The hard disk drive (HDD) industry may sound old-school in a world obsessed with chips and artificial intelligence (AI) models, but behind the scenes, it is quietly powering the rapid data surge. Every AI query, cloud application, or enterprise workload needs massive storage, and that is where HDDs still dominate, handling nearly 80% of global cloud storage demand. As AI scales, so does the need to store vast amounts of data in a cost-effective and efficient way, turning this once-cyclical sector into a key beneficiary of the AI spending boom.

So, at the center of this shift sits a tight duopoly - Seagate Technology Holdings plc (STX) and Western Digital Corporation (WDC). Together, they control the bulk of the HDD market, supplying storage solutions to hyperscalers, enterprises, and data centers worldwide. With limited competition and disciplined supply, both players are now in a sweet spot, where pricing power and demand are moving in their favor.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Lately, though, the spotlight has tilted toward Seagate. The company’s latest quarterly earnings beat expectations. Strong pricing, expanding margins, and upbeat guidance have analysts turning increasingly bullish, with some calling this cycle unprecedented. The stock responded in kind, surging sharply and lifting peers like Western Digital stock along with it.

But while Western Digital initially rode that wave, its momentum cooled after its own Q3 report. Despite posting solid numbers, the market reaction was more muted, hinting at different expectations or perhaps different trajectories.

So, while these two players are riding a powerful industry tailwind, which of these storage giants is the better stock to buy right now?

The Case For Seagate Technology Stock

Headquartered in Singapore, Seagate Technology has come a long way since its beginnings, now operating as one of the key players in global data storage. The company builds everything from HDDs to solid-state drives (SSDs), powering data centers, enterprise systems, and everyday computing.

It runs a tight ship across R&D, precision manufacturing, and a global supply chain to keep data flowing reliably. With the surge in cloud computing and AI, Seagate is doubling down on high-capacity storage innovation. Today, with a market cap of $163 billion, the company is riding the wave of the world’s exploding data needs.

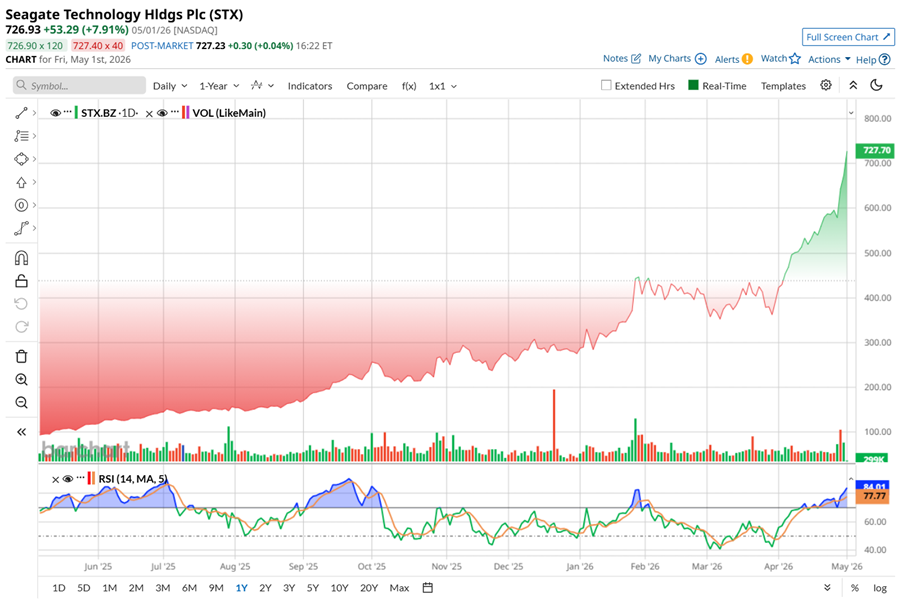

Seagate’s shares have been on an absolute tear, and it is not hard to see why. As AI infrastructure spending booms, hyperscalers are scrambling for high-capacity, cost-efficient storage, and that is exactly where Seagate shines with its advanced drives like Mozaic HAMR. As a result, we have a stock that has gone from steady to scorching.

