Shareholders of memory chipmaker SanDisk (SNDK) just got another chance to rejoice. The company recently authorized its first-ever buyback program since its separation from Western Digital (WDC) — to the tune of $6 billion. CFO Luis Visoso highlighted the rationale behind the move, saying management's goal is to "invest in the business, achieve a net cash position, and then return cash to shareholders."

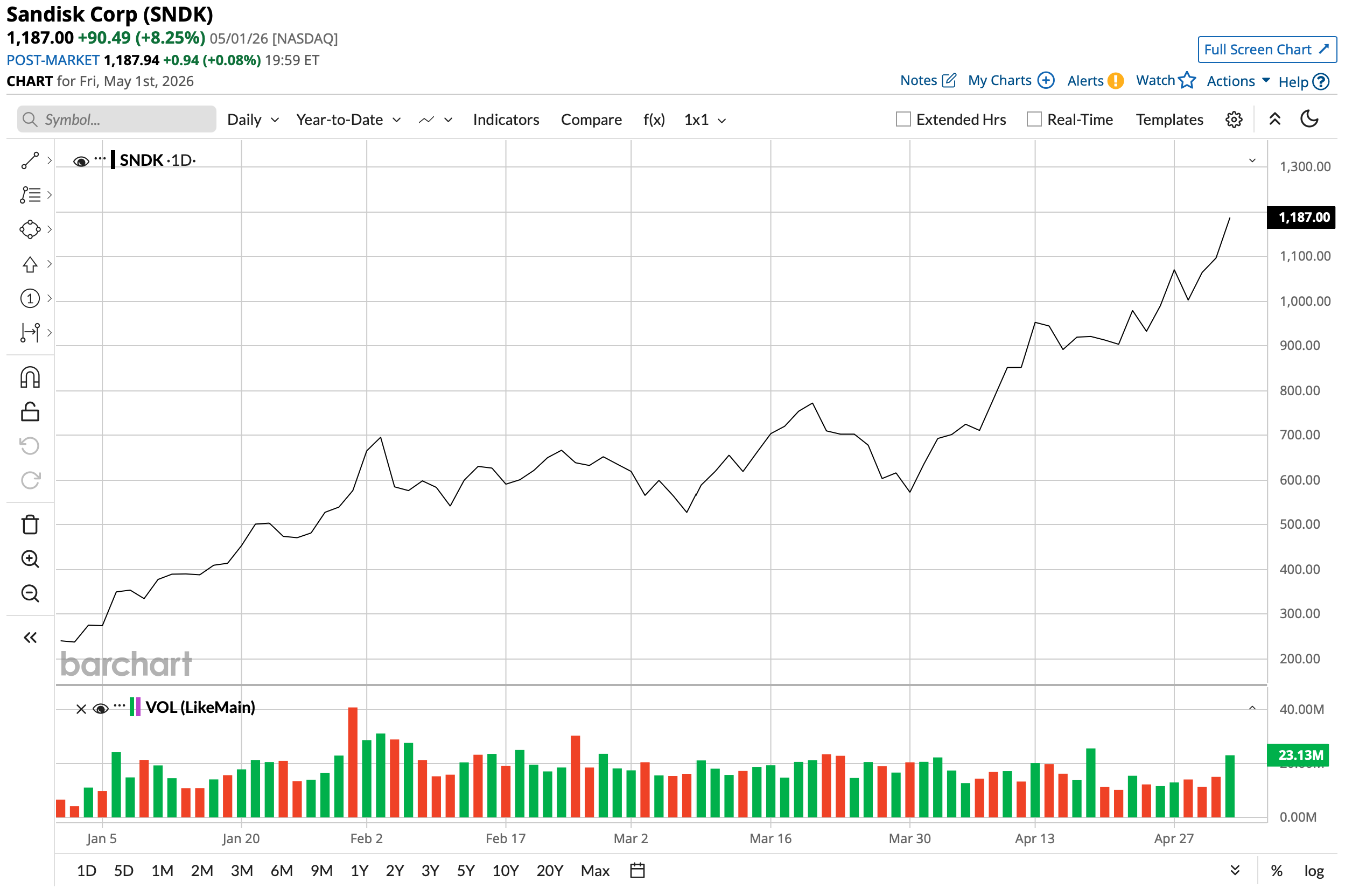

SanDisk, which has been on a sensational run thanks to unstoppable memory demand due to the AI infrastructure buildout, also reported its third-quarter results for fiscal 2026 on April 30. After reporting another blowout quarter, SNDK stock is up a whopping 495% year-to-date (YTD). Its market capitalization currently sits at $185 billion.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Has very strong demand, another set of better-than-expected quarterly results, and now the buyback move made owning SNDK stock an absolute no-brainer? Or are there chinks in the armor? Let's take a closer look.

