Rufus, Amazon.com's (AMZN) standalone artificial intelligence (AI) shopping bot launched during the generative AI boom, was designed to help consumers search, compare, and discover products through conversational prompts. But despite gaining traction, Amazon is now folding those capabilities directly into Alexa, retiring the Rufus brand in favor of a broader “Alexa for Shopping” experience embedded across the Amazon app, website, and Echo ecosystem.

The move signals far more than a product rebrand. It reflects Amazon’s growing belief that the future of e-commerce will be powered by deeply integrated AI agents rather than standalone chatbots. By turning Alexa into a persistent cross-platform shopping assistant that can remember preferences, track prices, answer contextual questions, and eventually take actions on behalf of users, Amazon is positioning itself to compete in the emerging era of agentic commerce.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

As AI shopping competition intensifies with rivals launching their own AI commerce tools, Amazon argues its advantage lies in its massive product catalog, customer review database, real-time inventory visibility, and delivery data. The company is also pushing deeper into AI-driven commerce through features like “Buy for Me,” which can purchase products from third-party retailers on behalf of users.

Alexa already has a massive consumer reach, brand familiarity, and years of behavioral data behind it, and consolidating Amazon’s AI efforts around Alexa could strengthen customer engagement, increase shopping conversion rates, and deepen the ecosystem.

About Amazon Stock

Amazon.com is a global technology and e-commerce behemoth, headquartered in Seattle, Washington. Today, the company operates across a dazzling range of businesses, cloud services via AWS, digital streaming, subscription services, advertising, physical retail, consumer electronics, and more. Its diversified growth model has placed it among the world’s most valuable public companies, with a market cap of $2.9 trillion, and it has a secure position in the Magnificent Seven group.

