Quantum computing stocks have been on the heels lately. World Quantum Day, which was held on April 14, saw IonQ and peers surge on breakthrough announcements.

IonQ (IONQ) revealed a “foundational” milestone, photonically linking two trapped-ion quantum systems, and landed a DARPA networking contract. These developments reignited interest in the sector after a quiet first quarter.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Now, all eyes turn to IonQ’s Q1 2026 earnings, due May 6 after market close. The company will host a conference call that evening to discuss results and guidance. With quantum computing momentum building, investors are marking calendars for the May 6 report.

About IonQ Stock

IonQ is a pioneering quantum computing hardware firm. It builds ion-trap quantum systems and claims record “world-class” performance, for example, a 99.99% two-qubit gate fidelity. Its 5th-generation “IonQ Tempo” machines are offered via cloud partners like Amazon's (AMZN) AWS and Microsoft (MSFT). The company touts itself as the first full-stack quantum platform covering computing, networking, sensing, and security.

Also, in early 2026, IonQ became the first public quantum company to exceed $100 million in annual revenue.

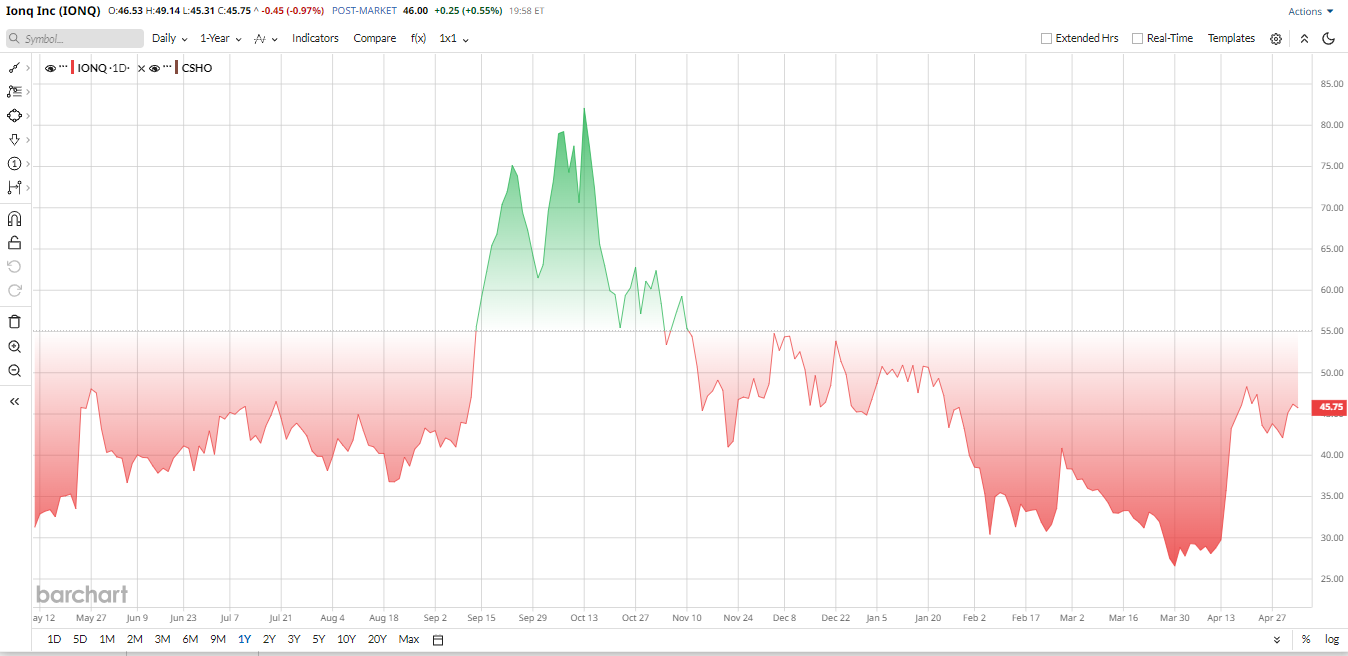

Despite these breakthroughs, so far this year, IonQ stock hasn’t made much progress overall. It’s roughly flat for the year, trading around the mid-$40s in early May, after dropping about 20% earlier in March due to profit-taking and concerns about how expensive the stock had become.

When it comes to valuation, IonQ still looks very pricey by traditional standards. The stock trades at 98.65 times sales, and 4.37 times book value. Even if you factor in its large cash reserves of $3.3 billion, the valuation remains high, with enterprise value still 110 times sales, far above typical for most companies.

www.barchart.com

www.barchart.com May 6 Earnings Outlook

The headline news is that IonQ will report Q1 2026 results on a conference call on May 6 at 4:30 p.m. ET. This release will cover the quarter ended March 31, 2026.