www.barchart.com

www.barchart.com No Complaints With Q3 Numbers

SanDisk's results for Q3 2026 reflect how demand for the company's chips remains the least of its concerns. Revenue jumped 251% year-over-year (YOY) to $5.95 billion as the Datacenter and Edge segments — two primary sources of revenue for the company — climbed by 645% YOY and 295% YOY to $1.47 billion and $3.66 billion, respectively. Non-GAAP gross margins also shot up to 78.4% from 22.7% in the year-ago period.

Notably, non-GAAP EPS of $23.41 compared favorably to the loss of $0.30 per share reported in Q3 2025, marking yet another quarter showing an earnings beat from the company.

Net cash from operating activities came in at $3.04 billion, a considerable jump from a mere $26 million in the year-ago period. Overall, SanDisk ended Q3 2026 with a cash balance of $3.74 billion, with no short-term debt on its books.

For Q4, SanDisk guided for revenue of $7.75 billion to $8.25 billion, as well as non-GAAP EPS between $30 and $33. Wall Street expectations are for $8.15 billion in revenue and earnings of roughly $33 per share.

Meanwhile, after such a scorching rally in its share price, investors could not be blamed for thinking that SanDisk might be trading at unreasonably overvalued levels. But that's not quite the case. For exmaple, SanDisk's forward price-to-earnings (P/E) ratio of 25 times is resonable compared with the sector median.

SanDisk Is a NAND King

In my last analysis of SanDisk, I shed light on what gives the company a competitive edge in the memory chip race. Now, as the demand for AI continues to soar, hyperscalers are shifting their memory needs to NAND along with DRAM, which bodes well for SanDisk.

To maintain and grow its market share in NAND, SanDisk's product roadmap is genuinely compelling. Its Stargate PCIe 5 QLC SSD line, powered by its BiCS8 technology, is targeting capacities of 256 TB in 2026 and 512 TB in 2027 — and potentially 1 petabyte (PB) after 2028. Away from the data center, edge SSD sales were up 30% YOY, consumer SSD sales climbed 27%, and co-branded Nintendo (NTDOY) Switch 2 microSD Express Card sales climbed in the quarter, underscoring the breadth of the demand picture. SanDisk's view that demand will outstrip supply throughout 2026 and beyond gives it pricing authority that few pure-play NAND makers can claim.

SanDisk is also looking to gain a foothold in the DRAM space. The company invested $1 billion in Nanya Technology and simultaneously entered a multi-year DRAM supply arrangement under which Nanya will supply DRAM products to support SanDisk's long-term sourcing strategy.

On the technology side, the ambitions go further. At its investor day, SanDisk revealed it is working with IMEC on a 3D Matrix Memory DRAM project with 4 to 8 gigabit capacity, aimed at addressing the growing disparity between memory bandwidth and compute capacity. There are also reports that SanDisk has been in talks with PSMC about potential manufacturing cooperation to fast-track memory output. This is not a company trying to outdo Micron (MU) overnight. Rather, it is methodically building the supply relationships and technology optionality to participate in DRAM when the moment is right.

However, some issues are certainly worth noting. For instance, the company walked away from a $63 billion domestic fab expansion in Michigan in July 2025, which raises questions about long-term production capacity independence. On the technology side, accelerating to BiCS10 will also carry the risk of lower manufacturing yields, which could eat into the very margins the company is trying to protect. And then there is the elephant in the room, which is that the memory industry is notoriously cyclical. Today's elevated margins could compress quickly if NAND supply catches up to demand in 2027, as it historically tends to do once profitability draws out capacity additions from all the major players.

What Do Analysts Think of SNDK Stock?

