Shares of Verizon Communications (VZ) stormed back into the spotlight on Monday, as the telecommunications giant delivered a Q1 earnings beat and lifted its fiscal 2026 guidance, fueled by stronger-than-expected postpaid subscriber growth and solid profit expansion. Investors didn’t hesitate, pushing the stock to its biggest one-day gain since January. Alongside a strong Q1 showing, another major highlight emerged during the earnings call.

On the earnings call, management revealed it is in “deep discussions” with hyperscalers around fiber and 5G partnerships, laying the groundwork for a major push into software-defined networks, greater scalability, and the use of 5G to power artificial intelligence (AI) infrastructure. Leadership framed this as a multi-billion-dollar revenue opportunity, calling the investment “absolutely essential” to Verizon’s long-term strategy. CEO Dan Schulman also spotlighted Verizon’s growing AI push, noting close collaboration with Alphabet (GOOG) (GOOGL) and Anthropic to unlock operational efficiencies and elevate customer satisfaction.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Given this backdrop, is Verizon now evolving into a compelling AI-driven growth story worth buying into?

About Verizon Stock

A cornerstone of modern connectivity, Verizon Communications powers how millions of customers live, work, and play, delivering mobility, reliable network connectivity, and security across an increasingly digital world. From its expansive wireless footprint to broadband, fiber, and enterprise solutions, the company supports operations for businesses of all sizes, including nearly all of the Fortune 500.

Formed in 2000 and headquartered in New York City, Verizon has steadily expanded its global reach, serving customers across multiple countries while remaining a critical player in communications infrastructure. In 2025, the company generated roughly $138.2 billion in revenue, underscoring its scale and market presence.

As the next wave of technology unfolds, Verizon is leaning deeper into artificial intelligence, using it to boost network efficiency, streamline operations, and elevate the customer experience, while pairing it with its expanding 5G capabilities to support increasingly data-intensive applications. That strategy reached a pivotal moment in early 2026, when Verizon closed its Frontier Communications acquisition in January.

By combining Frontier’s high-speed fiber network with its industry-leading 5G platform, Verizon is set to extend its reach to nearly 30 million fiber passings across 31 states and Washington, D.C., strengthening its network edge while delivering greater value and choice to millions more customers.

