The word “snowflake” in common parlance among the younger generation has a negative connotation, often associated with people who take offense easily and are deemed to be fragile. For the cloud-based data company Snowflake (SNOW), the “SaaSpocalypse” narrative had elicited almost a similar reaction.

However, that was that, a narrative that generative AI platforms would snatch the lunch of companies like Snowflake. The Q1 results of the company did a lot to change that.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Snowflake

Founded in 2012, Snowflake is a data infrastructure company that sits at the intersection of cloud computing, data analytics, and artificial intelligence, helping organizations store, process, share, and analyze massive amounts of data across multiple cloud providers. Its platform allows organizations to warehouse data, build data lakes, engineer data, and seamlessly share data.

Valued at a market cap of $82.7 billion, SNOW stock is up 14% on a YTD basis. In this context, the 36.5% rally in yesterday's trading session gives us a hint as to how strong its Q1 print was. But is that enough to bring the stock under your portfolio's fold? Let's find out.

www.barchart.com

www.barchart.com First Class Q1

The results for the first quarter of 2026 were marked by the strongest sequential growth in the company's history, with revenue and earnings surpassing estimates and the company raising its guidance.

Total revenues went up by 33% from the prior year to $1.39 billion, wherein product revenues increased by 34% to $1.33 billion. Revenue from professional services rose by 25.1% in the same period to $56.6 million. Further, earnings moved higher by 62.5% on a YOY basis to $0.39 per share, surpassing the Street estimates of $0.32 per share. Notably, this was the eighth consecutive quarter of earnings beat from the company.

Remaining performance obligations (RPO) and net revenue retention rates (NRR) are two critical metrics for any platform company, denoting demand and customer retention, respectively. While RPO for the quarter stood at $9.21 billion, up 38% from the prior year, the NRR at 126% means the existing customers are spending more on Snowflake's platform. The quality of the customers also remains high with 813 of the Forbes Global 2000 customers now using Snowflake.

Net cash from operating activities for the quarter ended April 30, 2026, was at $243.2 million, up from $228.37 million in the year-ago period. Overall, Snowflake's Q1 ended with a cash balance of $2.08 billion, with short-term debt of just $55.8 million.

Moreover, the company announced the acquisition of Natoma. Snowflake has a wide presence in the realm of agentic AI, and security remains an issue. This is where Natoma steps in. Natoma's platform provides a centralized MCP gateway identifying the details of who accessed which AI agents embedded into the enterprise.

Further, the $6 billion deal with Amazon Web Services (AWS) (AMZN) was also noteworthy. Under the terms of the deal, Snowflake will buy Graviton compute power from AWS to increase its compute capacity and serve its ever-growing enterprise customer base.

Lastly, Snowflake raised its full-year 2027 product revenue guidance to $5.84 billion from $5.66 billion earlier. Also, operating margin expectations were raised to 13.5% from 12.5%.

However, even after a modest rise on an overall basis this year, SNOW stock is trading at overvalued levels. Its forward P/E, P/S, and P/CF of 97.67x, 10.22x, and 48.17x are all much above the sector medians of 24.61x, 3.51x, and 19.52x, respectively.

Snowflake's Twin Pillars of Growth

As agentic AI becomes the next evolution of the AI revolution, Snowflake has two weapons in its arsenal to win this war: Cortex Code and Snowflake Intelligence, the fastest-adopted products in Snowflake's history.

While Snowflake Intelligence functions as a personalized AI work agent tailored to the needs of enterprise users, Cortex Code occupies a different but complementary role as Snowflake's dedicated AI coding agent, built on top of Claude Code and aimed specifically at data engineers, developers, and data scientists. Each of these products deserves a closer look on its own terms.

At its core, Snowflake Intelligence gives business users the ability to query enterprise data through natural language, generate insights, automate decisions, and trigger workflows without writing a single line of code. That is genuinely new territory for Snowflake, which until recently was largely a backend platform for data teams.

Remarkably, early enterprise adopters are reporting an average ROI of 41% from agentic AI initiatives but the barriers are high. Snowflake Intelligence offers an enterprise platform where every answer is traceable back to its source, whether a specific SQL query or the documents referenced, and data teams can flag verified responses with a "golden" status signal. That kind of auditability matters enormously to regulated industries.

Looking ahead, Snowflake is shaping the next version of Intelligence through direct customer feedback and insights from the research preview of Project SnowWork, pointing toward deeper agentic workflow capabilities across the full enterprise data estate.

Now, coming to Cortex Code. Launched in November 2025, Cortex Code is a Snowflake-native AI coding agent that understands which tables in your environment are sensitive, which transformations are expensive, and which pipelines are production-critical. By a few months in, it had already drawn over 4,400 new users, and more than 50% of Snowflake customers were actively using it. This kind of uptake is quite impressive for a product whose lifetime has not even exceeded a year.