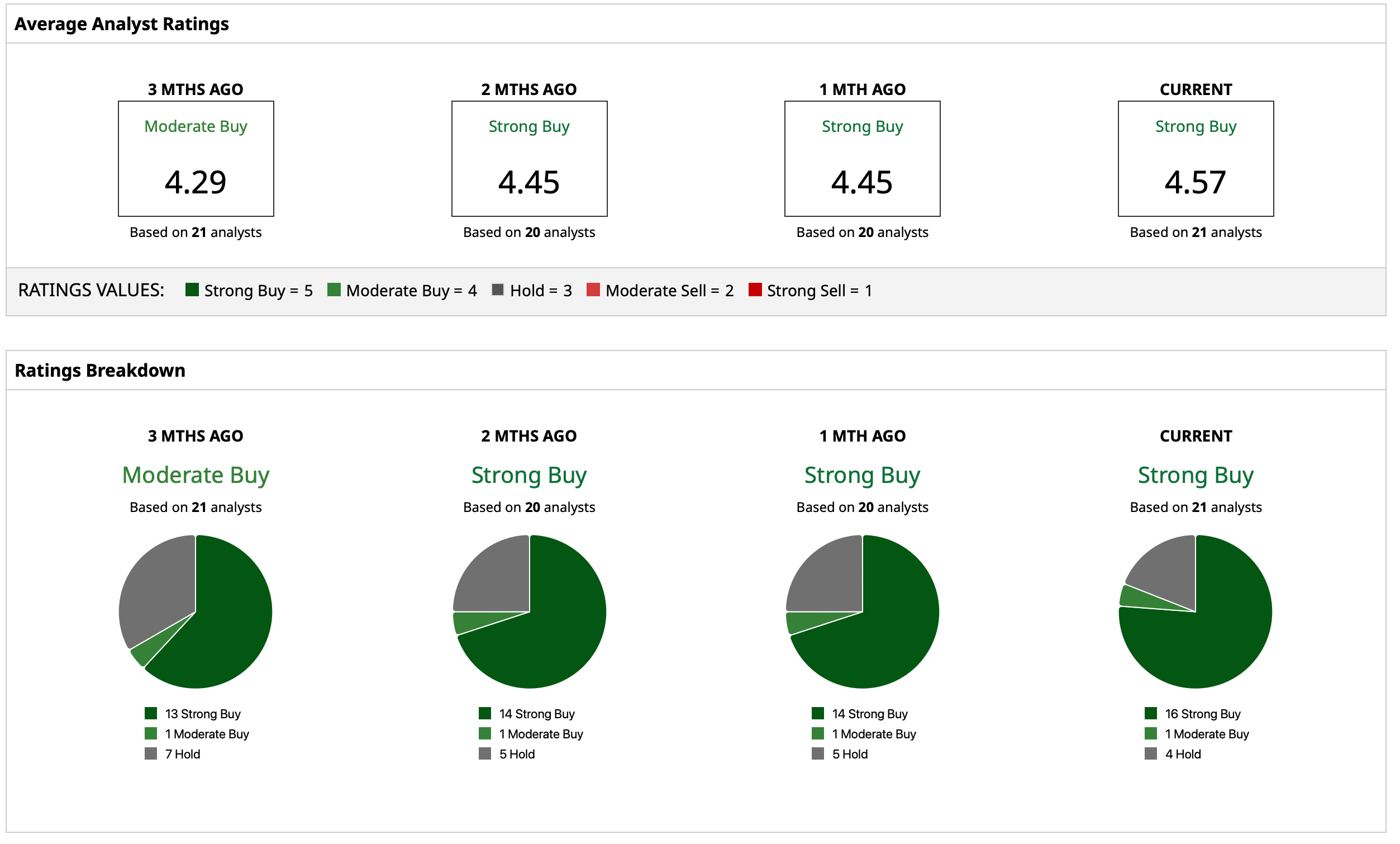

Aanalysts have a consensus “Strong Buy” rating on SNDK stock overall. The mean target price of $1,311.28 has already been surpassed by shares. Meanwhile, the high price target of $2,000 indicates potential upside of about 42% from current levels. Out of 21 analysts covering the stock, 16 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and four have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

PayPal Shares Are Sliding Despite Earnings Beat. Here's Why. A $6 Billion Reason to Buy SanDisk Stock Here Cathie Wood Remains Convinced on CoreWeave After 78% YTD Rally in CRWV Stock Ahead of AMD Earnings, Here Is What Barchart Options Data Shows for AMD Stock