Wall Street forecasts roughly $48 million - $51 million in Q1 revenue, with an implied EPS of –$0.55. Analysts will closely watch whether IonQ can hit that range. Hitting guidance would support the recent optimism; a miss might reinforce concerns about lumpiness.

Looking back, IonQ has beaten estimates in recent quarters. For instance, Q4 2025 revenue crushed the high end of guidance by 55%, and full-year revenue of $130 million surpassed all expectations.

Wedbush notes that if IonQ “delivers within its FY2026 range, FY2025 will look like the start of a repeatable growth ramp”. Investors will also glean qualitative clues: commentary on the SkyWater acquisition pending close in Q2/Q3, customer demand trends, and any updates on product roadmaps.

Given IonQ’s prior volatility, the stock could swing 10% - 15% around the print. Options-implied moves suggest investors expect a big reaction, consistent with the 13% - 15% moves in past quarters.

Wall Street Take on IonQ

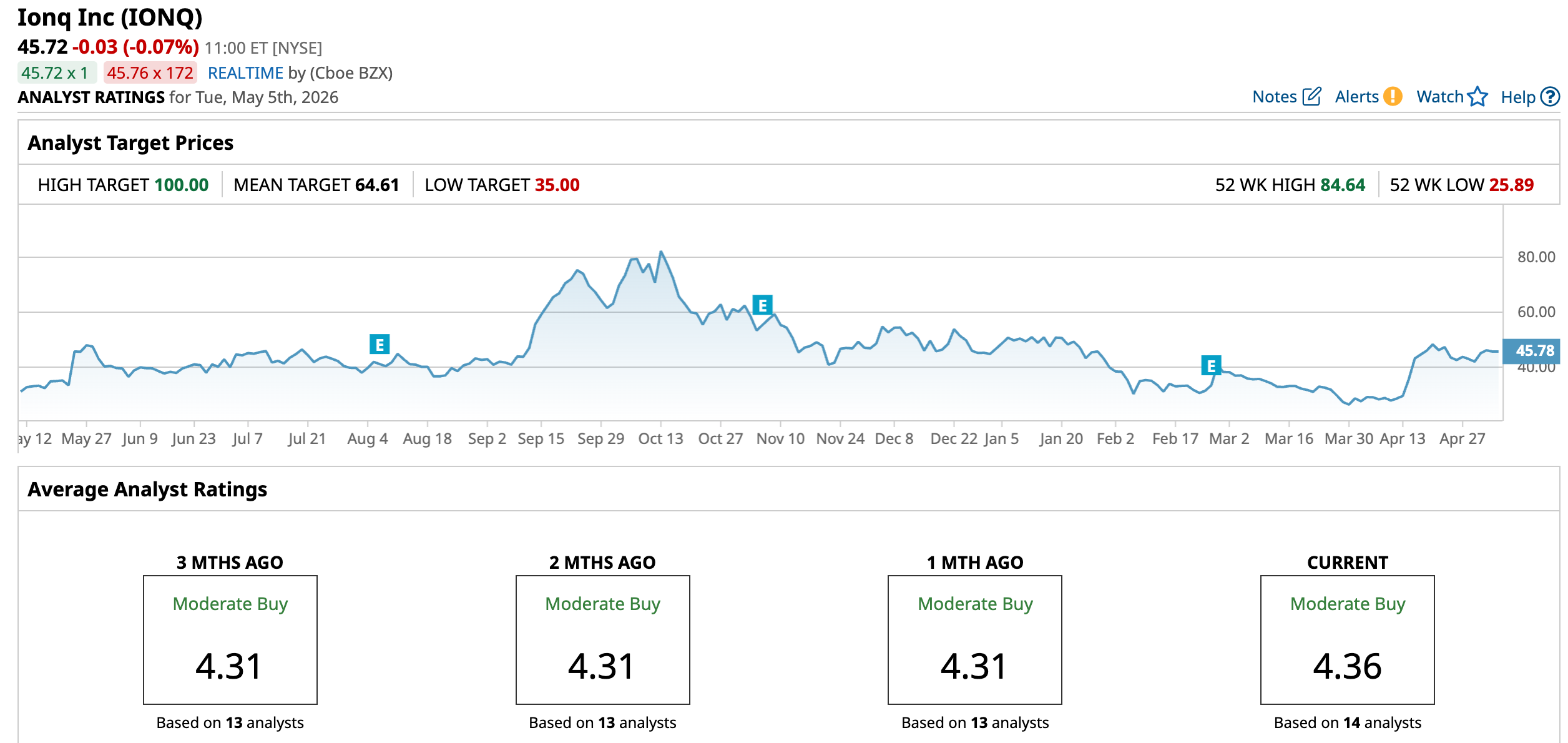

The recent analyst update indicates both the opportunity and the risk. Morgan Stanley increased its price target to $58 after IonQ exceeded its AQ-64 benchmark well in advance of the originally projected 15 hours of run time.