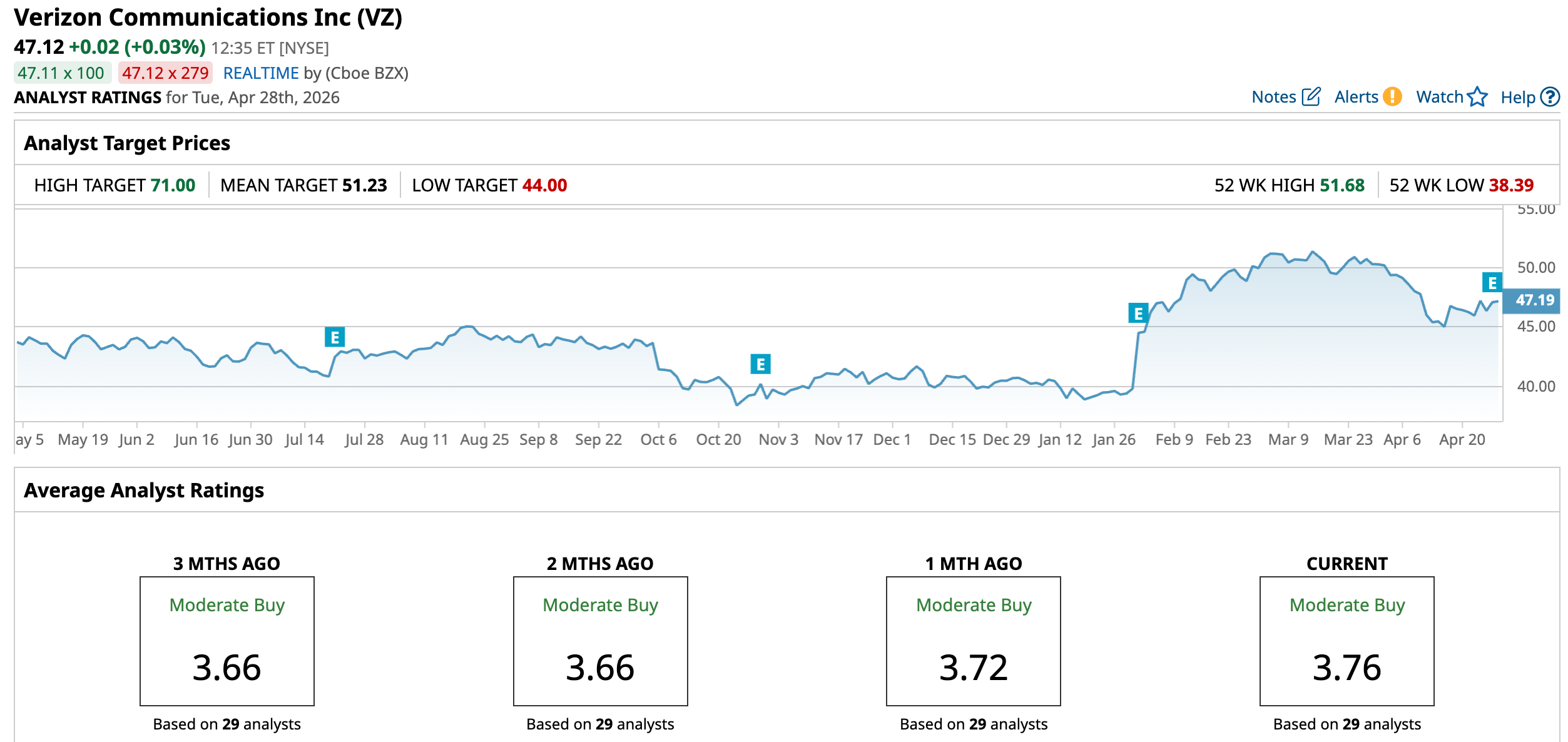

The telecommunications giant has been quietly flexing its strength on Wall Street. With a market capitalization of roughly $196.9 billion, the stock is up an impressive 16% so far in 2026, comfortably ahead of the broader S&P 500 Index ($SPX), which has gained just 4% in the same period. Shares rallied to a 52-week high of $51.68 on March 24, and although they’ve since eased about 8.7% from that level, the stock continues to hold its ground as a notable outperformer in the broader market.

www.barchart.com

www.barchart.com Verizon has long been a reliable income play, with a solid track record of rewarding shareholders through 21 consecutive years of dividend growth. The company is set to pay its next quarterly dividend of $0.7075 per share on May 1, reinforcing its commitment to steady payouts. At current levels, Verizon’s forward annualized dividend of $2.83 per share translates to an attractive 6.1% yield, making it a compelling option for income-focused investors seeking both stability and consistent returns.

A Look Inside Verizon’s Q1 Earnings Performance

Verizon kicked off fiscal 2026 on a strong note, even as the headline numbers told a slightly mixed story. The telecom giant reported first-quarter results on April 27, delivering a better-than-expected bottom line and solid postpaid phone net additions, factors that ultimately outweighed concerns around a modest revenue miss.

Total operating revenue came in at $34.4 billion, up 2.9% year-over-year (YOY), but just shy of the $35.03 billion consensus estimate. The shortfall was largely driven by a disciplined pullback in aggressive promotional spending, along with a one-time 80 basis point hit to wireless service revenue tied to customer credits following a major network outage in January.

Nevertheless, despite the top line miss, Wall Street zeroed in on the positives, sending shares up almost 1.6% on Monday. Verizon delivered a notable earnings beat, with adjusted EPS of $1.28, up an impressive 7.6% YOY, marking its strongest quarterly growth since 2021 and comfortably ahead of the $1.22 consensus estimate.

However, the biggest headline was subscriber momentum. Verizon posted a surprise gain of 55,000 postpaid phone subscribers, its first positive first-quarter net addition in this category since 2013, signaling a meaningful shift in momentum. Growth extended beyond wireless. Verizon added 341,000 broadband subscribers in Q1 2026, including 214,000 fixed wireless access additions and 127,000 fiber broadband net adds.

The company now boasts approximately 16.8 million fixed wireless access and fiber broadband connections, underscoring its expanding footprint in next-generation connectivity. On the financial front, Verizon continued to strengthen its balance sheet and return capital to shareholders. The company has already paid down roughly half of Frontier’s debt since the acquisition closed and expects to eliminate substantially all of it by year-end.

It also completed $2.5 billion in share repurchases during the quarter and remains on track to meet its full-year target of at least $3 billion. Moreover, Free cash flow rose to $3.8 billion, up from $3.6 billion in the year-ago period, reflecting a 4% increase. Riding this strong momentum, Verizon raised its full-year 2026 outlook.

