Intellia Therapeutics (NTLA) is a clinical-stage biotech firm working on CRISPR-based treatments that try to edit genes directly inside the body – basically aiming to fix diseases at their root with a one-time therapy. But NTLA stock has not exactly followed that story. Even with steady clinical progress, investors have stayed cautious. This is due to safety concerns circulating around gene editing, the idea of a permanent treatment still feels like a leap, competition from existing long-term drugs remaining strong, and NTLA is still burning cash with no commercial revenue yet. The stock remains nearly 95% below its 2021 peak.

But where the market hesitates, Cathie Wood leans in. Through her ARK Innovation ETF (ARKK) and ARK Genomic Revolution ETF (ARKG), she recently picked up over 3.4 million shares worth around $43 million. She’s been adding steadily through 2026, so Intellia has become a meaningful position across her funds.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Cathie Wood has built a reputation for spotting disruptive trends early, and that is exactly why markets pay attention. Her trades are more than just routine portfolio moves. They are often seen as signals of long-term confidence in high-risk, high-reward ideas, making them closely watched by investors looking for the next big shift.

And now, the story is getting interesting again. NTLA stock has started climbing in 2026 and, most recently, in fact, has been helped by positive Phase 3 results for its hereditary angioedema (HAE) treatment, ongoing FDA filings, and plans for a potential U.S. launch in 2027.

About Intellia Therapeutics Stock

Based in Cambridge, Intellia Therapeutics is focused on advancing CRISPR/Cas9 gene-editing therapies aimed at treating diseases at their source. Its in vivo programs work inside the body, targeting conditions like hereditary angioedema and transthyretin amyloidosis, while its ex vivo approach involves modifying cells outside the body to address cancer and autoimmune disorders. With a $1.64 billion market cap, the company is working toward making gene editing a scalable, one-time treatment option.

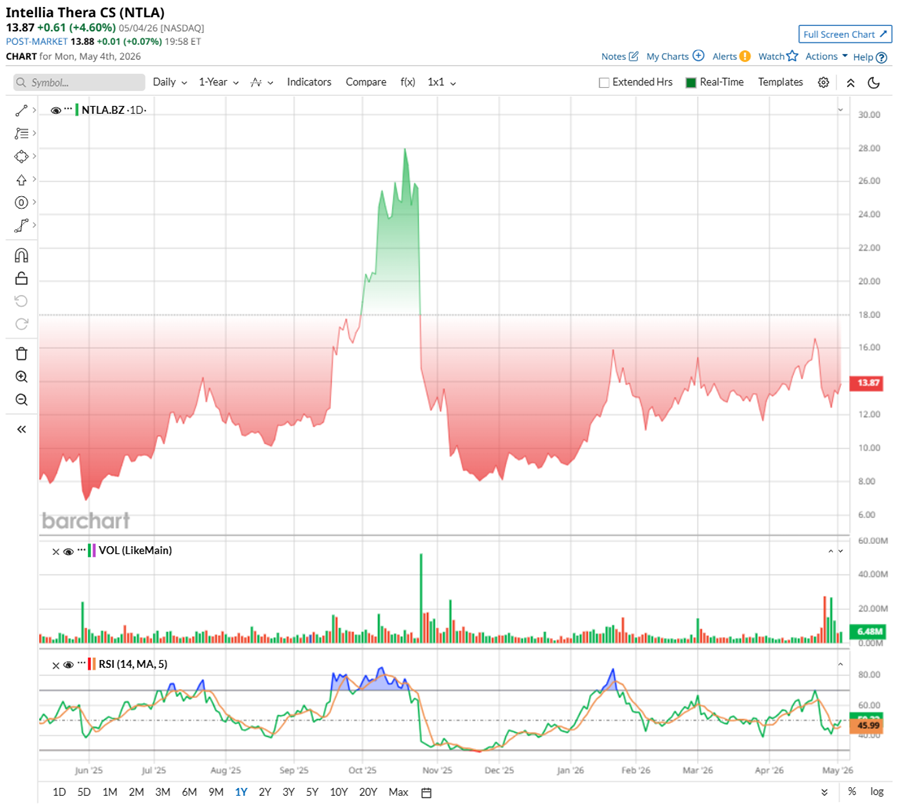

Nevertheless, the stock’s momentum has been anything but steady. Over the past year, NTLA has seen sharp swings, rising to $28.25 in late October, before pulling back nearly 50% from that peak. Even so, zooming out a bit, the trend looks steady, with the biopharma stock up 57.23% over the past 52 weeks and nearly 47.6% year-to-date (YTD).

