SM Energy Company SM posted a quarterly earnings beat, delivering adjusted earnings of $1.55 per share and total revenues of $1.48 billion, supported by higher oil-equivalent production volumes. The first quarter marked SM’s first full reporting period after the close of the Civitas merger.

The quarterly results showed an impressive 88% increase in the average net daily production, supported by output from the legacy Civitas assets. SM Energy is an independent exploration and production company with an asset portfolio spanning four premier shale basins in the United States: the Permian Basin, DJ Basin, South Texas and the Uinta Basin.

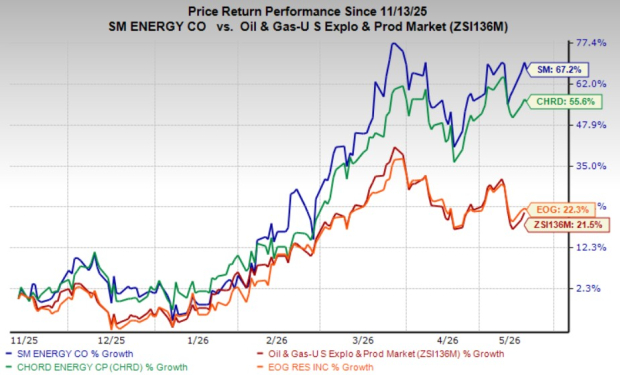

Over the past six months, SM stock has surged 67.2% compared with the industry’s 20% growth. Its peers, Chord Energy Corporation CHRD and EOG Resources EOG, have grown 55.6% and 22.3%, respectively, during the same time frame. While price performance demonstrates the attractiveness of a stock to some extent, it would be wiser to closely examine the company’s current business environment before offering any investment advice.

High-Quality Assets Support SM’s Production Growth

SM Energy has a top-tier asset base spread across four premier shale basins in the United States. The company owns 237,000 net acres in the Permian, 303,000 net acres in the DJ Basin, 94,000 net acres in South Texas and 62,000 net acres in the Uinta Basin, offering exposure to high-margin basins with oil-weighted production. The all-stock merger with Civitas Resources has been a major positive for SM, driving production growth through Civitas’ legacy assets.

The increased production is expected to benefit SM Energy, particularly given the favorable commodity price environment at present. Per the data from oilprice.com, the West Texas Intermediate crude prices are currently hovering around $100 per barrel, significantly higher than the prices seen at the beginning of the year. This is anticipated to boost the company’s earnings and cash flow profile in the near term.

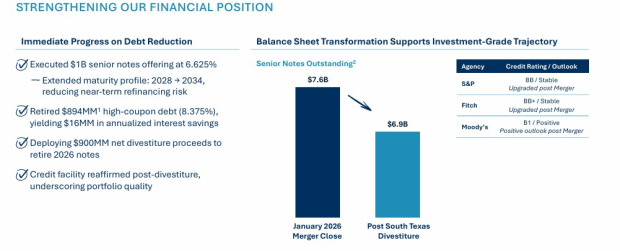

Significant De-Leveraging Efforts Strengthen SM’s Financial Position

SM Energy is taking significant strides to reduce its debt levels and strengthen its balance sheet. The company recently closed the divestiture of its South Texas assets and used $900 million in net proceeds from the transaction to reduce debt. In the first-quarter presentation, SM highlighted that it had retired $894 million of high-coupon debt, yielding $16 million in interest savings. The company has also indicated that it is on track to reduce leverage to the low-1x range earlier than its year-end 2026 target.

In addition to reducing debt, the company is focused on increasing free cash flow generation. The favorable commodity pricing environment, along with cost savings realized through merger-related synergies, is expected to drive higher free cash flows. SM noted that decreasing leverage and generating higher cash flows will enhance shareholder returns by increasing its allocation toward share buybacks.

Image Source: SM Energy

Valuation Snapshot

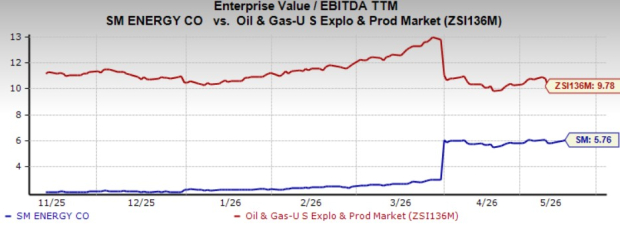

Coming to the valuation story, SM is currently considered cheap on a relative basis. The stock is trading at a trailing 12-month Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization (EV/EBITDA) of 5.76x, which is a discount compared with the broader industry average of 9.78x. Notably, Chord Energy and EOG Resources currently trade at a trailing 12-month EV/EBITDA of 4.03X and 6.27X, respectively.

Image Source: Zacks Investment Research

Time to Invest in the Stock or Wait?

SM Energy is well-positioned to benefit from rising commodity prices and its high-quality inventory spanning premier shale basins across the United States. Its production mix is mainly oil-weighted, enabling it to generate stronger profits in a higher crude price environment. Additionally, ongoing efforts to reduce its leverage and focus on generating higher cash flows should allow SM Energy to support higher shareholder returns.

Given that the stock is trading at a discount, investors should consider buying the SM stock, which sports a Zacks Rank #1 (Strong Buy) at present. CHRD currently sports a Zacks Rank #1, while EOG carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EOG Resources, Inc. (EOG): Free Stock Analysis Report

SM Energy Company (SM): Free Stock Analysis Report

Chord Energy Corporation (CHRD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).