In the meantime, Wedbush Securities maintained its “Outperform” rating and target of $60. Both cited the progress of fault tolerance of IonQ as a primary reason that the company may remain ahead of the pack, even as it also encouraged investors to follow near-term revenue execution and fault tolerance more closely by IonQ.

Northland Capital Markets opened coverage with a target of $55, labeling IonQ as a revenue leader in the quantum space, but not overlooking the downside risks associated with continuing to incur losses, and whose valuation remains stretched.

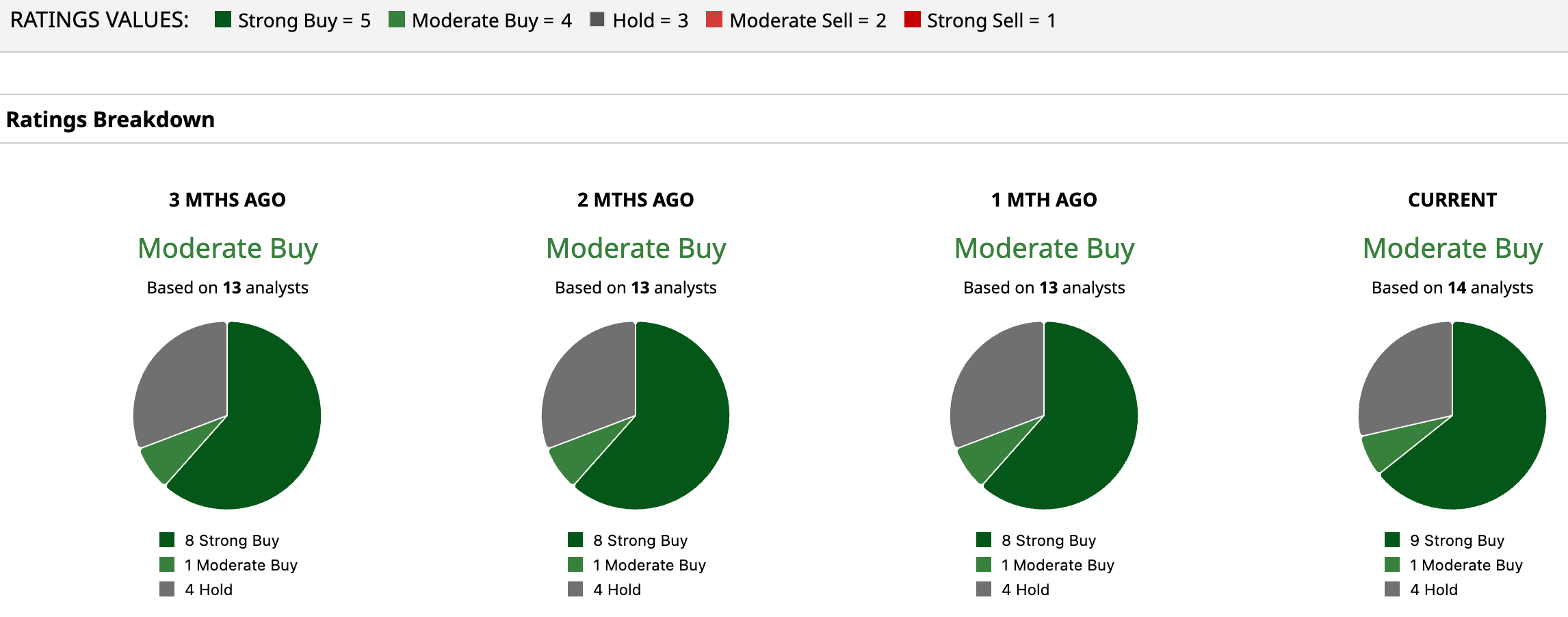

Wall Street is cautiously optimistic about IonQ heading into earnings, though the outlook is tempered by a healthy dose of reality. The current rating is a “Moderate Buy,” with an average price target of $64.61, implying 40.8% upside. But with prices ranging from $35 to $100, the outlook for price targets remains as unclear as ever.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com The Bottom Line

Take everything into consideration, and the story is simple: analysts believe in the long-term potential of IonQ, but the future of IonQ depends on how it is put into practice. The robust growth in revenues, restrained expenditure, and achievement of high technical milestones will carry much more weight than hype. As investors await the earnings, all eyes will be on whether the company really delivers or just promises.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Meta Stock Is Objectively Cheap at Current Levels Dear IonQ Stock Fans, Mark Your Calendars for May 6 Coinbase Layoffs Have Crypto Bros Down Bad as AI Takes Their Jobs. Don’t Be Surprised If They Get Rehired Soonish. Some Analysts Say BrightSprings Health Services Is the Best Healthcare Stock to Buy. Here’s Why.