A big part of the recent upside comes from strong Phase 3 results for its gene-editing therapy, lonvo-z, aimed at treating hereditary angioedema. The data marked a first for in vivo CRISPR therapies at this stage, and the results were hard to ignore. There was an 87% reduction in monthly attack rates versus placebo, with 62% of patients staying completely attack-free over six months. Just as importantly, the safety profile held up clean, with no serious adverse events reported.

For Intellia Therapeutics, this is not just another trial update, but a major step toward proving that a one-time, potentially curative treatment can actually work in practice, bringing its 2027 commercialization plans closer into view.

Technically, the charts reflect that mixed sentiment too. Trading volumes have started to lean positive with more green sessions, while the 14-day RSI sits at 46.70, suggesting the stock is neither overbought nor oversold, but quietly stabilizing.

www.barchart.com

www.barchart.com Valuation-wise, Intellia Therapeutics stock still trades rich at around 27.11 times forward sales, a premium to biotech peers. But it sits below compared to its own historical average, suggesting expectations have reset. Perhaps this is exactly the kind of window that keeps Cathie Wood buying into the long-term gene-editing story.

A Snapshot of Intellia Therapeutics’ Q4 Results

In February, Intellia Therapeutics rolled out its Q4 earnings report, and while it’s still very much a pre-commercial biotech story, there were a few notable positives. Revenue rose 73.8% year-over-year (YOY) to $23 million, ahead of Wall Street’s expectations, entirely driven by collaboration income. A big chunk of that came from its ongoing work with Regeneron Pharmaceuticals (REGN), along with a $9 million boost tied to the end of a prior agreement with privately owned SparingVision.

On the cost side, numbers looked a bit more controlled. Losses narrowed to $0.83 per share, better than what the Street was expecting. R&D spending dropped about 24% annually to $88.7 million, mainly due to lower employee and compensation costs, although some of that was offset by continued investment into its pipeline. General and administrative expenses stood at $33.1 million.

What really stands out is the balance sheet. Intellia ended 2025 with about $605 million in cash and investments, which it believes is enough to fund operations into the second half of 2027. That lines up with its plans to potentially launch its lead therapy, lonvo-z, for hereditary angioedema around that time.

For the full year, revenue grew 17% YOY to $67.7 million, while losses narrowed to $3.81 per share, showing gradual, steady progress.

Wall Street anticipates things can gradually turn positive for Intellia Therapeutics. Analysts expect losses to start narrowing, from 8.14% YOY improvement in 2026 to -$3.50 per share, and then a sharper 59.7% improvement in fiscal 2027 to roughly -$1.41. It is not a quick comeback story, but more like a gradual recovery of one step at a time after a pretty rough stretch.

What Do Analysts Think About Intellia Therapeutics Stock?

After a strong update from Intellia Therapeutics about its positive Phase 3 top line results for lonvo-z in HAE, Whitney Ijem from Canaccord Genuity raised the price target to $58 from $48 and maintained a “Buy” rating, signaling growing confidence in the NTLA stock’s outlook.

Adding to that, Citizens also nudged NTLA’s price target slightly higher to $30 from $28, while keeping an “Outperform” rating. The brokerage firm sees the Phase 3 HAELO results as a big step forward, especially for hereditary angioedema patients, pointing to the potential of a one-time treatment that clearly stands apart from existing options.