Over the past 52 weeks, STX stock has skyrocketed an eye-popping 697.3%, with another 196.4% jump just in the last six months. In fact, 2026 was equally impressive, with the stock already up 169.4% year-to-date (YTD). Zooming in further, the momentum looks even sharper as STX rose nearly 72.8% over the past month and another 24.5% gain in just the last five days, recently hitting a 52-week high of $749 on May 4. The rally over the week has been driven by a strong Q3 report and bullish analyst outlook.

Nevertheless, the atmosphere is becoming a bit heated. Trading volumes are flashing strong buying interest, but with the 14-day RSI at 84.81, the stock is firmly in overbought territory, suggesting this rally, while powerful, may need a breather.

www.barchart.com

www.barchart.com But after a run like this, the question naturally shifts to valuation. And here, STX stock starts to look a bit stretched, though not outright extreme. The stock is priced at 44.84 times forward Non-GAAP adjusted earnings. That’s higher than the industry average but lower than its historical median. The premium is more visible when we look at its forward price-to-sales (p/s) ratio of 13.53 times, which is well above the sector average and historical median.

So, while investors are clearly willing to pay up for Seagate’s positioning in this AI-driven storage boom, expectations are running high, and that leaves less room for error going forward.

And beyond growth and valuation, Seagate Technology has built a reputation for returning cash to shareholders. The company has been paying dividends for over a decade, growing them in two years, signaling confidence in its cash flow story. Most recently, it declared a quarterly dividend of $0.74 per share, payable on July 7, 2026. That brings the annualized payout to $2.96 per share, translating to a modest forward yield of 0.44% – not massive, but steady and reliable.

Seagate Beats Q3 Expectations

On April 29, Seagate unveiled its third-quarter results for fiscal 2026, generating revenue of $3.11 billion, marking a strong 44.1% year-over-year (YOY) jump and comfortably beating Wall Street’s estimates. Profitability followed the same trend, with non-GAAP EPS surging 115.8% annually to $4.10, again ahead of expectations.

The catalyst driving this surge is AI. The explosion in AI applications is creating massive amounts of data which is pushing demand for high-capacity storage through the roof. Seagate is leaning into this with its areal density-driven strategy, allowing it to scale storage efficiently while keeping costs in check.

Consequently, the demand is evident in margins. The company posted a record non-GAAP operating margin of 37.5%, up sharply from 23.5% a year ago. Cash generation was equally strong, with $1.1 billion in operating cash flow and $953 million in free cash flow. It used that strength to clean up its balance sheet, retiring $641 million in debt, while still returning $191 million to shareholders via dividends and repurchases.

On the demand side, nearline drives – used heavily by cloud and hyperscale customers – made up about 90% of shipments, with capacity largely booked through 2027. Meanwhile, Seagate’s HAMR-based Mozaic platform is gaining traction, with its latest drives offering significantly higher capacity.

Looking ahead, the management anticipates Q4 revenue around $3.45 billion, plus or minus $100 million, representing a 41% YOY growth at the midpoint, while non-GAAP EPS is guided to $5, plus or minus $0.20.

Wall Street analysts are also equally bullish on Seagate, projecting a revenue of $3.48 billion in Q4, with EPS expected to be somewhere around $4.83. For the current fiscal year, profit is expected to rise 94.21% annually to $14.10 per share, and then grow by another 81% annually to $25.52 in fiscal 2027.

After Seagate’s Q3 earnings report, multiple brokerages have adjusted their price targets on the stock. What stood out was not just the beat, but how consistently Seagate has been outperforming expectations in this AI-driven cycle.

Morgan Stanley’s Erik Woodring captured the shift best, noting that what was once a “bull case” is now becoming the base case. He lifted his price target to $767, pointing to stronger pricing, expanding margins, and rising earnings power, all supported by booming AI data demand and tight supply in the HDD duopoly.