The company now expects adjusted EPS growth of 5% to 6%, up from its prior 4% to 5% forecast, and anticipates postpaid phone net additions to land in the upper half of its 750,000 to 1 million target range, roughly two to three times its 2025 results.

What Do Analysts Think About Verizon Stock?

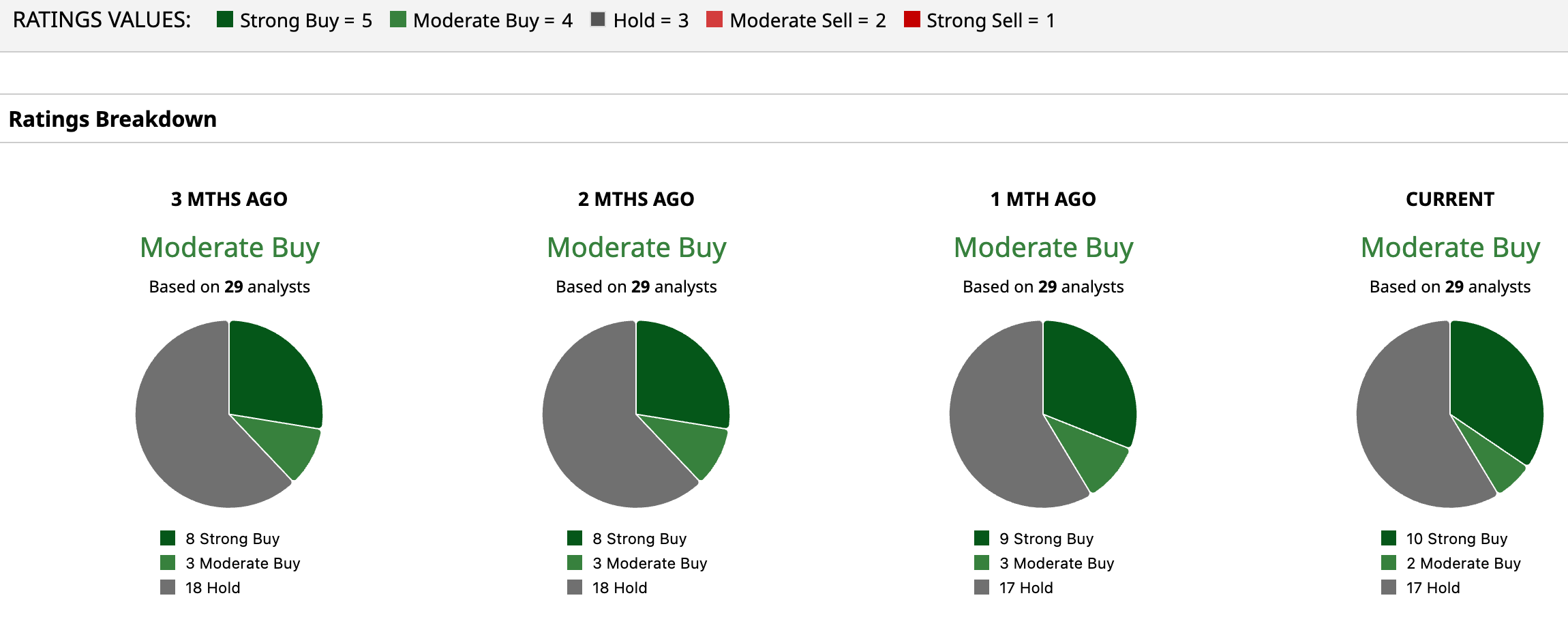

Overall, Wall Street’s stance on Verizon remains cautiously optimistic, with the stock carrying a consensus “Moderate Buy” rating. Of the 29 analysts covering the name, 10 are firmly bullish with “Strong Buy” calls, two lean positive with “Moderate Buy,” while the majority of 17 analysts remain on the sidelines with “Hold,” reflecting a balanced but watchful sentiment.

The upside story, however, still has room to run. The average price target of $51.23 implies a modest gain of 8.7% from current levels, while the Street-high target of $71 paints a far more bullish scenario, suggesting the stock could rally as much as 50.7% if execution and tailwinds align.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Verizon Stock Had Its Best Day Since January as Investors Bet on a Multibillion-Dollar Hyperscaler Deal. Should You Buy VZ? Investors Are Waiting for the Nike Stock Turnaround. Will the Latest 1,400 Job Cuts Be Enough? Newmont Is Golden: Why Record Gold Prices Make It a Must-Buy Dividend Stock Now The 3 Dividend Aristocrats Wall Street Calls a ‘Strong Buy’ With Up to 46% Upside