Aflac Incorporated AFL is well-poised to grow on the back of growing sales in both Japan and the U.S. markets and rising margin in Japan. Its shares climbed 4.7% in the year-to-date period compared with 5% growth of the industry.

Aflac — with a market cap of $59.1 billion — operates as a supplemental health and life insurance products provider. Based in Columbus, GA, it has strong footprints in the United States and Japan. Courtesy of solid prospects, this presently Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Aflac’s U.S. segment continues to recover strongly, with sales rising 3% year over year to $1.6 billion in 2025 and 2.9% in to $318 million in the first quarter of 2026. Multiple acquisitions, product innovation, virtual channel growth and agent recruitment are expected to sustain momentum and reinforce its competitive positioning.

Meanwhile, sales in Japan jumped 16% to $498 million in 2025 and 25.5% to $113 million in the first quarter of 2026. Solid sales of Anshin Palette, Miraito and Tsumitasu are driving the numbers. The segment’s pretax profit margin is on the rise with 30.5% in 2023, 36% in 2024 and 36.7% in 2025. In the first quarter of 2026, pretax profit margin was at 35%, up from 31.8% in the year-ago period.

Furthermore, AFL’s benefit ratio from Japan business declined to 62.9% in the first quarter from 65% in the previous quarter. The company expects the metric to be within 60-63% in 2026. Aflac U.S. benefit ratio was 47.2% in the first quarter, while the full-year guidance is pegged at 48-52%.

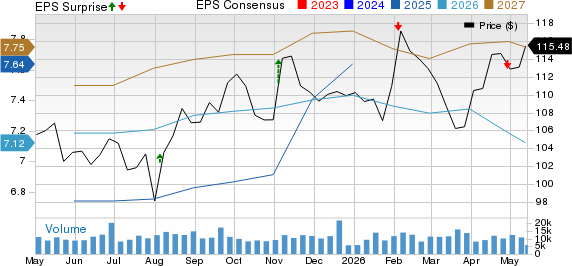

Estimates for Aflac

The Zacks Consensus Estimate for AFL’s current-year earnings is pegged at $7.12 per share, which witnessed one upward estimate revision in the past week against none in the opposite direction. The consensus mark for current-year revenues is pinned at $17.1 billion. Aflac’s earnings beat on estimates in two of the last four quarters and missed twice, the average being 7.9%.

Aflac Incorporated Price, Consensus and EPS Surprise

Aflac Incorporated price-consensus-eps-surprise-chart | Aflac Incorporated Quote

Key Risks

There are a few factors that investors should keep an eye on.

Operating cash flow has remained under pressure, declining 23.2% in 2022, 17.8% in 2023, 15.1% in 2024 and 5.6% in 2025. While the metric rebounded sharply in first-quarter 2026, rising 64.3% year over year, the company will need to sustain this momentum for a meaningful turnaround.

Aflac’s shares trade at a forward P/E of 15.71X, above both its five-year median of 12.93X and the industry average of 12.91X, indicating the stock is priced at a premium and leaving less room for outsized upside from current levels.

Better-Ranked Players

Some better-ranked stocks in the broader insurance space are Hamilton Insurance Group, Ltd. HG, Slide Insurance Holdings, Inc. SLDE and Radian Group Inc. RDN, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Hamilton Insurance’s current-year earnings of $3.95 per share increased 49 cents over the past week. HG’s earnings beat estimates in each of the trailing four quarters, with the average surprise being 84.8%. The consensus estimate for current-year revenues is pegged at $2.87 billion.

The consensus estimate for Slide Insurance’s current-year earnings is pegged at $3.51, which signals 4.5% year-over-year growth. Its earnings beat estimates in each of the trailing four quarters, with the average surprise being 41.8%. The consensus mark for Slide Insurance’s current-year revenues of $1.45 billion implies a 25.9% year-over-year jump.

The consensus estimate for Radian Group’s current-year earnings is pegged at $5.23 per share, which indicates 17.5% year-over-year growth. Its earnings beat estimates in each of the trailing four quarters, with the average surprise being 10.7%. The consensus estimate for RDN’s current-year revenues is pegged at $1.22 billion.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aflac Incorporated (AFL): Free Stock Analysis Report

Radian Group Inc. (RDN): Free Stock Analysis Report

Hamilton Insurance Group, Ltd. (HG): Free Stock Analysis Report

Slide Insurance Holdings, Inc. (SLDE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).