Wedbush echoed that optimism. Analyst Matt Bryson raised his target to $825 and reiterated an “Outperform” rating, highlighting that revenue, margins, and guidance are now exceeding even their upgraded expectations.

J.P. Morgan also leaned bullish, with analyst Samik Chatterjee increasing his target price to $775, citing a clear roadmap for capacity growth and margin expansion, especially with Mozaic gaining traction among hyperscalers.

And it did not stop there. Barclays maintained an “Overweight” rating and increased the price target from $625 to $750, while Citi raised the target to $740.

Cantor Fitzgerald’s analyst C.J. Muse raised his price target on STX from $700 to $1,000 – also the Street’s highest – maintaining an “Overweight” rating. He pointed to a strong beat-and-raise quarter, driven by surging AI storage demand, solid pricing, and expanding margins, with the business now entering a new structural growth phase.

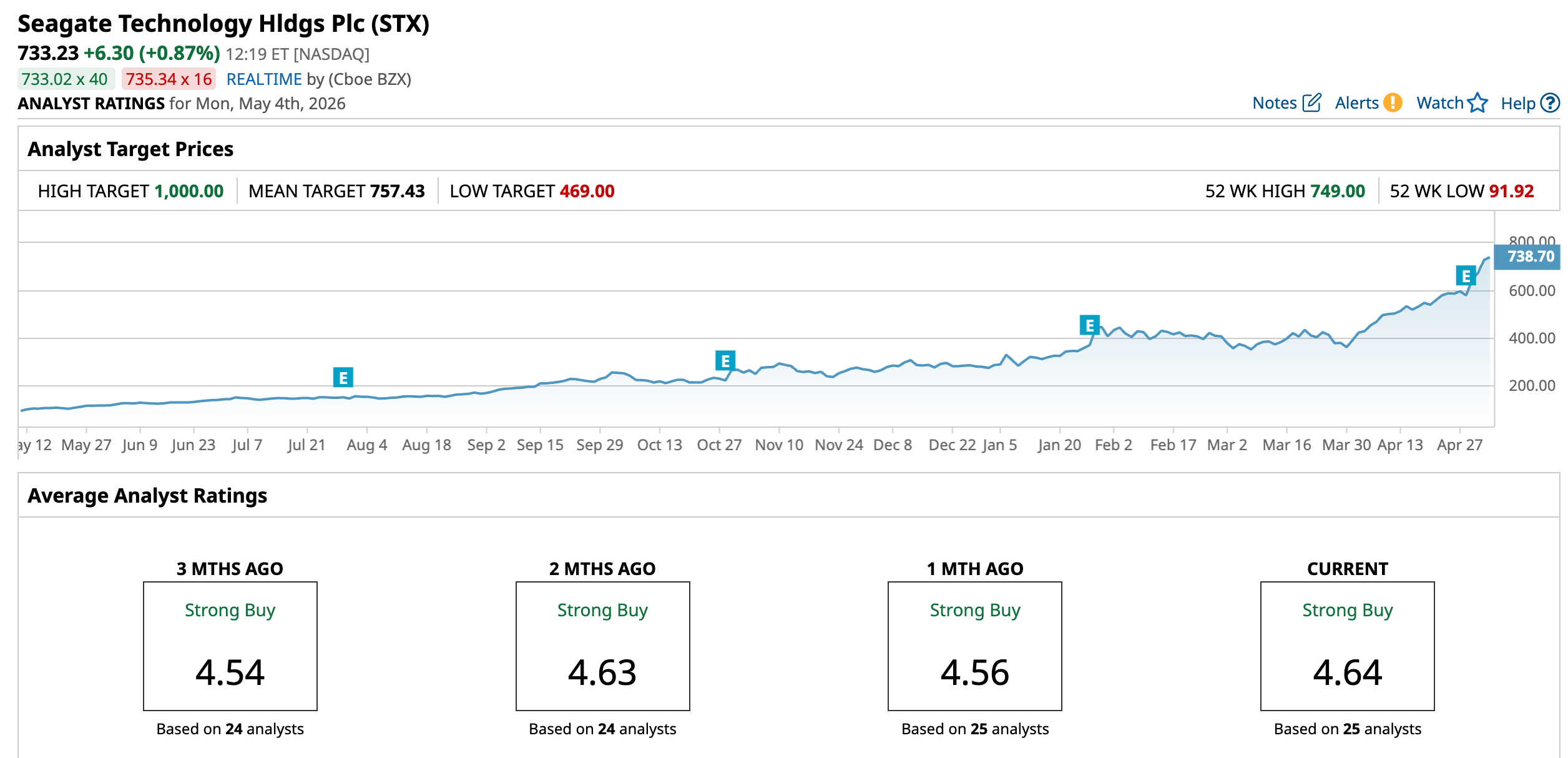

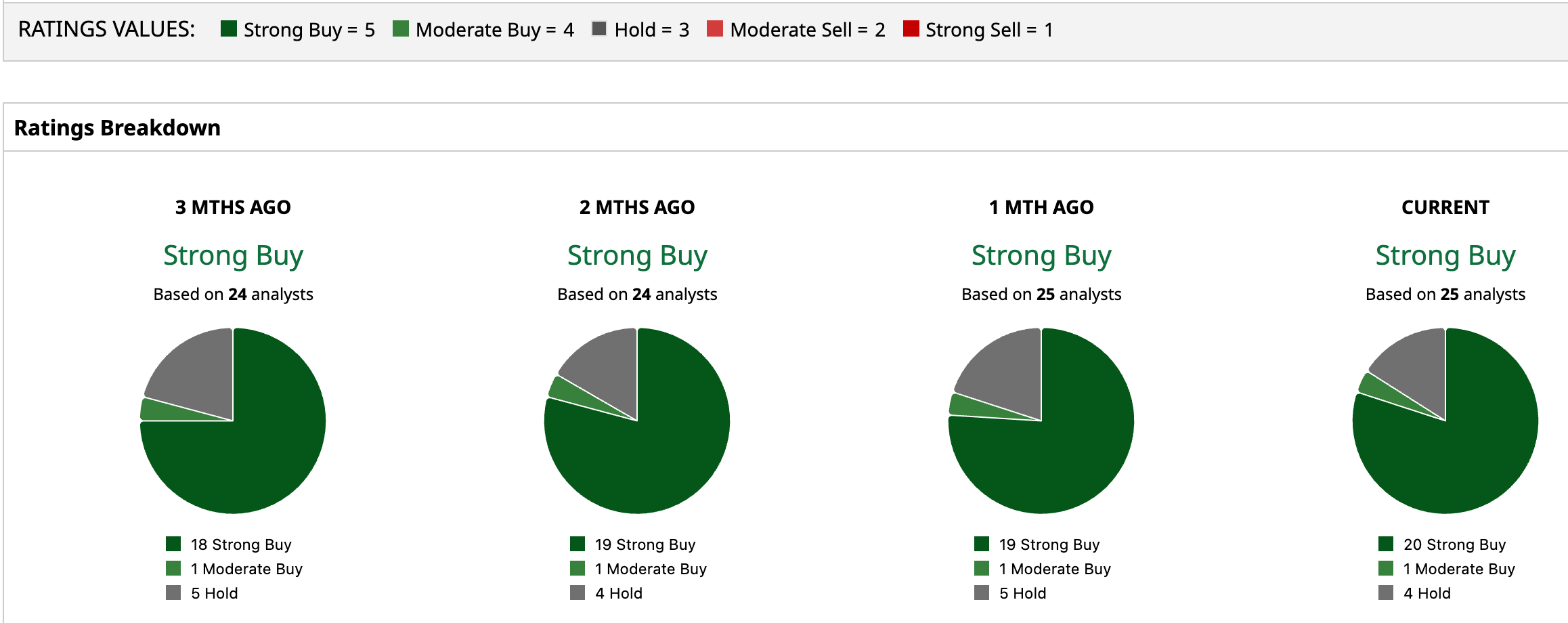

STX stock has an overall “Strong Buy” rating. Of the 25 analysts rating the stock, 20 rate it a “Strong Buy,” one has a “Moderate Buy,” and four analysts are playing it safe with a “Hold” rating.

