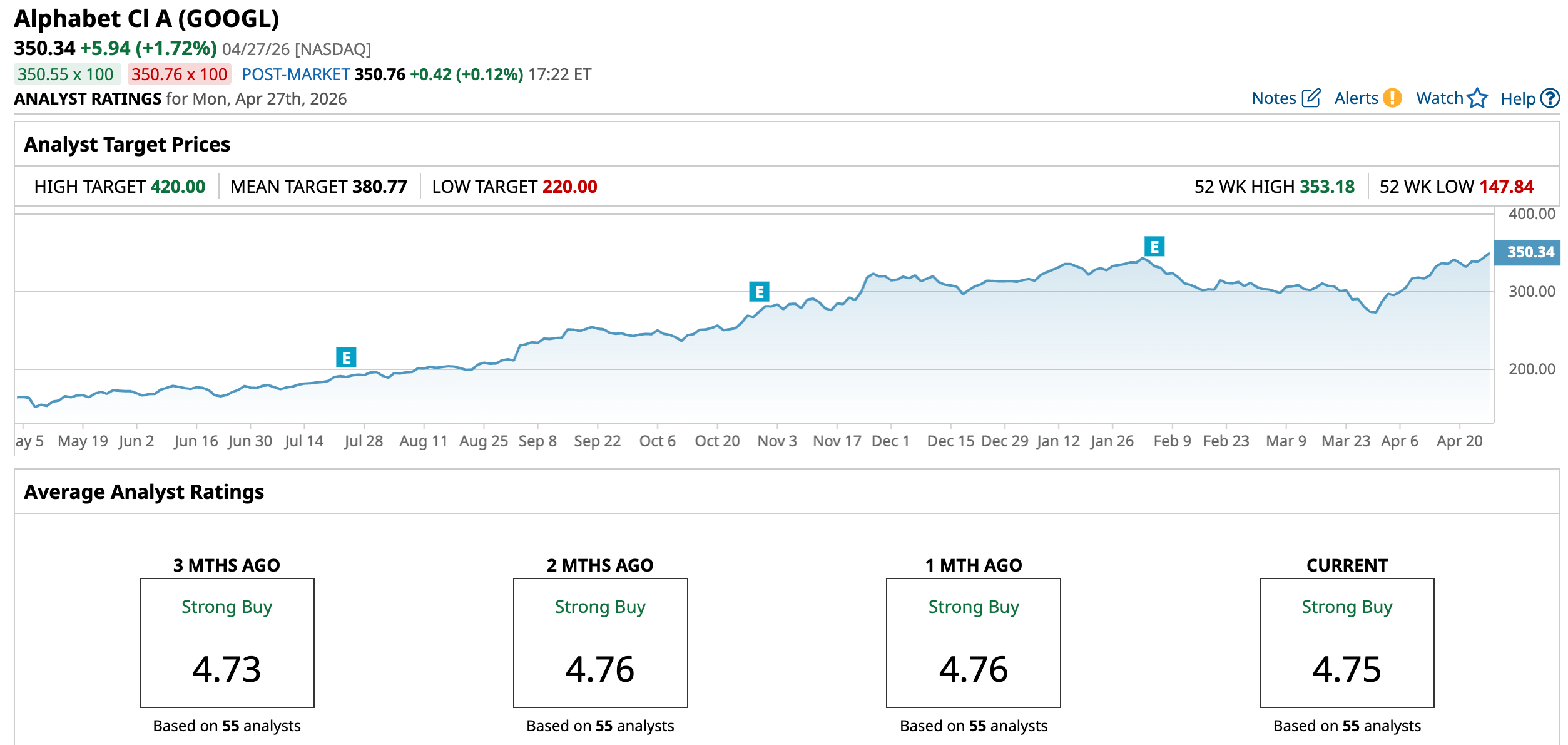

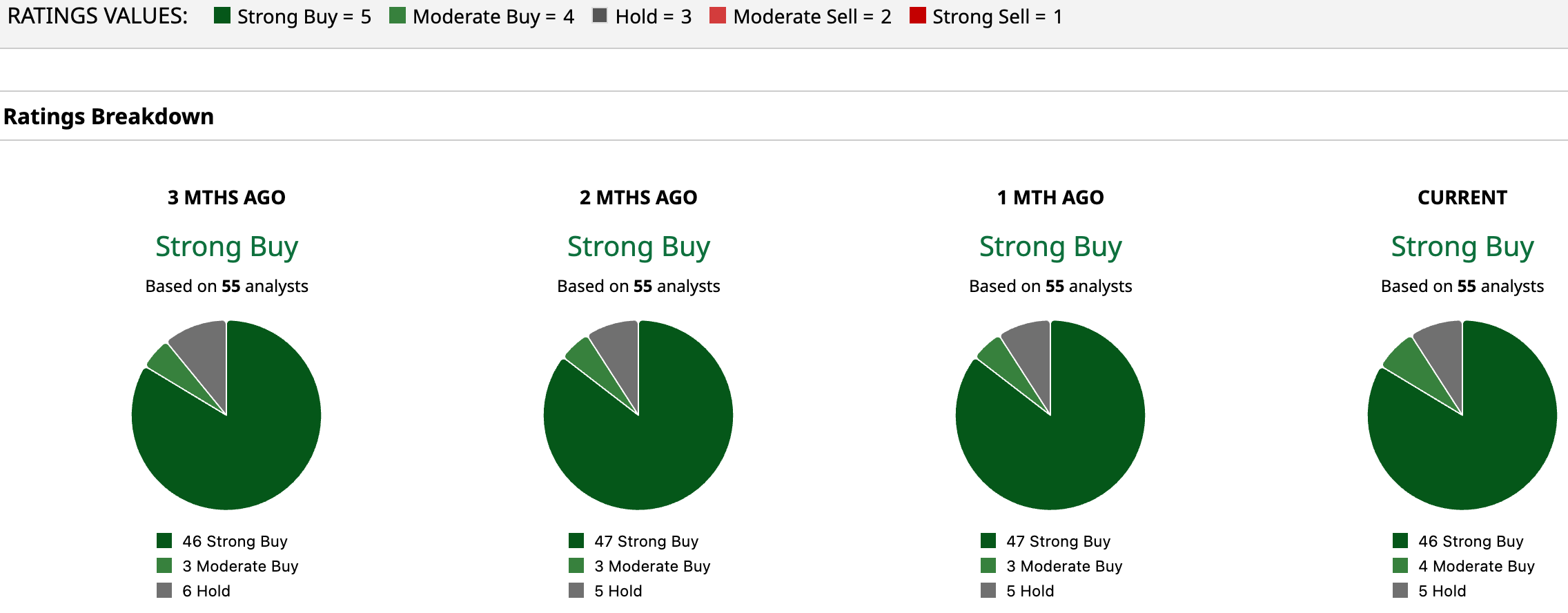

Overall, Alphabet stock is appealing to investors with a long-term outlook. Wall Street analysts maintain a “Strong Buy” stance heading into the earnings release.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Michael Burry Disagrees With the AI Narrative, Buys Microsoft Stock and 2 Unexpected Names Domino's Pizza Stock Drop May Be Overdone, Based on Its Strong FCF Margins A $7.5 Billion Reason to Buy Applied Digital Stock Here Is Alphabet Stock a Buy, Sell, or Hold Ahead of Q1 Earnings?