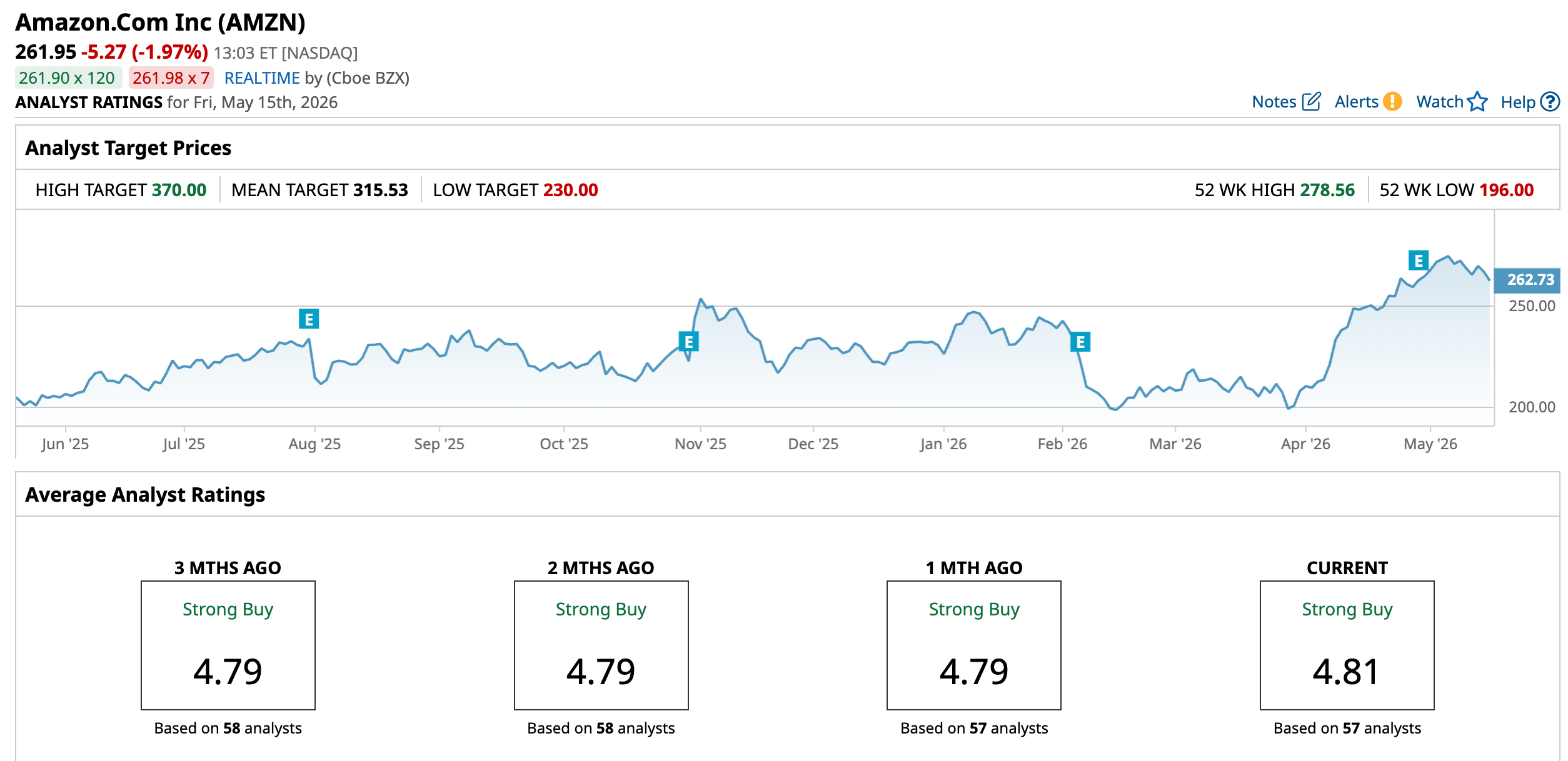

Amazon stock has delivered a strong performance over the past 12 months, fueled by accelerating AI momentum, robust AWS growth, and improving profitability across its retail and logistics operations. Shares are up 27.84% over the past 52 weeks and have gained 13.63% year-to-date (YTD), significantly outperforming the broader market.

The stock reached a fresh 52-week high on May 5, hitting $278.56 amid a post-earnings rally. Investors responded positively to Amazon’s stronger-than-expected Q1 2026 results, which included AWS revenue growth ahead of expectations and improving operating margins. The rally was further supported by enthusiasm around Amazon Supply Chain Services and the company’s expanding AI ecosystem.

However, following the announcement that Amazon would retire Rufus and integrate its capabilities into the new Alexa for Shopping, the stock reaction was relatively muted.

www.barchart.com

www.barchart.com AMZN currently trades at a premium compared to the sector median, but below its own historical average at 35.01 times forward earnings.

Steady Q1 Results

Amazon released its first-quarter 2026 financial results on April 29. Amazon generated net sales of $181.5 billion for the quarter ended March 31, 2026, up 17% year-over-year (YOY) from $155.7 billion in the prior-year period. North America sales rose 12% YOY to $104.1 billion, while International revenue climbed 19% YOY to $39.8 billion. AWS once again led growth, with cloud revenue surging 28% YOY to $37.6 billion, marking its fastest expansion rate in several years.

Profitability improved sharply during the quarter. Operating income increased significantly to $23.9 billion from $18.4 billion a year earlier. North America’s operating income rose to $8.3 billion from $5.8 billion, while International operating income improved to $1.4 billion from $1.0 billion. AWS’ operating income jumped to $14.2 billion compared with $11.5 billion in Q1 2025, underscoring the segment’s continued importance as Amazon’s primary profit engine.

Net income surged to $30.3 billion, or $2.78 per share, versus $17.1 billion, or $1.59 per share, in the year-ago quarter.

Cash flow metrics were more mixed as Amazon significantly accelerated AI infrastructure spending. Operating cash flow over the trailing twelve months increased 30% YOY to $148.5 billion. However, free cash flow fell sharply to $1.2 billion from $25.9 billion in the prior-year period due primarily to a $59.3 billion increase in property and equipment purchases related to AI data center and infrastructure expansion.

Advertising also remained a strong contributor, with ad revenue rising 24% YOY to $17.2 billion, while management highlighted growing momentum across AI initiatives, custom Trainium chips, and enterprise cloud demand.

Furthermore, Amazon guided for second-quarter 2026 revenue between $194.0 billion and $199.0 billion, representing expected growth of 16% to 19% YOY.

Meanwhile, analysts remain upbeat, projecting EPS of $7.71 for fiscal 2026, up 7.5% YOY, and anticipating a further 29.8% annual increase to $10 in fiscal 2027.

What Do Analysts Expect for Amazon Stock?

Most recently, TD Cowen reiterated its “Buy” rating and $350 price target on Amazon after the company launched “Amazon Now,” a new 30-minute grocery delivery service in major U.S. markets including Atlanta, Dallas-Fort Worth, Philadelphia, and Seattle.

