Investor enthusiasm around Intel Corporation (INTC) has returned with force and not without reason. Following a pivotal Q1 earnings beat, the narrative around artificial intelligence (AI) infrastructure is undergoing a subtle but important shift. For much of the past two years, GPUs dominated the conversation. But as AI systems evolve toward more complex, autonomous “agentic” architectures, the role of the CPU is rapidly being re-rated.

That pivot was reinforced by a landmark agreement between Amazon.com (AMZN) and Meta Platforms (META), in which Meta will deploy tens of millions of AWS-designed Graviton processors to power next-generation AI workloads. Far from being a niche infrastructure decision, the deal signals a broader industry realization that agentic AI systems built around orchestration, reasoning, and real-time tool use are inherently CPU-intensive.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Intel’s latest results align closely with this emerging paradigm. Management highlighted that the transition from model training to inference and agentic workflows is “significantly increasing the need” for CPUs, particularly in data center environments. This is already showing up in the numbers, with strong growth in Intel’s data center and AI segment and a surge in demand for server-grade processors.

Moreover, the Amazon-Meta deal provides external validation that CPUs are moving back toward the center of the architecture. As investors reassess the long-term compute mix required to power agentic AI, Intel’s positioning in high-performance processing may be more strategically valuable than the market previously assumed.

About Intel Corporation Stock

Intel Corporation is a leading technology company specializing in the design, development, manufacture and marketing of semiconductor products, including microprocessors, chipsets, graphics processing units (GPUs), memory and related hardware for consumer, enterprise and industrial markets. Headquartered in Santa Clara, California, Intel remains a key player in data center, PC and emerging AI and networking segments. Intel’s market cap is $424.5 billion, reflecting its valuation among the world’s largest semiconductor companies.

The recent price action in Intel stock reflects one of the most dramatic sentiment reversals. After a period of underperformance, Intel has emerged as one of the market’s strongest AI-linked turnaround stories in 2026.

Year-to-date (YTD), the stock has delivered exceptional gains, rising 121.63%, making it one of the top performers in the S&P 500 Index ($SPX) and materially outperforming both the broader index and peers. This sharp re-rating has been driven by a combination of earnings momentum, improving execution, and critically, a shift in investor perception around CPUs’ role in AI infrastructure.

Over the past 52 weeks, Intel’s performance has been even more striking. The stock has rallied 334.4% from a 52-week low of 18.97, reached in August 2025, closing the last session at $81.80. The stock has gained 298.7% over the past year.

Moreover, on April 24, after Intel delivered a blowout Q1 earnings report, the stock surged 23.6% in a single session, its best daily performance since 1987, hitting a 52-week high of $85.22. The surge signaled that investors are increasingly viewing it as a direct beneficiary of the next phase of AI adoption, particularly inference and agentic workloads, where CPUs play a central role.

www.barchart.com

www.barchart.com The stock is currently trading at a premium to its sector median at 988.16 times forward earnings.

Outstanding Financial Growth

Intel’s first-quarter 2026 earnings were released on April 23. The company reported revenue of $13.6 billion, up 7% year-over-year (YOY), while non-GAAP earnings per share (EPS) reached $0.29 versus $0.13 in the prior-year period, representing a 123% YOY increase and exceeding expectations. On a non-GAAP basis, net income rose to $1.5 billion, up 156% YOY.

The most important feature of the quarter was the acceleration in Intel’s data center and AI business, which is increasingly defined by CPU demand tied to AI workloads. Segment revenue reached $5.1 billion, up 22% YOY, materially outpacing the rest of the portfolio and well ahead of expectations. This growth was driven primarily by server CPUs, particularly Xeon processors, as hyperscalers and enterprises scale infrastructure for inference and emerging agentic AI systems. Management explicitly framed CPUs as the “essential role” in the AI era, reflecting a shift from GPU-centric training workloads toward CPU-heavy orchestration, inference, and real-time processing.

This CPU-led demand is not merely cyclical but structural. Industry data indicates that AI server architectures are evolving toward significantly higher CPU-to-GPU ratios, which is materially increasing unit demand and pricing power for server-grade processors. As a result, Intel is actively prioritizing production capacity toward data center CPUs, underscoring the centrality of this segment to near-term growth.

Outside of the data center, performance was more mixed but still constructive. The Client Computing Group generated $7.7 billion in revenue, up about 1% YOY, while the foundry business experienced around 16% growth.

Furthermore, Intel’s guidance reinforced the improving trajectory. For Q2 2026, the company expects revenue of $13.8 billion to $14.8 billion and non-GAAP EPS of $0.20.

Analysts predict EPS to be $0.17 for fiscal 2026, an improvement of 241.7% YOY, before surging by 241.2% annually to an EPS of $0.58 in fiscal 2027.

