Memory chipmaker Micron (MU) is heeding President Donald Trump's call for companies to manufacture in the United States. As the only major U.S. manufacturer of high-demand memory chips, Micron is not merely a critical player in the artificial intelligence (AI) industry; its importance in the larger realm of geopolitical significance is indisputable, just like Nvidia (NVDA).

Now, the company is bringing 1-alpha DRAM manufacturing to Manassas, Virginia. What is 1-alpha — and is it even possible for this news to take MU stock higher ? Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Micron's ‘Alpha’ Story

Understanding 1-alpha requires placing it within the broader arc of Micron's generational DRAM node roadmap rather than evaluating it in isolation. It represents the fourth generation within Micron's 10-nanometer-class DRAM architecture — sitting after the 1x, 1y, and 1z generations in sequence — and its introduction brought new lithography and patterning techniques that allowed memory cells to continue shrinking while becoming more power efficient in the process.

Measured against its immediate predecessor, the 1z node, 1-alpha delivered a 40% improvement in memory density alongside power savings of up to 20% for mobile applications, advances that were genuinely substantial at the time of its arrival in 2021. The manufacturing philosophy behind 1-alpha also drew attention from a competitive positioning standpoint. Micron built 1-alpha on ArF immersion-based lithography, deliberately avoiding the extreme ultraviolet (EUV) photomasks that Samsung had chosen to adopt for its own DRAM scaling at the same generational step. Despite taking a different path, Micron reached an industry-leading bit density of 0.315 gigabits per square millimeter with 1-alpha, making it the most densely packed DRAM commercially available at one point.

For Micron investors, the practical expectation attached to 1-alpha was that it would serve as a vehicle for gaining ground in the highly lucrative DRAM market. The competitive landscape as of the first quarter of 2025 showed SK Hynix holding a 36% share of the global DRAM market, edging past Samsung's 34% for the first time. SK Hynix's commanding position in HBM3E for AI applications has given it both pricing power and a margin profile in the fastest-growing corner of the memory market that Micron has been actively working to match. Progress has been real, particularly in HBM3E supply to Nvidia, but the gap in volume and yield relative to SK Hynix remains a genuine constraint on how rapidly Micron can fully convert its node-level technology advantages into revenue within the AI infrastructure buildout.

The alpha thesis for Micron, however, extends beyond 1-alpha alone. The 1-gamma node enters the picture as a forward-looking dimension of the same story. Built on EUV lithography combined with advanced high-k metal gate (HKMG) technology, 1-gamma is engineered to make devices simultaneously smaller, faster, and less power hungry. The density gains that come with fitting more bits onto each wafer translate into greater output capacity without a proportional increase in capital investment, while the reduction in energy consumption at the component level gives hyperscalers a meaningful lever for managing operating costs. When combined with faster memory performance, the result is a technology foundation that makes producing high-margin AI solutions considerably more practical.

CXL adds another dimension to why the memory story at Micron deserves attention. The technology enables large numbers of AI systems to draw from a shared memory pool, a capability that grows more valuable as model sizes continue to expand and AI inference workloads become increasingly dependent on access to large volumes of memory.

Micron has already moved into production of CXL memory chips, and the customer base among hyperscalers is beginning to transition from exploratory pilots toward commercial-scale deployments. Given that the number of companies capable of manufacturing high-end DRAM in meaningful volume remains very small, Micron stands to benefit disproportionately as CXL adoption builds momentum across the AI infrastructure landscape.