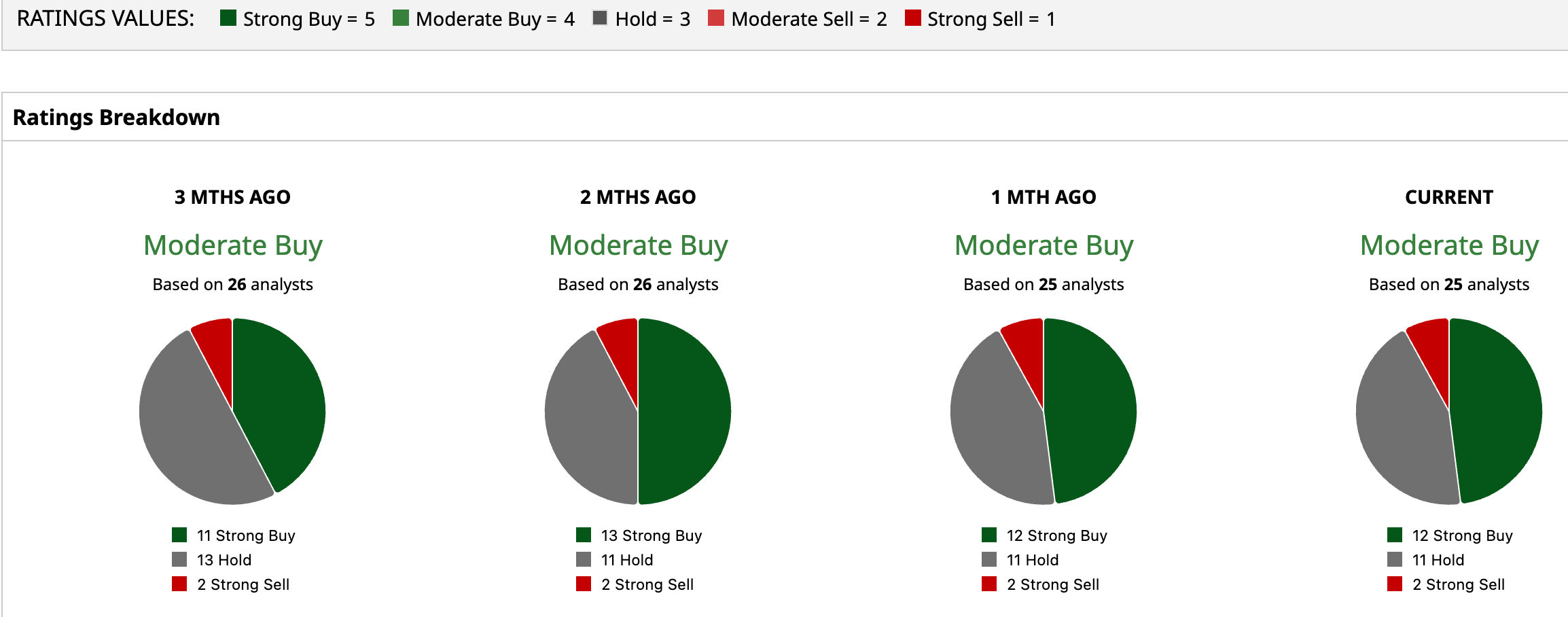

While still overall bullish, Wall Street’s tone is a little cautious. NTLA has a consensus “Moderate Buy” rating overall. Of the 25 analysts rating the stock, 12 analysts recommend a “Strong Buy” rating, 11 are cautious with a “Hold” rating, and two analysts are outright skeptical with a “Strong Sell” rating.

The consensus price target of $26.30 represents 98.5% potential upside from current levels. The Street-high price target of $95 implies that NTLA could rise 617% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intellia Therapeutics Stock Is Down Nearly 95% From Its Record Highs but Cathie Wood Keeps Buying Intel Jumps as Apple Explores Chip Deal. Here's How You Should Play INTC Stock Now, According to Barchart Data. Dear Microchip Technology Stock Fans, Mark Your Calendars for May 7 Unity Software Stock Is Down Nearly 40% YTD but Wedbush Is Pounding the Table Ahead of Earnings