Given the stock’s stellar rally, the mean price target of $757.43 translates into possible 3.3% upside. Yet, the Street-high target of $1,000 implies that the stock could rally as much as 36.4%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com The Case For Western Digital Stock

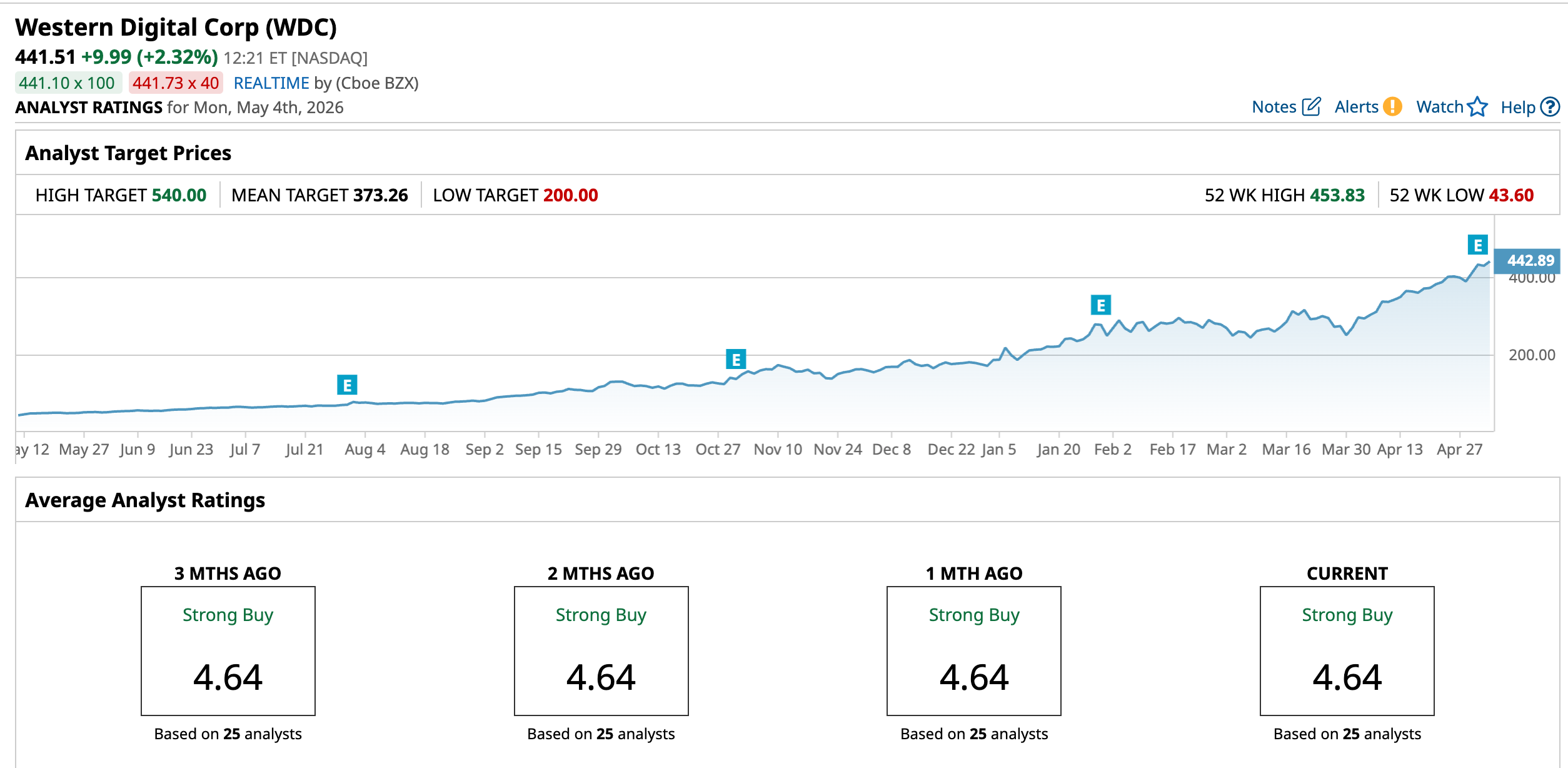

Western Digital, founded in 1970 and based in San Jose, California, is a storage powerhouse, with a $147.3 billion market cap. The company designs and sells HDD-based solutions under its Western Digital and WD brands, serving cloud providers, enterprises, and everyday consumers. Its lineup spans everything from internal and external drives to data center platforms and NAS systems.

Backed by deep R&D investments and a strong patent portfolio in magnetic recording and storage tech, Western Digital keeps pushing innovation in a highly competitive space, distributing its products globally through OEMs, retailers, and channel partners.

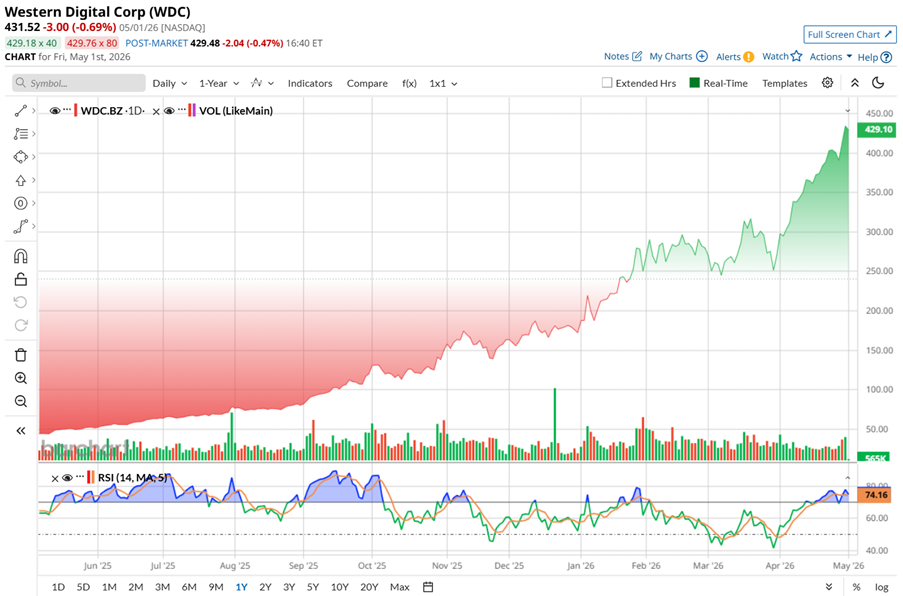

Western Digital has transformed into one of the market’s most interesting AI-storage bets, with its rally driven not by hype but by strong, fundamentals-backed growth in revenue and profitability. Over the past year, WDC stock has delivered a staggering surge of nearly 881.8%, reflecting how central its storage solutions have become in the AI ecosystem. That momentum carried into recent months as well, with shares climbing over 187% in just the last six months, as demand for high-capacity storage continues to accelerate.

The stock recently touched a high of $446.62 on May 1 before pulling back slightly by about 3.4%, and that felt more like a pause than a reversal. After all, the broader backdrop remains strong, with AI and cloud storage markets expected to grow.

Technically, though, things look stretched. With the 14-day RSI around 76, the stock is flashing overbought conditions, suggesting the rally may cool in the near term, even as the long-term trend stays intact.

www.barchart.com

www.barchart.com Valuation-wise, WDC is not exactly cheap right now. The stock is trading at around 48 times forward adjusted earnings and about 11.7 times sales, both sitting above sector averages and its own historical levels, showing investors are paying up for its AI-driven growth story.

Meanwhile, like Seagate, Western Digital also returns value to shareholders. The company recently announced a 20% increase in the quarterly cash dividend to $0.15 per share, payable to the stockholders on June 17, 2026. This comes out to about $0.60 per-share annually. But with an annualized yield of just 0.14%, income is not really the main attraction here.