Strength Backed by Fundamentals

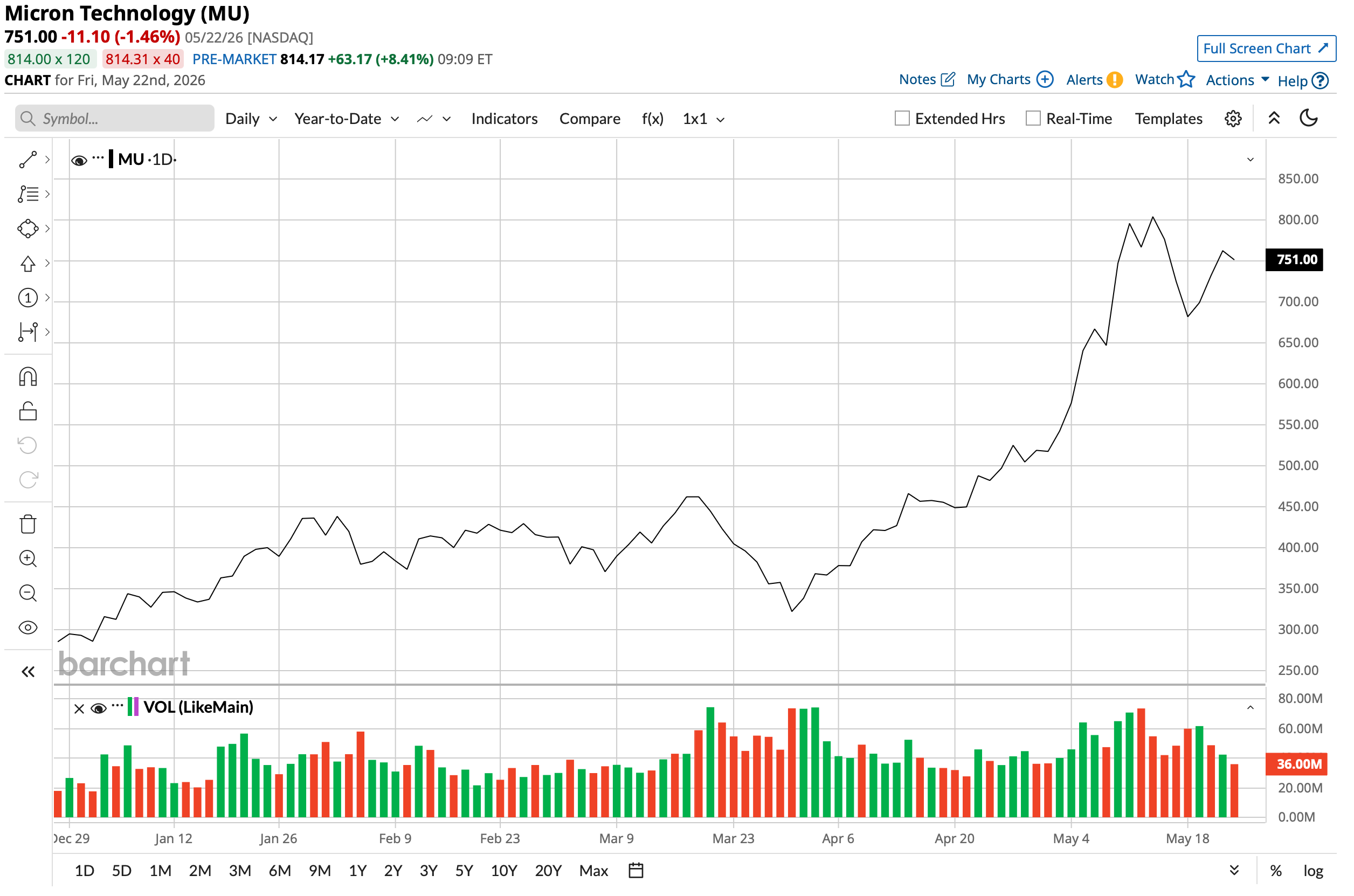

My last report on Micron was just a few days before its Q2 2026 print. Since then, MU stock has climbed to a massive 74% gain in the past month and is up 220% on a year-to-date (YTD) basis.

www.barchart.com

www.barchart.com A beat on both the revenue and earnings front certainly helped. Q2 2026 saw the company report revenue of $23.9 billion, up four times from the prior-year period. In fact, not a single segment of the business witnessed a yearly growth rate of less than 150%. Notably, the Mobile and Client Unit segment saw revenue increase by 244% on a year-over-year (YOY) basis to $7.71 billion, while the vital Data Center segment reported revenue of $5.69 billion, a rise of 211% YOY.

Gross margins almost doubled to 74.9% from 37.9%, signifying a strong demand trend and the company's competitive solidity. Meanwhile, earnings jumped to $12.20 per share from a mere $1.56 in the prior-year period, easily surpassing consensus estimates. This marked the ninth consecutive quarter of an earnings beat from the company.

Net cash from operating activities for the six months ended February 26, 2026, stood at $20.3 billion, up from $7.2 billion in the year-ago period. Overall, Micron closed the quarter with a cash balance of $13.9 billion. This was much higher than its short-term debt levels of $585 million.

For Q3 2026, Micron forecast revenue to be between $32.75 billion and $34.25 billion. Similarly, earnings are expected to be somewhere between $18.75 per share and $19.55 per share. Meawnhile, analysts expect revenue and earnings of $33.59 billion and $19.15 per share, respectively.

In terms of valuation, Micron still trades at relatively undervalued levels. Its forward price-to-earnings (P/E) ratio of 12.9 times sits below the sector median, while the forward price-to-sales (P/S) ratio sits at 7.7 times.

What Do Analysts Think of Micron Stock?

