Qualcomm (QCOM) will release its second-quarter fiscal 2026 earnings on April 29. The company continues to benefit from steady consumer demand for smartphones and strong positioning of its Snapdragon products. Growth is also being supported by expanding momentum in its automotive and IoT segments. However, broader industry challenges, such as limited memory supply and a slowdown in chip orders, may put pressure on both revenue and earnings in Q2.

Qualcomm shares have declined approximately 12% year-to-date (YTD), underperforming the broader S&P 500 ($SPX). This suggests that investors are already pricing in some degree of cyclical weakness heading into the earnings release.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Qualcomm Q2 Earnings: Here’s What to Expect

Qualcomm’s upcoming second-quarter results are likely to reflect modest revenue contraction amid constrained memory supply. The company has guided total revenue to be in the range of $10.2 billion to $11 billion. The midpoint of $10.6 billion implies a slight year-over-year (YoY) decline from $10.98 billion. This suggests that while certain growth drivers remain intact, near-term headwinds, primarily in the handset market, will weigh on overall performance.

Within its core Qualcomm CDMA Technologies (QCT) division, the outlook remains mixed. Management expects QCT revenue between $8.8 billion and $9.4 billion. The midpoint of $9.1 billion indicates a YoY decline from $9.5 billion reported in the same quarter last year. The decline is largely attributable to ongoing softness in the handset market, with QCT handset revenues projected at $6 billion, marking both sequential and YoY declines.

A key factor impacting Qualcomm’s QCT handset revenue is the surge in demand for memory components driven by AI data center expansion. This has created supply imbalances and pricing volatility, which in turn are affecting handset manufacturers. Faced with higher input costs and uncertain supply, OEMs, primarily in China, are taking a more conservative stance on production planning and inventory management. This cautious approach has translated into reduced chipset orders for Qualcomm.

That said, underlying growth vectors within QCT remain intact. Qualcomm continues to benefit from the expansion of premium and high-tier smartphones, supported by strong adoption of its Snapdragon platforms across leading OEMs. Moreover, momentum in the automotive and Internet of Things (IoT) markets is likely to be sustained.

QCT IoT revenues are expected to grow in the low teens YoY, driven by demand across both industrial and consumer applications. Meanwhile, the automotive segment’s revenue is projected to grow by more than 35% YoY.

The Qualcomm Technology Licensing (QTL) segment is projected to generate between $1.2 billion and $1.4 billion in revenue, with a midpoint of $1.3 billion, slightly below the prior-year level.

Qualcomm’s bottom line is expected to face pressure in the quarter. An expected decline in revenue and higher operating expenses are likely to compress margins. Qualcomm projects adjusted earnings per share (EPS) of $2.45 to $2.65, down from $2.85 a year ago. Street expectations are more conservative, with analysts forecasting EPS of approximately $1.90, indicating a notable decline.

While Qualcomm’s earnings are expected to decline in Q2, investors should note that the company has exceeded analyst EPS estimates in three of the past four quarters.

Is QCOM Stock a Buy, Sell, or Hold Now?

Qualcomm continues to gain traction in expanding markets like automotive technology and IoT, which should support its future growth. Moreover, its acquisition of AlphaWave is expected to enhance its capabilities in next-generation AI data centers, providing a significant growth opportunity.

However, Qualcomm is facing short-term headwinds. Revenue growth may remain constrained due to limited semiconductor supply and softer chip demand. Earnings are also projected to decline in fiscal 2026 and could remain under pressure into 2027, raising caution for investors.

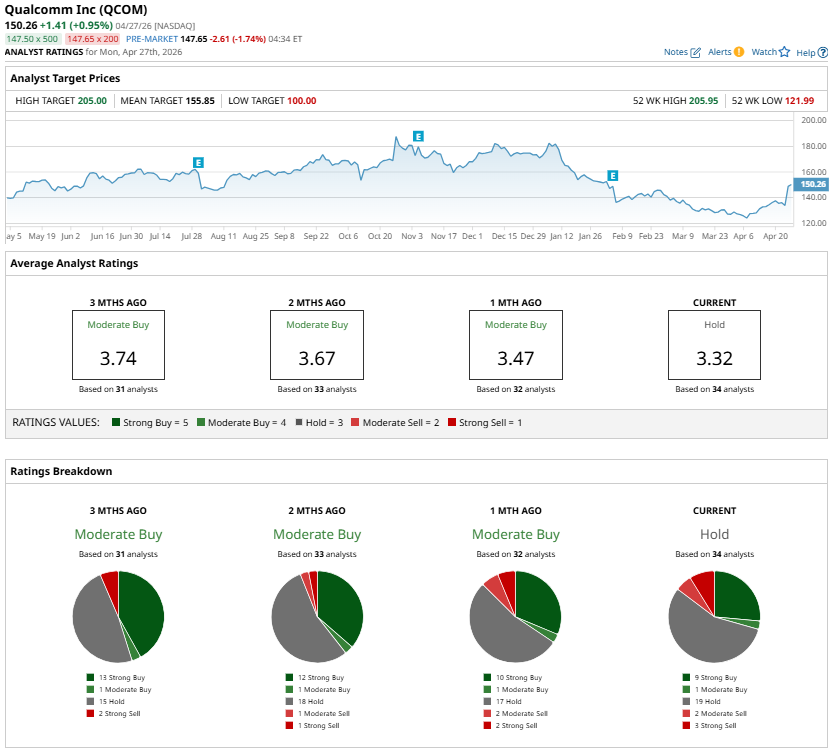

Analysts remain sidelined on QCOM stock. For now, QCOM stock carries a “Hold” consensus rating as the market looks ahead to its upcoming Q2 earnings.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SMCI Stock Alert: 2 Red Flags and 1 Green Flag About Supermicro Where is the Most Diversified U.S. Stock Market Index Heading? Memory Supply Dynamics May Hurt Qualcomm’s Q2. Is QCOM Stock a Buy, Sell, or Hold? As OpenAI Drags Down Chip Stocks, Is Applied Materials Stock a Buy, Sell, or Hold?