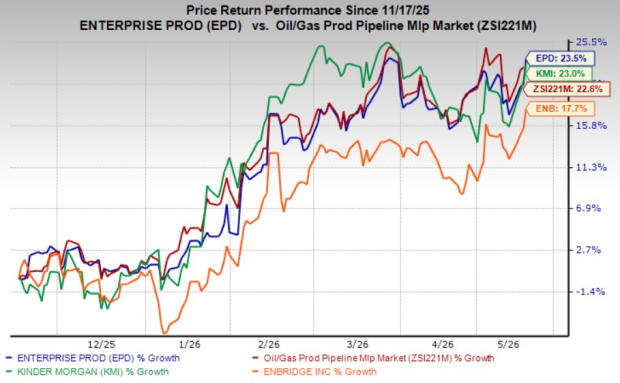

Enterprise Products Partners LP EPD units are rapidly climbing toward their 52-week high of $39.74, closing at $39.23 on May 14, 2026. Over the past year, EPD stock has gained 23.5%, outperforming the industry’s 22.7% growth. Its peers, Kinder Morgan KMI and Enbridge Inc. ENB, have grown 23% and 17.7%, respectively, during the same time frame.

Enterprise Products operates an integrated midstream asset network for the transportation and storage of crude oil, natural gas, natural gas liquids (NGLs), petrochemicals and refined products. The partnership’s midstream assets connect suppliers from some of the largest basins in the United States, Canada and the Gulf of America to various domestic and international markets. The partnership reported adjusted earnings of 68 cents per common unit, up from 64 cents in the prior-year quarter, but lagged the Zacks Consensus Estimate of 71 cents.

The partnership’s strong fundamentals and stable business model make Enterprise Products a preferred choice in the energy sector for risk-averse investors. However, it is essential to assess the broader operating environment for the stock before arriving at an investment decision.

EPD’s Contractual Business Model Ensures Stable Cash Flows

Enterprise Products owns and operates a 50,000-mile pipeline network that transports crude oil, natural gas, natural gas liquids and refined products across North America. The partnership generates stable fee-based revenues, implying that its earnings are less vulnerable to commodity price fluctuations. This allows EPD to generate predictable cash flows across business cycles. Notably, the partnership has highlighted that almost 90% of its long-term contracts include an escalation provision that protects its cash flows and distributions in inflationary business environments.

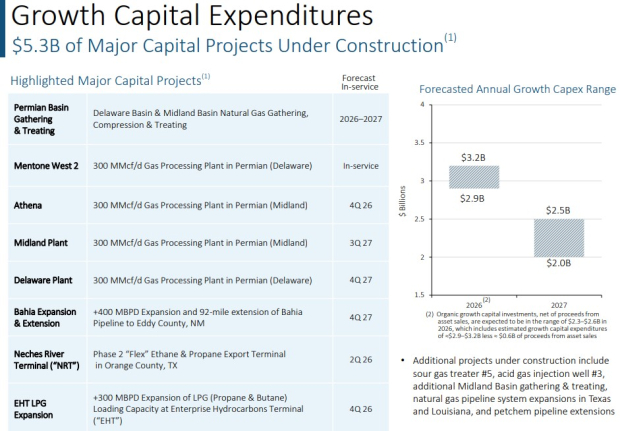

Additionally, the partnership has major capital projects worth $5.3 billion under development, expected to be placed into service through 2026 and 2027. These growth projects are backed by favorable market fundamentals, including rising production of crude oil, NGLs and natural gas in the Permian Basin, which should support sustained volume growth across EPD’s integrated value chain. Enterprise Products’ long-term contracts and sustained demand for its midstream services are expected to generate resilient earnings and cash flows.

Image Source: Enterprise Products Partners L.P.

EPD’s Financial Position Supports Resilience & Distribution Growth

Enterprise Products has a strong balance sheet, with nearly $3.3 billion in consolidated liquidity, comprising liquidity available under its credit facilities and unrestricted cash on hand. Its leverage ratio was 3.2x as of March 31, 2026, which lies within its target range of 2.75-3.25x. Moreover, the partnership has mentioned that nearly 95% of the debt was fixed, implying that short-term fluctuations in interest rates will not significantly affect interest payments. The strong balance sheet allows EPD to maintain its resilience across various business cycles and withstand downturns better.

Enterprise Products also believes that its discretionary free cash flow could reach up to $1 billion in 2026, despite increasing its growth capital expenditure by $300 million. In the near term, the partnership plans to allocate free cash flows toward growing distributions, unit buybacks and debt reduction. This indicates that, alongside improving its financial position, Enterprise Products intends to increase returns to unitholders. Notably, Enterprise has increased its distributions for 27 consecutive years. As of March 31, 2026, the partnership had returned approximately $5.1 billion of capital to unitholders on a trailing 12-month basis.

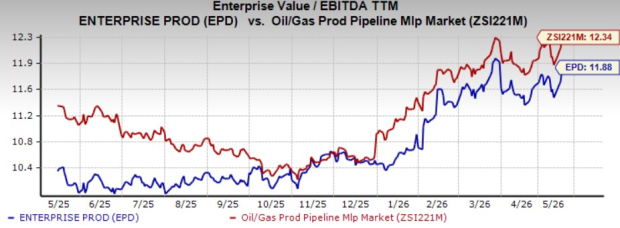

Valuation Snapshot

Considering the valuation snapshot, EPD is currently considered cheap on a relative basis. The stock is trading at a trailing 12-month Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization (EV/EBITDA) of 11.88x, which is a discount compared with the broader industry average of 12.34x. Notably, Kinder Morgan and Enbridge currently trade at a trailing 12-month EV/EBITDA of 14.59x and 17.37x, respectively.

Image Source: Zacks Investment Research

Final Verdict: Time to Buy or Hold?

Enterprise Products is expected to generate stable earnings and cash flows, backed by its long-term, inflation-protected contracts. The demand growth for U.S. energy products in domestic and international markets is expected to drive sustained volume growth across EPD’s integrated gathering, processing, transportation and export value chain.

Given that the stock is currently undervalued, investors should consider buying the EPD stock, which currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Enterprise Products Partners L.P. (EPD): Free Stock Analysis Report

Enbridge Inc (ENB): Free Stock Analysis Report

Kinder Morgan, Inc. (KMI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).