What Do Analysts Expect for Intel Stock?

Recently, Evercore upgraded Intel Corporation to “Outperform” and raised its price target to a Street-high $111 from $45, citing improved execution, a rebound in CPU demand, and Intel’s strategic position.

On the other hand, DA Davidson raised its price target on Intel Corporation to $77 from $45 but maintained a “Neutral” rating, citing a strong Q1 earnings beat.

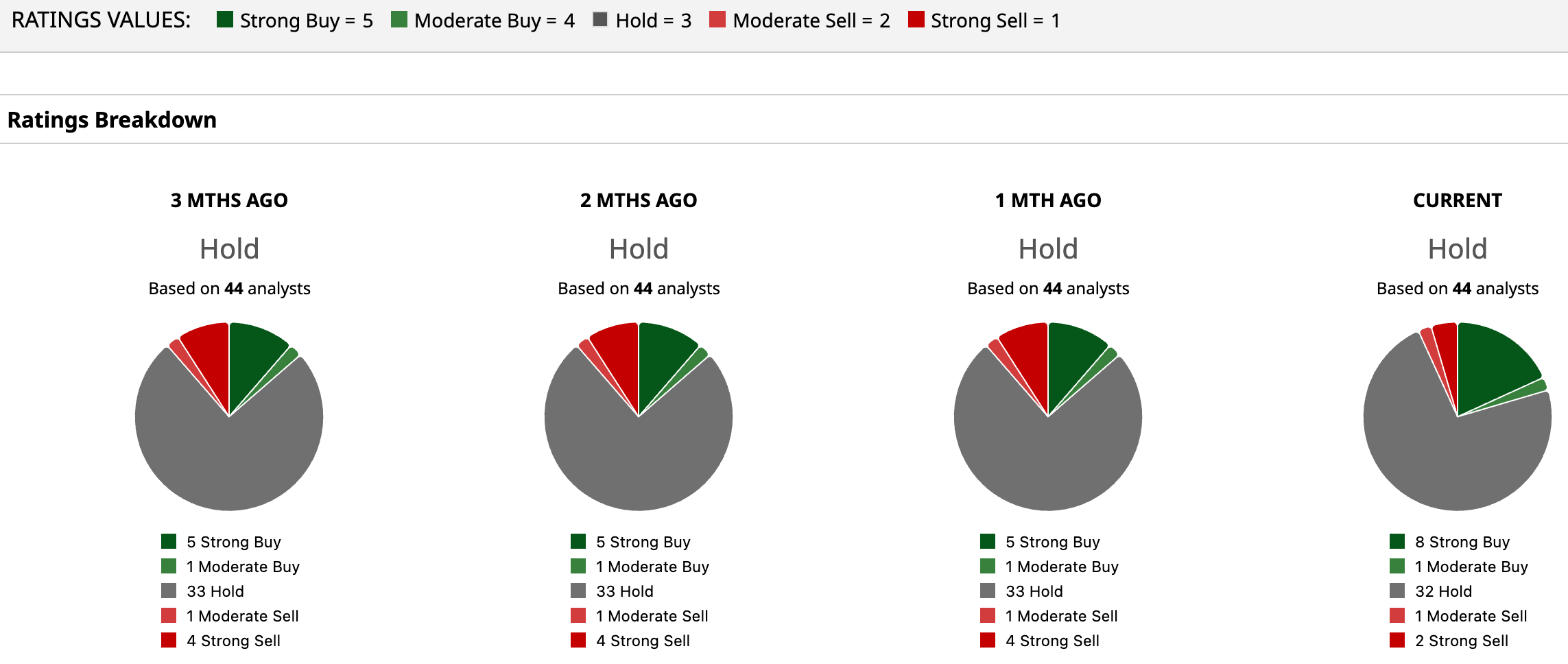

Overall, INTC has a consensus “Hold” rating. Of the 44 analysts covering the stock, eight advise a “Strong Buy,” one recommends a “Moderate Buy,” 32 analysts are on the sidelines, giving it a “Hold” rating, one suggests a “Moderate Sell,” and two propose a “Strong Sell.”

INTC has already surged past the average analyst price target of $74.54, while Evercore’s Street-high target price of $111 suggests that the stock could rally 34.8%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Super Micro Computer Just Announced Its Largest-Ever U.S. Location. Does That Make SMCI Stock a Buy Here? Why the Real Story Behind the UAE’s OPEC Exit is Petrodollar Diplomacy Verizon Stock Had Its Best Day Since January as Investors Bet on a Multibillion-Dollar Hyperscaler Deal. Should You Buy VZ? The Amazon-Meta Deal Just Highlighted Another Reason to Hold Intel Stock