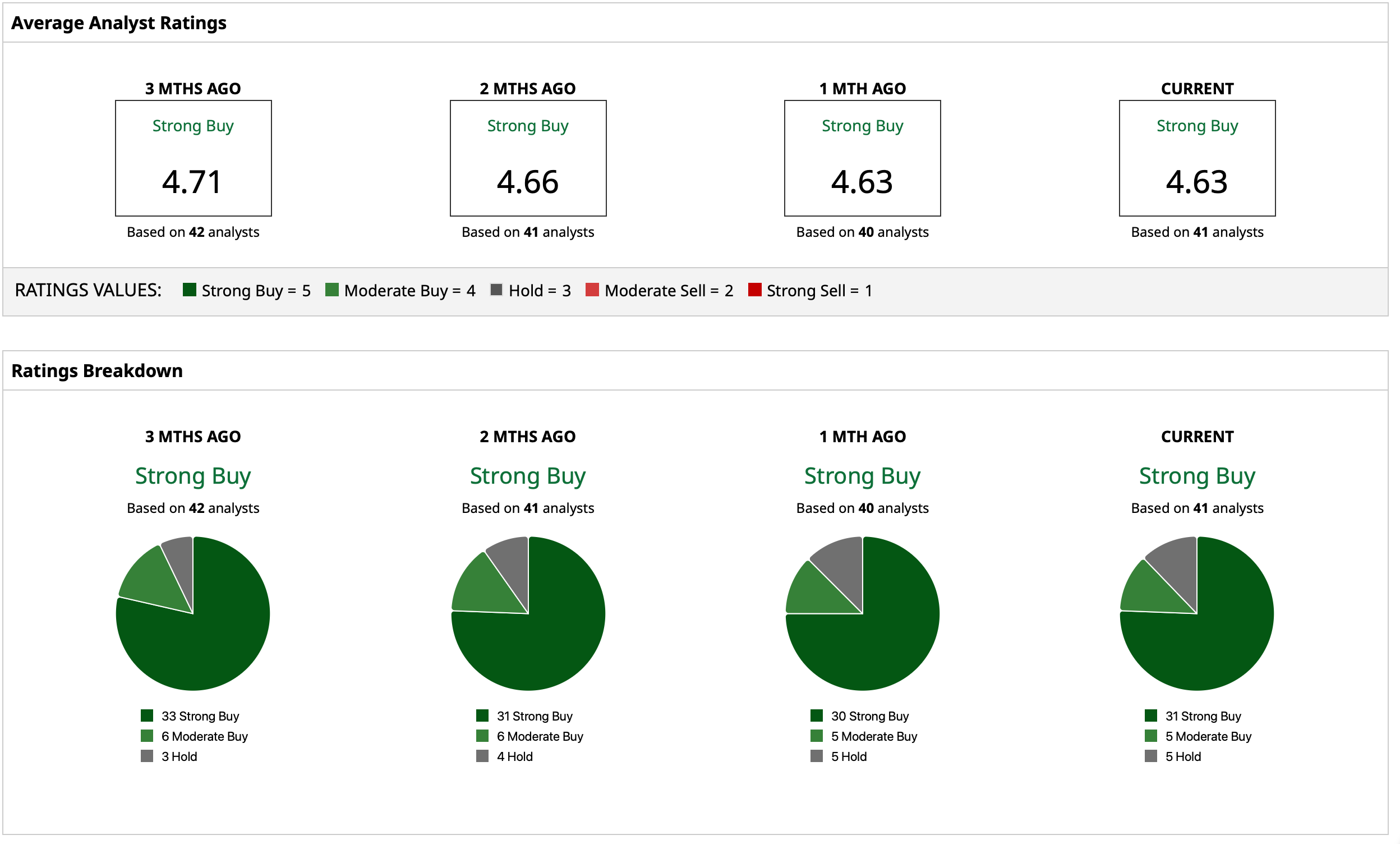

Overall, analysts have a consensus “Strong Buy” rating for MU stock. The mean target price of $628.20 has already been surpassed, but the high target price of $1,100 points to potential upside of about 23% from current levels. Out of 41 analysts covering the stock, 31 have a “Strong Buy” rating, five have a “Moderate Buy” rating, and five have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Bank of America Says Nvidia Is Still the Top AI Compute Stock to Buy Despite YTD Underperformance. Here’s Why. Why Amazon’s AI Game Looks Completely Different Than Every Other Tech Giant Tesla Has a SpaceX Stake and $890 Million in Related Revenue. The Upcoming SpaceX IPO Could Be a Major Win for TSLA Stock. As Micron Heeds Trump’s Call for Domestic DRAM Manufacturing, MU Stock Is Still Undervalued