nLIGHT, Inc. LASR is scheduled to report first-quarter 2026 earnings after market close on May 7.

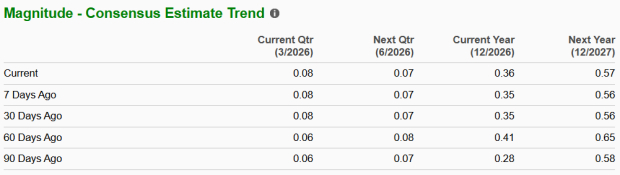

For the first quarter, LASR anticipates revenues between $70 million and $76 million. The Zacks Consensus Estimate for revenues is pinned at $71.2 million, indicating an improvement of 37.8% from the year-ago quarter’s revenues of $51.7 million.

The consensus mark for first-quarter earnings is pegged at 8 cents per share, revised up by 2 cents over the past 60 days. This signifies a robust improvement from the year-ago quarter’s loss of 4 cents per share.

Image Source: Zacks Investment Research

The stock has surpassed the Zacks Consensus Estimate for earnings twice in the trailing four quarters, matching on one occasion and missing once, the average surprise being 50.4%.

nLight Price and EPS Surprise

nLight price-eps-surprise | nLight Quote

Earnings Whispers for LASR

Our proven model does not conclusively predict an earnings beat for nLIGHT this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here.

nLIGHT has an Earnings ESP of 0.00% and carries a Zacks Rank #4 (Sell) at present. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Influence nLIGHT’s Q1 Results

The company’s first-quarter results are likely to reflect the benefits of strong demand from the aerospace and defense (A&D) end market. In the A&D space, nLIGHT is tapping into areas like directed energy systems, missile defense and laser sensing, all of which are long-term funding priorities for the Department of Defense (DoD). With defense programs benefiting from rising spending in the United States and among allied nations, the company’s A&D segment is likely to have witnessed strong year-over-year growth in the to-be-reported quarter.

The directed energy end market was a key reason behind the strong performance of its Aerospace and Defense (A&D) business in 2025. A&D revenues rose 60% year over year to a record $175 million, and management said directed energy was one of the main contributors. The company believes it is well-positioned in this market because it offers products across the full stack, from laser chips and components to high-energy laser systems and full laser weapon modules.

nLIGHT’s laser sensing products are used in missile guidance, proximity detection, range finding and countermeasures. These products are already part of several long-running defense programs, and are expected to continue growing. In the third quarter of 2025, nLIGHT signed a new $50 million contract for an existing long-running missile program that uses one of its laser sensing products. The long-running missile program remains a key priority for the customer as part of the nation's munitions restocking efforts. In the fourth quarter of 2025, nLIGHT began low-rate initial production on a new classified sensing program. This shows that nLIGHT's existing sensing programs are in full-rate production and is expected to have contributed positively to the company’s near-term prospects.

However, a key risk that weighs on nLIGHT’s first prospects is the company’s decision to exit the cutting and welding business, which will create a clear revenue headwind in 2026. Management said that this move is expected to reduce full-year revenues by around $25 million to $30 million. Further, cutting and welding were still contributing profit on incremental sales, so removing those revenues creates some near-term margin pressure. This impact was already visible in fourth-quarter results. As a percentage of revenues, nLIGHT's product gross margin declined sequentially to 37.3% in the fourth quarter, down from 41.0% in the prior quarter.

This reflects a sequential decline of 370 basis points, which was primarily due to higher inventory charges, along with lower factory utilization and a less favorable mix, related to the exit of cutting and welding. Further, for the first quarter of 2026, LASR expects product gross margins to be around 36.5% at the midpoint. This reflects another sequential decline in the company's Product gross margins and indicates that the margins will remain under pressure in the near term.

LASR Price Performance & Stock Valuation

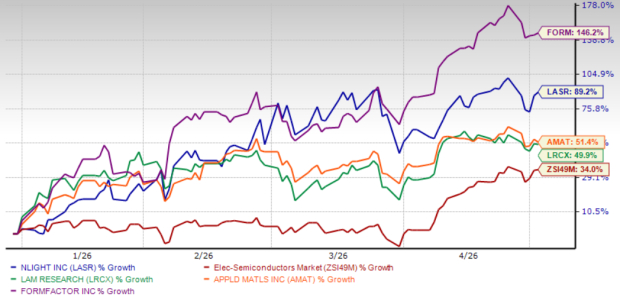

Year to date, shares of nLIGHT have surged 89.2%, outperforming the Zacks Electronics – Semiconductors industry and its peers, Lam Research LRCX and Applied Materials AMAT, while underperforming FormFactor FORM.

The Zacks Security industry has jumped 34% in the year-to-date period. Shares of FormFactor, Lam Research and Applied Materials have returned 146.2%, 49.9% and 51.4%, respectively.

YTD Price Return Performance

Image Source: Zacks Investment Research

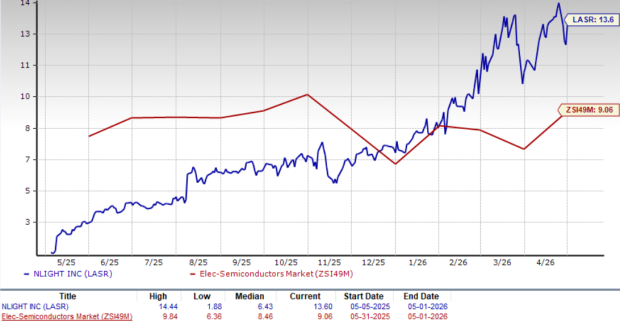

Now, let’s look at the value nLIGHT offers investors at the current levels. nLIGHT is trading at a premium with a forward 12-month P/S of 13.60X compared with the industry’s 9.06X, reflecting a stretched valuation.

Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

nLIGHT stock also trades at a higher P/S multiple compared with other industry peers, including FormFactor, Lam Research and Applied Materials. At present, FormFactor, Lam Research and Applied Materials have P/S multiples of 11.03X, 11.17X and 8.91X, respectively.

Investment Consideration for nLIGHT

nLIGHT’s decision to exit the cutting and welding business is likely to have continued weighing on its overall financial performance in 2026, as this move creates a clear gap in the company’s revenue base. Exit from the cutting and welding business creates revenue headwinds for the company, where the company forecasts this exit to reduce 2026 revenues by about $25-$30 million.

Further, margin contraction due to nLIGHT’s exit from its cutting and welding business is a key concern. Exit from the cutting and welding business means that the company is losing a business that had a positive contribution margin. Cutting and welding were still contributing profit on incremental sales, so removing those revenues creates margin pressure for the company. Rising expenses due to lower factory use and inventory-related costs, related to the exit of cutting and welding, are expected to weigh on the company’s bottom-line results.

Conclusion: Sell LASR Stock Right Now

nLIGHT is exiting its cutting and welding business, which will create revenue headwind and also pressure margins in the near term, creating a clear gap in both sales and profitability. Further, LASR’s premium valuation makes the stock look unattractive at current levels, and investors should consider staying away from the stock at present.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lam Research Corporation (LRCX): Free Stock Analysis Report

FormFactor, Inc. (FORM): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

nLight (LASR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).