Notably, Snowflake is also expanding model flexibility, letting customers choose between Claude Opus 4.6 and OpenAI GPT-5.2 depending on their quality, latency, and cost priorities. On the roadmap side, Cortex Code is extending support to dbt and Apache Airflow workflows, ensuring it covers the full stack of tools data engineers actually use rather than just the Snowflake-native slice.

Analyst Opinion

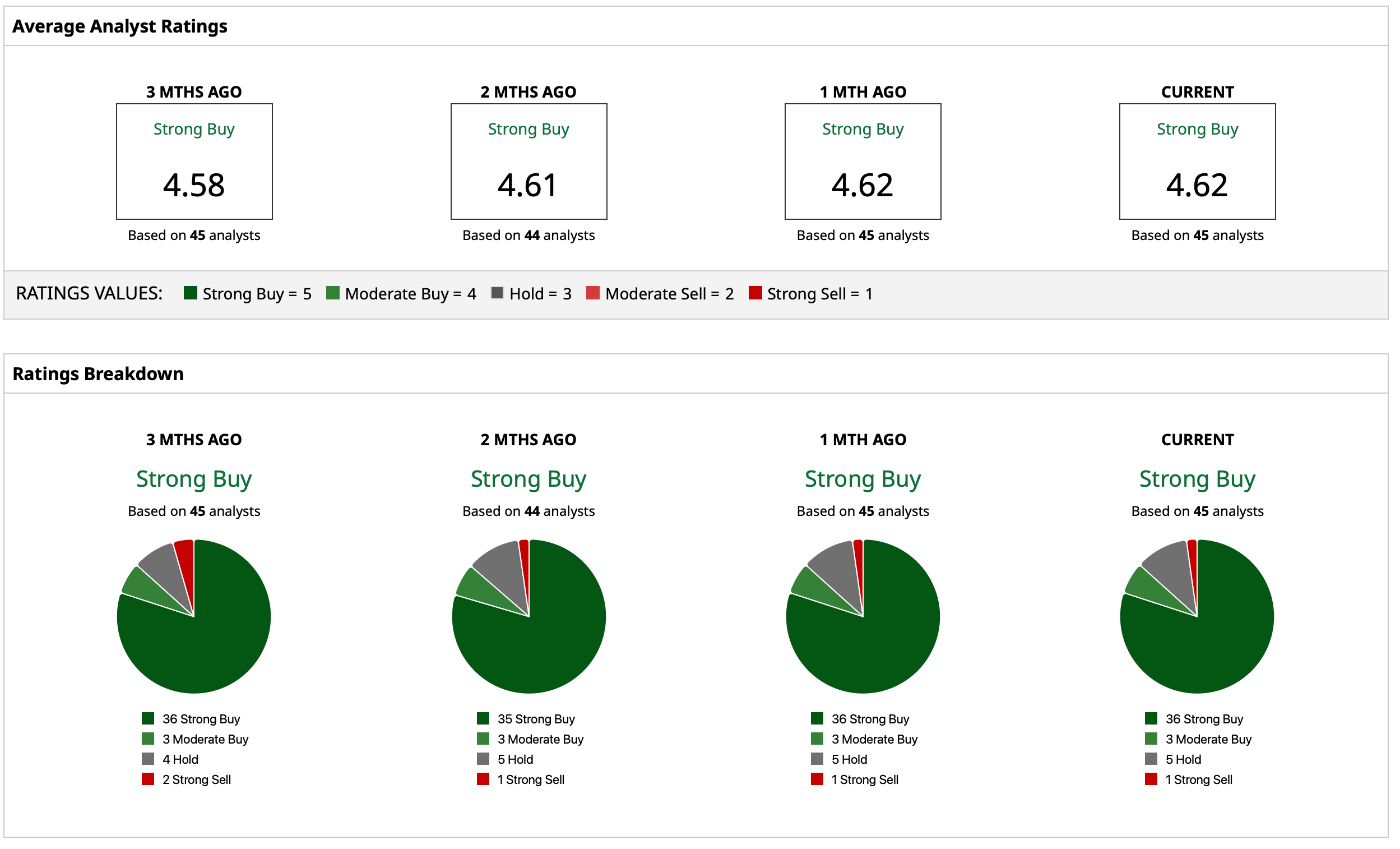

Thus, analysts have assigned a rating of “Strong Buy” for SNOW with a mean target price that has already been surpassed. The high target price of $325 denotes an upside potential of about 30% from current levels. Out of 45 analysts covering the stock, 36 have a “Strong Buy” rating, three have a “Moderate Buy” rating, five have a “Hold” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Snowflake Stock Rallies on Blockbuster Q1 Results. It Turns Out That Gen AI Isn’t Eating Its Lunch. Dycom Industries Stock Just Skyrocketed. It's the Latest Winner from Data Center Demand. The 180-Day Lease Holding Up SpaceX's $2 Trillion IPO