Western Digital’s Q3 Earnings Snapshot

On April 30, after the market closed, the company unveiled its Q3 earnings report for fiscal 2026, posting a revenue of $3.3 billion. This represented a growth of 45% YOY and 11% sequentially as demand across AI-driven data infrastructure and cloud markets continued to accelerate. Adjusted net income per share grew 97% annually to $2.72. Both the top and bottom lines beat Wall Street’s projections.

Meanwhile, non-GAAP gross margins expanded meaningfully to 50.5%, driven by a richer mix of higher-capacity drives, disciplined pricing, and tighter cost control. Non-GAAP operating margins also jumped to 38.6%, reflecting the company's efficiency in scaling within this demand environment.

Western Digital shipped 222 exabytes during the quarter, a 34% increase from a year ago. This included 4.1 million next-gen ePMR drives, contributing 118 exabytes, with capacities reaching up to 32TB, showing how quickly advanced storage is ramping.

Financially, the company remained strong. Cash and cash equivalents stood at $2 billion as of April 3. It also sold 5.8 million SanDisk shares, cutting debt by $3.1 billion and leaving $1.6 billion in convertible debt. Operating cash flow came in at $1.1 billion versus $508 million last year, while disciplined CapEx of $145 million helped drive free cash flow of $978 million, up 124.3% annually.

During Q3, the company repurchased roughly 2.9 million shares for $752 million and paid dividends of $43 million.

Looking ahead, management expects Q4 revenue to land around $3.65 billion, plus or minus $100 million, with non-GAAP gross margins in the 51% to 52% range. Non-GAAP EPS is projected at roughly $3.25, with a possible swing of $0.15 either way.

Meanwhile, analysts tracking the company forecast its Q4 fiscal 2026 revenue to be $3.66 billion, and EPS is anticipated to grow 66.2% YOY to $2.51. For fiscal 2026, bottom line growth is projected at 91.6% YOY, rising to $8.68 per share before surging by another 57.6% to $13.68 in fiscal 2027.

Western Digital got a measured vote of confidence from UBS after its Q3 release. The brokerage firm lifted its price target to $375 from $350, while sticking with a “Neutral” rating, noting that the company not only beat expectations but also raised guidance, mirroring a similar trend seen with rival Seagate Technology earlier in the week.

Looking ahead, UBS highlighted the way Western Digital is increasingly locking in visibility. The company is already in discussions for longer-term agreements stretching as far out as 2029, though pricing typically gets finalized within a 12-month shipment window. That still gives management a solid handle on near-term volumes and guidance.

UBS also raised its EPS forecasts to $16.22 for 2026, $32.70 for 2027, and $39.01 for 2028. Margins are also expected to expand meaningfully, with gross margins projected to climb into the 70% to 75% range over the next eight quarters, reflecting improving pricing power and operating leverage.

TD Cowen lifted WDC's price target to $500 from $325, keeping a “Buy” rating, even as the stock dipped post-earnings. The firm flagged slower incremental margins and softer near-term pricing but sees no structural change, maintaining its bullish outlook with $21 EPS by 2027 and upside if pricing strengthens further.

