SoFi Technologies (SOFI) delivered a strong first-quarter performance, driven by strong members and product growth. While SoFi’s top line growth rate continued to accelerate, the market reaction has been negative, with the stock declining in pre-market trading following the announcement.

The primary concern appears to stem from full-year guidance. SoFi’s management kept the full-year net revenue and adjusted EPS guidance unchanged at $4.655 billion and $0.60, respectively, despite strong Q1 performance. This indicates softness ahead. Further, its Technology Platform segment’s top line came under pressure as a large client moved off its platform.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Notably, SoFi stock has witnessed selling pressure over the past several months. Shares have fallen 48.88% over the past six months, due to valuation concerns and dilution risk. The company’s capital-raising activities, while supportive of long-term growth initiatives, have raised concerns about dilution and weighed on investor sentiment. Moreover, persistent geopolitical tensions and a broadly uncertain economic environment have further dragged SoFi stock lower.

www.barchart.com

www.barchart.com SoFi’s Growth Engine Still Running at Full Speed

SoFi’s first-quarter results reflect that its business is scaling rapidly, with strong momentum across its core operating metrics. Member growth was solid, with 1.1 million new members added during the quarter, bringing the total to 14.7 million. This represents a 35% year-over-year (YOY) increase, reflecting sustained demand for SoFi’s integrated financial ecosystem. Product adoption also kept pace, with a record 1.8 million products added, pushing the total to 22.2 million.

SoFi highlighted that 43% of new products came from existing members, reflecting improving monetization efficiency, as existing users engage more deeply across multiple offerings.

SoFi’s solid member and product growth gave its top line a significant boost. SoFi reported adjusted net revenue of $1.1 billion, up 41% YOY. This reflects acceleration from 40% growth registered in Q4 of 2025.

The fintech’s adjusted EBITDA rose 62% to approximately $340 million, resulting in an adjusted EBITDA margin of 31%.

Supporting SoFi’s revenue and margins is its ongoing shift toward diversified and fee-based revenue streams. It reported fee-based revenue of $386.8 million in the quarter, up 23% YOY. The growth was driven by ongoing strength in its Loan Platform Business, referral fees, and brokerage services. These businesses are less capital-intensive and more resilient than traditional lending income. The continued expansion of the Loan Platform Business reflects SoFi’s shift toward a balanced and less cyclical revenue mix.

Even so, lending remains a core growth driver. Total loan originations reached $12.2 billion, with strength across personal, student, and home loans. The surge in student loan originations, in particular, reflects the normalization of that market after pandemic-related disruptions.

On the funding side, SoFi continues to improve its cost structure through deposit growth. Deposits accounted for over 90% of average total liabilities during the quarter, reflecting a strategic shift away from more expensive funding sources. This optimization of the funding base enhances profitability and strengthens its balance sheet.

The Weak Link: Technology Platform Under Pressure

Although SoFi showed overall strength, its Technology Platform, considered a high-margin, SaaS-like segment, reported a 27% YOY revenue decline. This drop was mainly due to the loss of a major client that moved off the platform.

Notably, the Technology Platform has been positioned as a key pillar of SoFi’s long-term diversification strategy. Any weakness in this segment was likely to raise investor concerns.

SoFi Stock: Buy or Avoid?

SoFi remains a high-quality growth stock, even amid short-term skepticism. The company continues to deliver strong operational performance, expand its ecosystem, and shift toward a more resilient and diversified business model.

However, the lack of upward guidance revision, weakness in the Technology Platform, and dilution concerns amid a challenging macro backdrop could restrict upside potential in the short term.

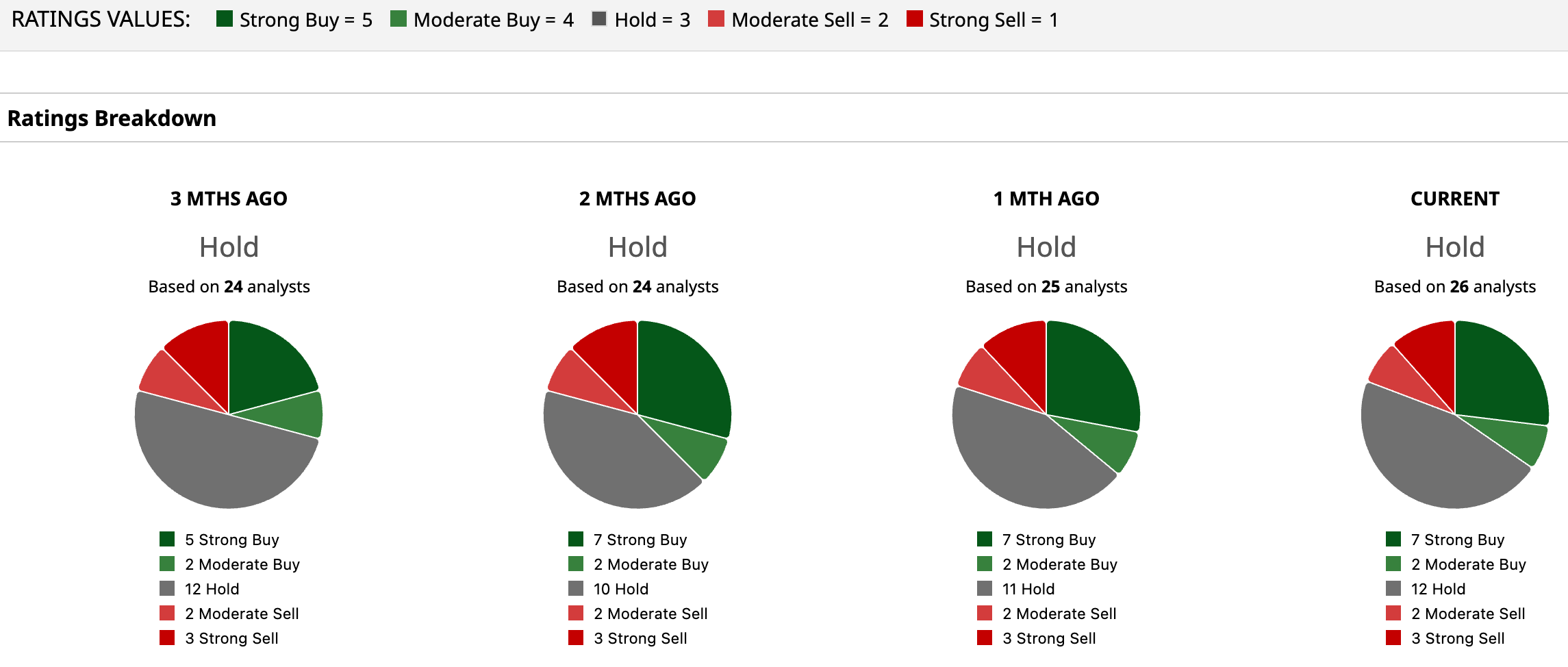

Analysts have a “Hold” rating on the stock. However, SoFi’s long-term outlook remains solid. Investors with a long-term perspective may consider adding the stock on weakness.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

The Trump Admin Officially Enters Bailout Talks With Spirit Airlines. Should You Buy Its Bankrupt Stock Here? As Nvidia Launches Nemotron 3 Nano Omni Model, Should You Buy, Sell, or Hold NVDA Stock? Why SoFi Stock Is Sliding Despite Strong Q1 Results—Buy or Avoid? Meta Platforms Is Betting on Space-Based Solar Power as AI Drives Power Demands. Northrop Grumman Stock Could Be a Winner.