Moreover, last month, KeyBanc raised its price target on Amazon to $330 from $325 while maintaining an “Overweight” rating, citing a stronger long-term profit outlook through 2027.

Also, Scotiabank raised its price target on Amazon to $325 from $275 while maintaining a “Sector Outperform” rating, citing accelerating growth in Amazon Web Services and improving profitability.

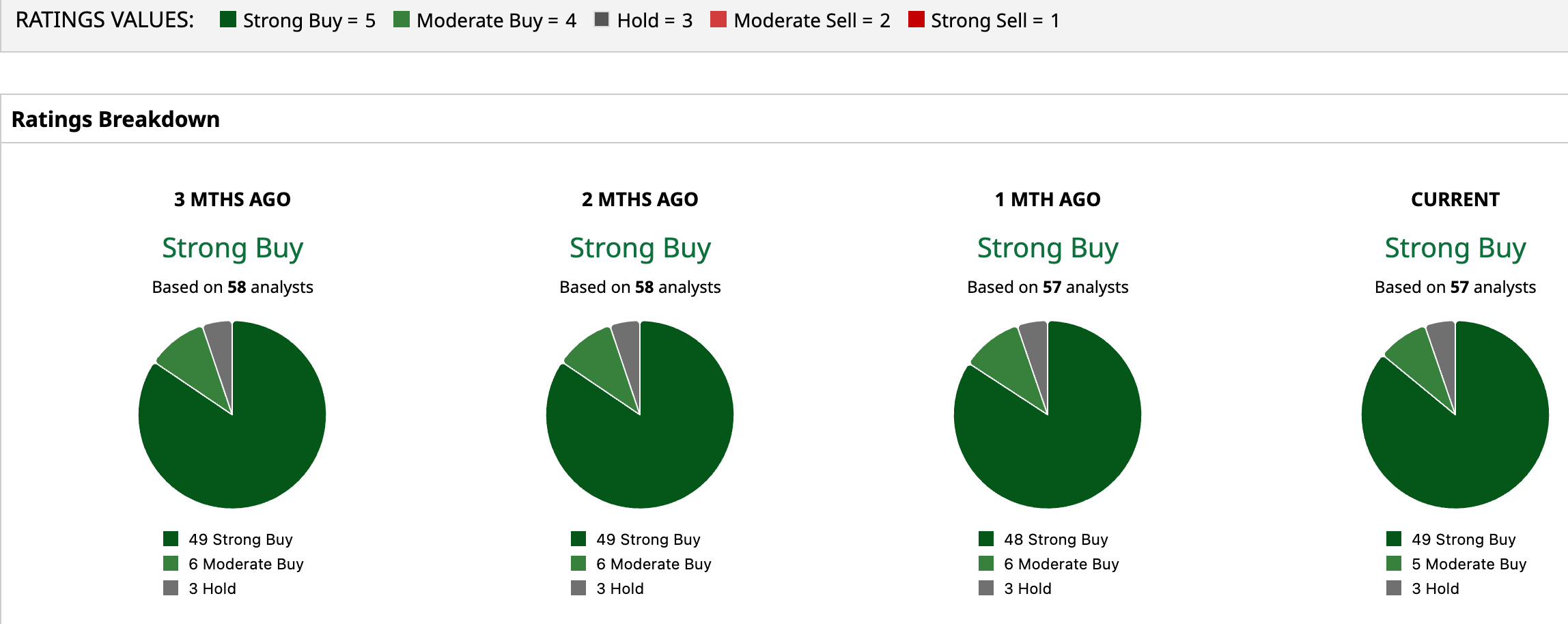

Overall, AMZN has a consensus “Strong Buy” rating. Of the 57 analysts covering the stock, 49 advise a “Strong Buy,” five suggest a “Moderate Buy,” and three analysts recommend a “Hold” rating.

The average analyst price target for AMZN is $315.53, indicating a potential upside of 20.5%. The Street-high target price of $370 suggests that the stock could rally as much as 41.3%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Alexa Is Finally Back in the Spotlight as Amazon Axes Rufus. What the AI Pivot Means for AMZN Stock. Dear Take-Two Stock Fans, Mark Your Calendars for May 18 Alibaba’s AI Growth Fails to Mask Plunging Profits: How to Play BABA Stock After Q4 Earnings Cisco Stock Jumps 13% as the Company Cuts 4,000 Jobs to Pivot Toward AI. Its Growth Story Is Far From Over.