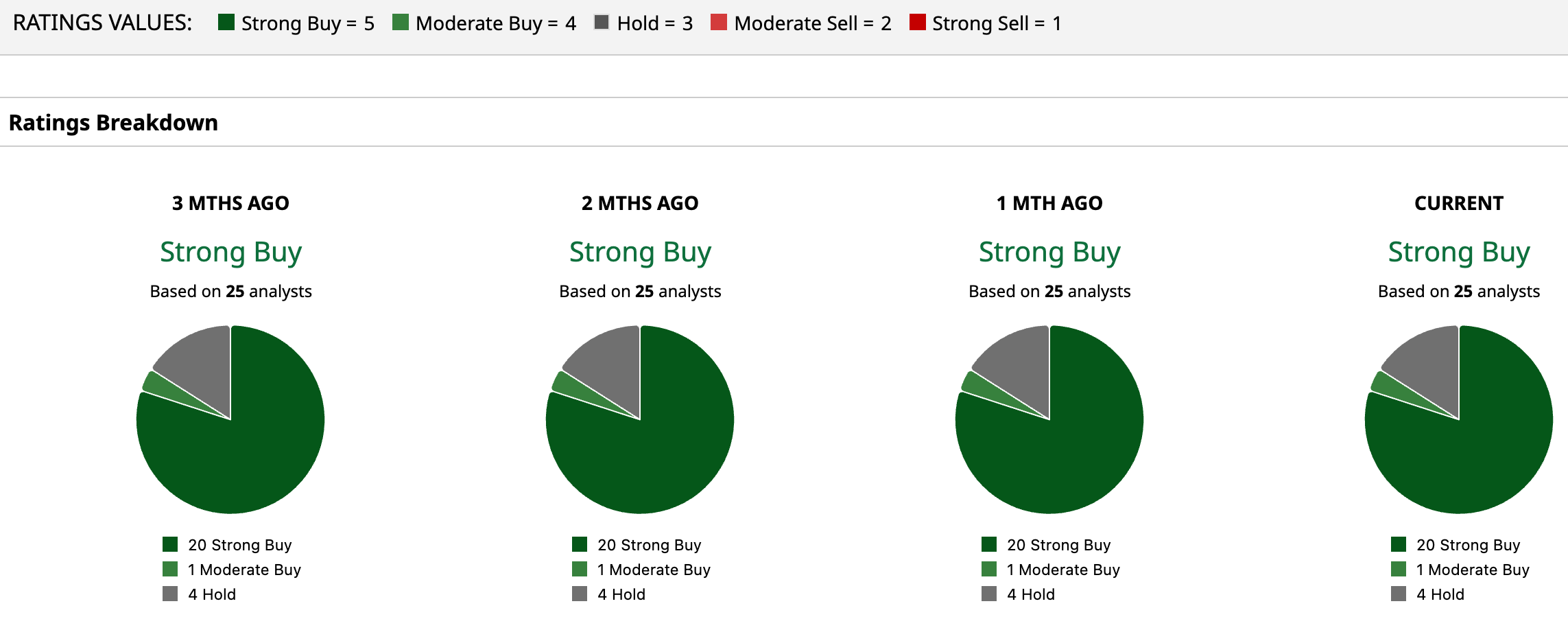

Based on 25 analysts covering the stock, WDC has a consensus “Strong Buy” rating. A majority of 20 analysts have a “Strong Buy” rating for the stock, one analyst has a “Moderate Buy,” and four analysts are on the sidelines, giving it a “Hold” rating.

WDC’s impressive rally has pushed it higher, and the stock now trades far beyond the mean price target of $373.26. The most bullish price target of $540 suggests that shares could climb as much as 22.3% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com STX Vs. WDC: Which Stock Is The Better Buy?

Both Seagate Technology and Western Digital are clearly riding the same AI-driven storage boom, hitting new highs, but they are not playing out the same way.

Seagate is the momentum winner right now, exhibiting stronger recent stock performance, slightly better valuation comfort, increasingly aggressive analyst bullishness after its earnings, and more upside potential. It is also showing solid margins and better near-term earnings upgrades, which are keeping sentiment very upbeat.

Meanwhile, Western Digital is also growing fast and improving margins, but the reaction has been a bit more mixed. Analysts are still positive, just more balanced, and there are some concerns around near-term pricing pressure even though the long-term story looks strong.

So if we go purely by momentum and current market excitement, STX looks like a better buy. But if one wants a steadier, slightly more value-leaning play, Western Digital still stays in the game.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

PayPal Needs to Focus on Growth, So Exercise Caution with PYPL Stock Before May 5 Caterpillar Stock Is Anything but Boring as a Data Center Boom Lifts Shares 170% AMD Q1 Earnings Preview: Investors Are Betting That AI Demand Can Push AMD Stock Higher Why Microsoft’s Misfires Could Create a Contrarian Opportunity in MSFT Stock