As Costco Wholesale Corporation COST prepares to unveil its third-quarter fiscal 2026 earnings results on May 28, after the market closes, investors face an important decision: Should they buy, hold or sell the stock? With expectations and market conditions in focus, it is crucial to evaluate the key factors influencing Costco’s performance and whether the stock offers an attractive entry point.

Costco's strategic investments, customer-centric approach, merchandise initiatives and focus on membership growth have supported steady sales and earnings growth, positioning COST as a consumer defensive stock.

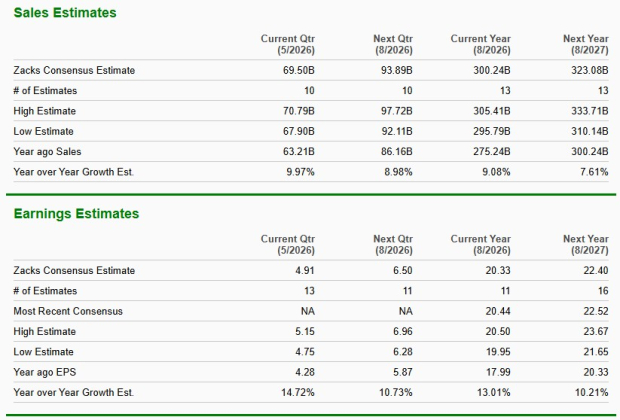

Analysts are optimistic about Costco's upcoming earnings. The Zacks Consensus Estimate for third-quarter revenues stands at $69.50 billion, calling for a 10% increase from the prior-year reported figure. On the earnings front, the consensus estimate has improved by 3 cents to $4.91 per share over the past 30 days, implying a 14.7% year-over-year jump.

Costco has a trailing four-quarter earnings surprise of 1.1%, on average. In the last reported quarter, this Issaquah, WA-based company beat the Zacks Consensus Estimate by a margin of 0.7%.

Image Source: Zacks Investment Research

What the Zacks Model Predicts About COST’s Q3 Earnings

As investors prepare for Costco's third-quarter announcement, the question looms regarding earnings beat or miss. Our proven model predicts that an earnings beat is likely for Costco this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Costco has an Earnings ESP of +1.95% and carries a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

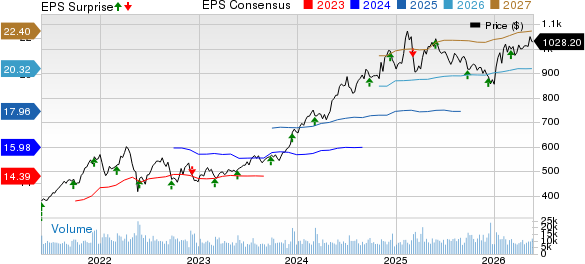

Costco Wholesale Corporation Price, Consensus and EPS Surprise

Costco Wholesale Corporation price-consensus-eps-surprise-chart | Costco Wholesale Corporation Quote

Costco: Key Factors at Play

Costco’s third-quarter performance is likely to have benefited from continued momentum in membership growth, strong renewal trends and steady traffic gains across regions. Management highlighted that members remain focused on value and quality, which continues to support shopping frequency and basket expansion even in a cautious consumer environment. Costco also continued to benefit from growth in executive memberships and member upgrades, supported by added member benefits and retention initiatives. The Zacks Consensus Estimate calls for total paid members of 83.7 million in the quarter, with membership fee income expected to improve 9.9%.

The company’s ability to maintain loyalty while attracting younger and digitally engaged shoppers is likely to have supported healthy comparable sales growth during the quarter. The Zacks Consensus Estimate calls for comparable sales growth of 8.1% for the quarter under discussion, with expected increases of 6.5% in the United States, 8.4% in Canada and 9.8% in Other International markets.

The company’s merchandising initiatives and pricing strategy are also likely to have been key contributors to third-quarter performance. Costco continued to lean on its value positioning by lowering prices on select everyday essentials while expanding its Kirkland Signature offerings across food and non-food categories. Costco’s disciplined inventory management and sourcing flexibility are likely to have helped the company maintain product availability and support customer demand despite an evolving global trade environment.

Another important driver for the quarter is Costco’s continued digital and operational progress. The company has been investing heavily in improving the member experience both online and inside warehouses through personalization tools, app enhancements and faster checkout capabilities. The rollout of personalized recommendations, same-day delivery partnerships and technology-led efficiency improvements is likely to have supported higher customer engagement while also helping Costco improve productivity.

That said, potential operational headwinds could have tempered third-quarter performance. Costco continues to navigate a complex global environment marked by shifting trade policies, tariff-related uncertainties and commodity volatility, which may have pressured sourcing and merchandising operations. Slightly softer renewal rates among digitally acquired members may have remained a modest area of pressure during the quarter.

Costco Stock Price Performance

Costco, which competes with Dollar General Corporation DG, Ross Stores, Inc. ROST and Target Corporation TGT, has seen its shares jump 19.1% in the year-to-date period compared with the industry’s rise of 14%. While shares of Target and Ross Stores have rallied 28.5% and 30.3%, respectively, those of Dollar General have fallen 20.4% in the aforementioned period.

Image Source: Zacks Investment Research

Does Costco Tick the Boxes for Value Investing?

From a valuation standpoint, Costco currently trades at a premium relative to its industry peers. The company’s forward 12-month price-to-earnings (P/E) ratio is 47.06, higher than the industry average of 32.45 and the S&P 500’s 22.06. The stock is also trading above its median P/E level of 46.86, observed over the past year.

Costco is trading at a premium to Target (with a forward 12-month P/E ratio of 14.88), Ross Stores (30.08) and Dollar General (14.14).

Image Source: Zacks Investment Research

How to Play Costco Stock Ahead of Q3 Earnings?

Costco appears well-positioned heading into its third-quarter earnings release, supported by resilient membership trends, steady traffic growth, strong value positioning and continued digital momentum. The company’s disciplined execution and customer-focused strategy are likely to have helped offset ongoing macroeconomic and tariff-related uncertainties. Given Costco’s favorable earnings indicators and stable long-term fundamentals, existing investors may consider holding the stock ahead of the release. For potential investors, it may be prudent to wait for either post-earnings clarity or a more attractive entry point before initiating new positions, rather than buying aggressively ahead of the report.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).